Updated on July 15th, 2025 by Nathan Parsh

On October 3rd, 2024, RPM International (RPM) announced that it would increase its quarterly dividend for the 51st consecutive year.

As a result, it has joined the list of Dividend Kings.

The Dividend Kings are a select group of 55 stocks that have increased their dividends for at least 50 consecutive years. Given this longevity, we believe the Dividend Kings are among the highest-quality dividend growth stocks to buy and hold for the long term.

With this in mind, we created a full list of all 55 Dividend Kings. You can download the full list, along with important financial metrics such as dividend yields and price-to-earnings ratios, by clicking on the link below:

RPM is a diversified company and a leader in the materials sector. We believe it has a long runway of growth ahead and can continue to be relied upon for annual dividend increases.

This article will provide an overview of the company’s business, discuss its growth prospects, highlight its competitive advantages, and outline the expected returns.

Business Overview

RPM International manufactures, markets, and distributes chemical products to industrial, retail, and specialty customers. The majority of its sales are to industrial customers. Founded in 1947, RPM employs more than 17,000 people.

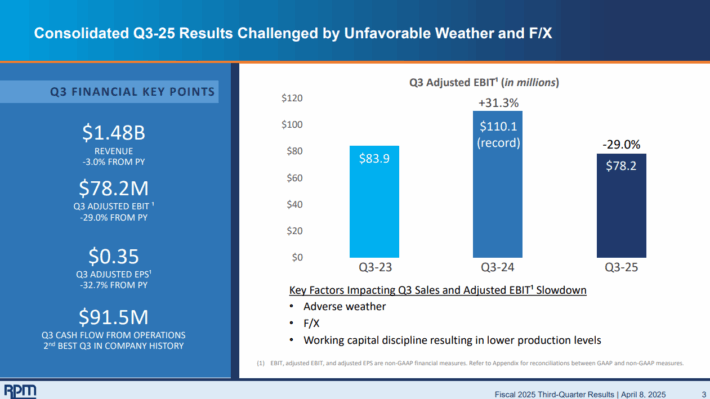

The company reported results for the third quarter of fiscal year 2025 on April 8th, 2025.

Source: Investor Presentation

Growth Prospects

In recent years, growth has been much steadier. From fiscal year 2014 to fiscal year 2024, earnings per share grew at a rate of 8.5% per year, accelerating to 12.3% over the last five years.

Factoring in the strength of recent results with the likely declines in earnings during the next recession, we now forecast annual earnings growth of 7%, up from 5%, through fiscal year 2030.

Organic revenue growth is expected to be the primary contributor. Expanding profit margins will also be key to the company’s future EPS growth.

Source: Investor Presentation

Growth slowed during the last recession, but RPM maintained and increased its dividend payments to shareholders even in an adverse economic climate.

Competitive Advantages & Recession Performance

RPM is a leading manufacturer and distributor of paints, coatings, construction chemicals, colorants, and adhesives to consumers, contractors, and construction businesses. Due to increases in construction and home improvement spending, these businesses tend to perform well during periods of economic growth.

However, RPM is very susceptible to recessions. You can see the company’s earnings-per-share performance during the Great Recession below:

- 2007 earnings-per-share of $1.64

- 2008 earnings-per-share of $0.36 (78% decline)

- 2009 earnings-per-share of $0.93 (158% increase)

- 2010 earnings-per-share of $1.39 (49% increase)

As you can see, the company’s earnings per share declined significantly in 2008 but recovered in the following two years as the economy emerged from the recession.

We expect this recession-resistant Dividend King to perform similarly during future economic downturns.

RPM is not recession-proof, as shown by its decline in earnings and the time it took for earnings growth to return following the last recession. The company also has a high level of debt that could make acquisitions or high dividend growth difficult if earnings were to weaken.

From a dividend perspective, RPM’s dividend also appears very safe.

Source: Investor Presentation

The company’s projected dividend payout ratio for 2025 is 37%. RPM has raised its dividend for 51 consecutive years.

Valuation & Expected Total Returns

Based on the expected 2025 EPS of $5.48, RPM stock trades at a price-to-earnings ratio of 20.6. We reaffirm our target P/E of 22 as this is more in line with the long-term average valuation and reflects the quality of earnings results over the past few years.

If the stock were to trade with this multiple by fiscal 2030, then valuation would be a 1.3% headwind to annual returns over this period.

The other major component of RPM’s future total returns will be the company’s earnings-per-share growth. We expect the company to achieve 7% annual EPS growth.

Lastly, the company’s dividend payments will boost total returns. RPM shares currently yield 1.8%.

In total, annual returns are projected to be 10% through fiscal year 2030. Given the company’s lengthy track record of dividend growth, sound business model, and expected returns, RPM is rated as a buy.

Final Thoughts

RPM International continues to deliver record-setting results, an impressive feat considering the company’s growth rates last fiscal year. The company also has an impressive dividend growth streak.

With expected returns of 10% annually over the next half-decade, we currently rate RPM stock a buy.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Aristocrats List: S&P 500 stocks with 25+ years of dividend increases.

- The Blue Chip Stocks List: contains stocks on either the Dividend Achievers, Dividend Aristocrats, or Dividend Kings list.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: