Updated on February 24th, 2026 by Felix Martinez

The Dividend Aristocrats are S&P 500 companies that have raised their dividends for at least 25 consecutive years. The list changes each year as new companies are added (and occasionally removed when streaks end).

Fastenal Co. (FAST) was the one addition to the Dividend Aristocrats list in 2024.

You can see the full list of all 69 Dividend Aristocrats here.

We created a comprehensive list of all Dividend Aristocrats, along with key financial metrics, including price-to-earnings ratios and dividend yields. You can download your copy of the Dividend Aristocrats list by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Fastenal increased its dividend for the 27th consecutive year last year. On January 16th, 2026, Fastenal raised its quarterly dividend by 9.1%, from $0.22 to $0.24.

This article will discuss the most recent addition to the Dividend Aristocrats list in greater detail.

Business Overview

Fastenal began in 1967 when Bob Kierlin and four friends pooled together $30,000 to open the first store. The original intent was to dispense nuts and bolts via vending machine, but that idea got off the ground after 20 years.

The company went public in 1987 and today provides fasteners, tools, and supplies to its customers via 1,592 public branches, 1,872 active Onsite locations, and over 115,000 managed inventory devices.

Fastenal has a market capitalization of $51.7 billion.

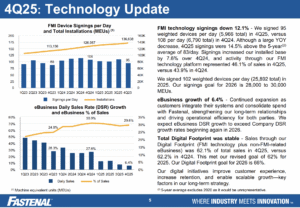

Fastenal reported (1/20/26) fourth-quarter and full-year results for fiscal 2024 in January. The company reported solid 2025 results, with net sales increasing 8.7% to $8.20 billion, net income rising 9.4% to $1.26 billion, and diluted EPS growing to $1.09.

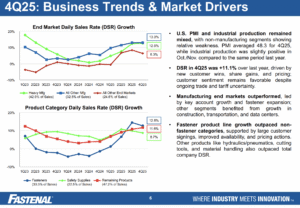

Fourth-quarter sales rose 11.1% year over year to $2.03 billion, supported by higher unit volumes, pricing benefits of roughly 310–340 basis points, and continued expansion in large contract customers. Operating income increased 9.6% annually, with operating margins improving slightly to 20.2%, reflecting disciplined expense control despite inflationary cost pressures.

Growth was primarily driven by manufacturing customers, which represented 75.4% of quarterly sales and grew 12.8% year over year, alongside strength in transportation and data-center demand. Fastenal’s technology-enabled distribution model continued gaining traction, with FMI (FASTBin, FASTVend, and FASTStock) sales rising 14.6% to $3.71 billion, accounting for 44.7% of total revenue, while digital footprint sales reached 61.4% of total sales.

Higher spending from large customer sites and expanding managed inventory programs supported consistent share gains even as broader industrial production remained sluggish.

Looking ahead, management expects continued growth driven by customer contract wins, digital inventory expansion, and increased capital investment of $310–$330 million in 2026, aimed at logistics capacity, IT upgrades, and distribution efficiency improvements.

While near-term demand remains tied to industrial activity cycles, Fastenal’s increasing penetration of large enterprise accounts and its automation-driven service model position the company for steady revenue growth and margin stability across varying economic conditions.

Source: Investor Presentation

Growth Prospects

Fastenal has grown its earnings per share at an average annual rate of 10.3% over the last decade and 8.1% over the last five years. This has been driven by a variety of factors, including sales more than doubling, improved margins, and tax reform.

The COVID-19 pandemic impacted many businesses, but Fastenal proved resilient in 2020. The traditional business faced challenges, but the Safety segment more than offset lost sales. We expect 7% earnings-per-share growth over the next five years.

Fastenal is in the midst of a transformation from traditional public branches to Onsite locations and managed inventory (mostly vending devices), leading the business’s growth story.

We believe this is a prudent move that will help establish stickier customer relationships. This is especially true since only a small fraction of the company’s business is from walk-in customers, while the majority is done business-to-business.

Source: Investor Presentation

Competitive Advantages & Recession Performance

Fastenal has a first-mover competitive advantage in its industrial vending and Onsite locations, creating a very sticky and well-attuned customer relationship with high switching costs.

Moreover, its scale enables the company to continue growing, adapt to customer preferences, and reliably deliver the goods customers need.

You can see Fastenal’s earnings-per-share during the Great Recession below:

- 2007 earnings-per-share: $0.19

- 2008 earnings-per-share: $0.24

- 2009 earnings-per-share: $0.16

- 2010 earnings-per-share: $0.23

Earnings declined during the worst of the recession, but the company remained profitable. This kept the dividend rising during that period.

While we note cyclical possibilities in the construction industry, the company has thus far proven itself well-prepared to weather financial storms.

We note that the dividend payout ratio rose to 80% in 2026, but we believe this is reasonable given the company’s debt-free balance sheet.

Valuation & Expected Returns

Based on the expected adjusted EPS of $1.25 For fiscal 2025, Fastenal stock is currently trading at 36.4 times that figure. The earnings multiple is above our fair value estimate at 24x.

This implies a 7% annual headwind should it reach 24 times earnings over the next five years. The expected earnings growth will offset the decline, which we estimate at 7% per year.

Fastenal stock also has a current dividend yield of 2.1%. Therefore, we project total annual returns of 2.1% over the next five years.

Final Thoughts

Fastenal has proven to be a great company with consistent earnings and dividend growth. Moreover, it is executing moves to further cement its position as a go-to supplier.

However, the stock has more than doubled over the past five years and is now overvalued. We expect the stock to generate a 2.1% average annual total return over the next five years. The stock maintains its hold rating.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: