Updated on March 18th, 2026 by Nathan Parash

Each year, we individually review each of the Dividend Aristocrats, a group of 69 stocks in the S&P 500 Index that have raised their dividends for at least 25 consecutive years.

To make it on the list of Dividend Aristocrats, a company must possess a profitable business model, a valuable brand, global competitive advantages, and the ability to withstand recessions. This is why Dividend Aristocrats can continue to raise their dividends in difficult years.

With this in mind, we have created a list of all 69 Dividend Aristocrats.

You can download your free copy of the Dividend Aristocrats list, along with important financial metrics such as price-to-earnings ratios and dividend yields, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

One company that has a very impressive dividend growth track record is Nordson Corporation (NDSN), which has raised its dividend for 62 consecutive years.

This article will discuss the company’s business overview, growth prospects, competitive advantages, and expected returns.

Business Overview

Nordson was founded in 1954 in Amherst, Ohio, by brothers Eric and Evan Nord, but the company’s roots go back to 1909 with the U.S. Automatic Company.

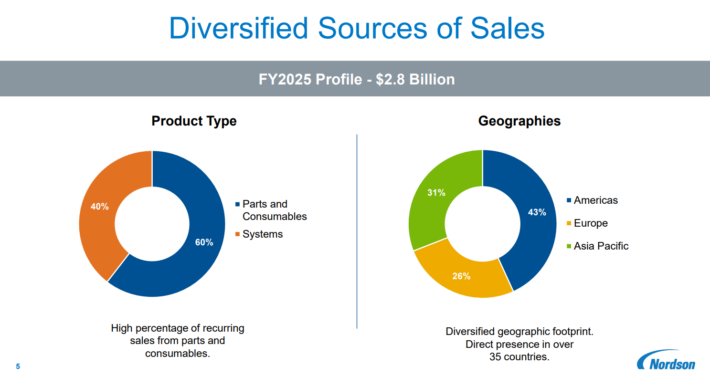

Today, the company has operations in over 35 countries and engineers, manufactures, and markets products used for dispensing adhesives, coatings, sealants, biomaterials, plastics, and other materials. These products have applications ranging from diapers and straws to cell phones and aerospace.

Source: Investor Presentation

On February 18th, 2026, Nordson reported first quarter results for the period ending January 31st, 2026. (Nordson’s fiscal year ends October 31st.) The company reported that sales increased 9% to $669 million. Growth was driven by a 7% improvement in organic sales and a 4% tailwind from favorable currency exchange, partly offset by the divestiture of the medical contract manufacturing business.

Adjusted EPS grew 15% to $2.37, while the backlog increased 4%, indicating solid future demand.

The Industrial Precision Solutions and Advanced Technology segments saw sales increase by 9% and 23%, respectively, while Medical and Fluid Solutions revenue was relatively flat

For Q2, Nordson expects sales between $710 and $740 million, with adjusted EPS of $2.70 to $2.90. The company sees improving order trends and a growing backlog as signs of strength in its business.

For the fiscal year, Nordson expects revenue in a range of $2.86 billion to $2.98 billion, which would be a 4.6% increase from FY 2025 at the midpoint. Adjusted earnings-per-share are projected to be in a range of $11.00 to $11.60. At the midpoint, this would represent growth of 10.4% year-over-year.

Growth Prospects

From 2016 through 2025, Nordson grew earnings-per-share by a solid 9.1% annually. However, this growth rate has accelerate to 13.3% over the past five years.

In its investment thesis, Nordson lists factors such as best-in-class technology that boosts client production while cutting costs, a worldwide service model, a balanced income stream, and a successful track record.

A growing demand for disposable goods, productivity investments, mobile computing, an increase in the use of medical devices, and the production of lightweight/lean vehicles are all areas of growth for the company’s adhesive and coating sectors, and would add to the company’s top line.

Nordson will keep making acquisitions to gain access to unique precision technologies and strengthen its competitive advantage.

For example, in 2023 Nordson completed its acquisition of the ARAG Group. ARAG is a global market and innovation leader in developing, producing and supplying precision control systems and smart fluid components for agricultural spraying. More recently, the company added Atrion Corporation in 2024, which expanded Nordson’s footprint in the areas of infusion fluid delivery and niche cardiovascular solutions.

Acquisitions will likely remain a viable option for the company has it works to further its growth.

Source: Investor Presentation

We project 10% EPS growth over the next five years, driven by an increase in top line revenue, modest margin expansion, and the favorable effects of acquisitions.

Competitive Advantages & Recession Performance

Nordson’s competitive advantage lies in its proprietary precision technologies. The business offers specialized and essential components used in various manufacturing processes.

This has enabled Nordson to muster an enormous installed base of customers worldwide. Due to its extensive global presence, Nordson has diversified its revenue geographically and by industry and segment.

However, this does not imply that Nordson is immune to economic downturns. Earnings decreased by -32% for the year during the Great Financial Crisis before rapidly increasing. Given the company’s reliance on global expansion, another recession could reduce its projections for near-term growth.

Valuation & Expected Returns

Nordson’s current price-to-earnings ratio is 23.9 based on our 2026 forecasted earnings-per-share of $11.30. This valuation is slightly lower than the company’s trailing decade average P/E ratio of about 24.0. Given its solid prospects, we believe that 25 times earnings is a reasonable fair value estimate for Nordson.

Given shares trade under our fair value estimate today, Nordson stock could experience a positive return of roughly 0.9% per year over the next five years from an expanding multiple.

Nordson also has a 1.2% dividend yield, which has increased yearly for 62 years. Furthermore, we forecast a payout ratio of only 29% for 2026, leaving ample room for continued increases in the years ahead.

Combining the company’s 1.2% dividend yield, our forecasted EPS growth rate of 10%, and the potential valuation tailwind, we see Nordson stock generating total returns of 12.1% per year in the intermediate term. As a result, Nordson receives a buy rating at this time.

Final Thoughts

The company’s growth prospects seem promising, and Nordson has an impressive track record of earnings and dividends. The company is currently trading at a lower level, which increases its attractiveness.

We expect that Nordson will post another record year for adjusted earnings-per-share. Moreover, we believe that Nordson will continue to grow at a high rate over the medium-term. This long-term earnings growth and the very conservative dividend payout ratio should see the company increasing its dividend for many more years ahead.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: