Updated on March 4th, 2026 by Nathan Parsh

Roper Technologies (ROP) has increased its dividend payout for 33 consecutive years, making it one of the Dividend Aristocrats.

The Dividend Aristocrats are a select group of 69 stocks in the S&P 500 that have had 25+ years of consecutive dividend increases. We believe they are among the best long-term investments in the stock market.

You can download a full list of all Dividend Aristocrats (along with important financial metrics that matter) by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

To become a Dividend Aristocrats, a company needs a strong business model, durable competitive advantages, and the ability to withstand global recessions.

The Dividend Aristocrat are high-quality dividend growth stocks. Even more appealing is Roper’s high dividend growth rate. The most recent increase was another 10% raise. This type of raise isn’t out of the ordinary as the company’s dividend has a compound annual growth rate of nearly 12% over the last decade.

Even among the Dividend Aristocrats, dividend hikes of 10% are rare, which makes Roper’s dividend increases over the last decade very impressive. This article will discuss Roper’s business, growth potential, and valuation.

Business Overview

Roper designs and develops software, including both software-as-a-service and licensed technology, and engineered products and solutions. Roper has a diverse portfolio of products and services, which it provides to a multitude of sectors, including healthcare, transportation, food, energy, water, and education.

Roper focuses on three main business segments:

- Application Software

- Network Software

- Technology Enabled Products

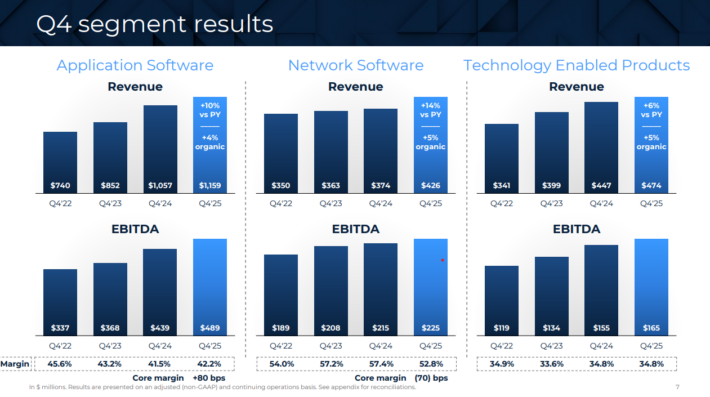

Source: Investor Presentation

The Application Software business includes Aderant, CBORD, CliniSys, Data Innovations, Deltek, Frontline, IntelliTrans, PowerPlan, Strata, and Vertafore as its main products.

The Network Software business includes its main products: ConstructConnect, DAT, Foundry, iPipeline, iTradeNetwork, Loadlink Technologies, MHA, SHP, and SoftWriters.

Finally, the Technology Enabled Products segment includes CIVCO Medical Solutions, FMI, Inovonics, IPA, Neptune, Northern Digital, rf IDEAS, and Verathon as its main products.

Roper has broadly benefited from the steady expansion of the U.S. economy over the past decade. We believe the company can maintain a positive growth trajectory for many years going forward.

Growth Prospects

Roper is uniquely positioned to generate strong growth across its business, even when the broader U.S. economy faces challenges such as inflation and geopolitical risk.

Source: Investor Presentation

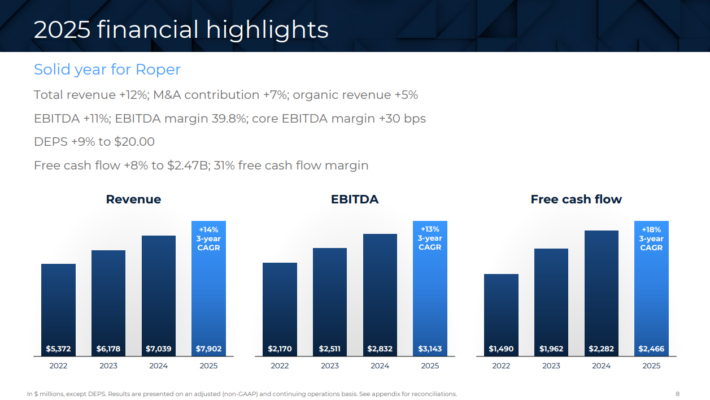

On January 27th, 2026, Roper reported its Q4 results for the period ending December 31st, 2025. Quarterly revenues and

adjusted EPS were $2.06 billion and $5.21, up 10% and 8% year-over-year, respectively. Organic growth was 4% for the period, with

acquisitions adding 5%, reflecting continued strength across Roper’s diversified software and technology portfolio.

During the quarter, the company continued to actively deploy capital, repurchasing $500 million of shares and building

on a year in which it invested $3.3 billion in strategic acquisitions including CentralReach and Subsplash, while continuing to advance AI-driven innovation across its businesses.

Management initiated full-year 2026 adjusted EPS guidance of $21.30 to $21.55. At the midpoint, this would represent 7.2% growth from 2025.

Competitive Advantages & Recession Performance

Over the past several years, Roper pursued an asset-light business model, with a specific focus on software and engineered products and services. The company adopted this strategy to expand margins, by reducing capital expenditure needs, while also generating recurring revenue.

This has resulted in much stronger cash conversion over time and is likely to further increase its cash conversion ratio moving forward.

These factors give Roper tremendous competitive advantages. Its high margins and operational efficiency provide it with ample cash flow, which can be invested to stay ahead of the competition.

Another competitive advantage that Roper has is that it is highly diversified within the technology sector. It owns ~27 independent businesses with leadership positions in niche markets. Furthermore, these end markets are quite diversified and offer strong recurring revenue and customer retention.

Investors should also note that in the past, Roper was a cyclical business. It had the capacity for very strong growth when the economy was expanding but also struggled during recessions. Earnings-per-share during the Great Recession are shown below:

- 2007 earnings-per-share of $2.68

- 2008 earnings-per-share of $3.06 (15% increase)

- 2009 earnings-per-share of $2.58 (16% decline)

- 2010 earnings-per-share of $3.34 (29% increase)

As you can see, Roper was not a highly recession-resistant company. Earnings-per-share declined 16% in 2009. If the economy were to enter a recession in the years ahead, Roper could see earnings decline.

Roper also has a tremendous dividend growth record, numbering 33 years of consecutive dividend increases. Over the past decade, DPS has grown annually by an average of 11.7%.

We have a DPS growth projection of10%, which aligns with Roper’s latest increase and is easily supported by the underlying net income. We expect Roper to grow earnings-per-share at a rate of 8% annually through 2031.

Valuation & Expected Returns

Roper is a high-quality company with strong growth prospects, thanks to the high demand for its technology. Therefore, it should not be surprising that the stock has often held a premium valuation, often in the mid- to high 20x EPS range.

But with the stock trading at ~$362 and expected earnings-per-share of $21.43 for the year, shares trade with a price-to-earnings ratio of 16.9.

We have a 2031 target price-to-earnings ratio of 19.0. If shares were to revert to this target valuation within five years, then multiple expansion would add 2.4% to annual returns over this period.

Coupled this with our earnings growth estimate of 8% and the starting yield of 1.0%, we forecast total annual return potential of 11.5% through 2031.

Final Thoughts

Roper has a high-quality business model, and 8% annual earnings-per-share growth is not an unreasonable assumption moving forward.

The stock is also a Dividend Aristocrat, and thanks to the company’s high earnings growth rate, 10%+ annual dividend increases are possible.

Roper fits the bill of a great company and the stock appears to be undervalued. We believe that the stock could provide low double-digit returns for shareholders, making it a buy.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: