Updated on March 28th, 2024 by Bob Ciura

Every year, we review each of the 68 Dividend Aristocrats, the group of companies in the S&P 500 Index with 25+ consecutive years of dividend increases. We believe the Dividend Aristocrats are among the best stocks to buy and hold for the long run.

Broadly speaking, to make it on the list of Dividend Aristocrats, a company must possess a profitable business model with a valuable brand, global competitive advantages, and the ability to withstand recessions.

With this in mind, we have created a list of all 68 Dividend Aristocrats. You can download your free copy of the Dividend Aristocrats list, along with important financial metrics such as price-to-earnings ratios and dividend yields, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

McDonald’s Corporation (MCD) embodies all of the qualities inherent in a Dividend Aristocrat. McDonald’s paid its first dividend in 1976 and has increased it every year since. The company has now increased its dividend for more than four decades.

McDonald’s has implemented a successful turnaround in recent years through new menu offerings, remodeled restaurants, and accelerated investment in technology. These initiatives should help McDonald’s continue to raise its dividend for many years, although the stock appears to be overvalued today.

Business Overview

McDonald’s was founded in 1954 by Ray Kroc and his partners, Dick and Mac McDonald. Together, they formed the McDonald’s System Inc. In 1960, Kroc bought the exclusive rights to the McDonald’s name. Today, McDonald’s operates approximately 39,000 locations in more than 100 countries worldwide.

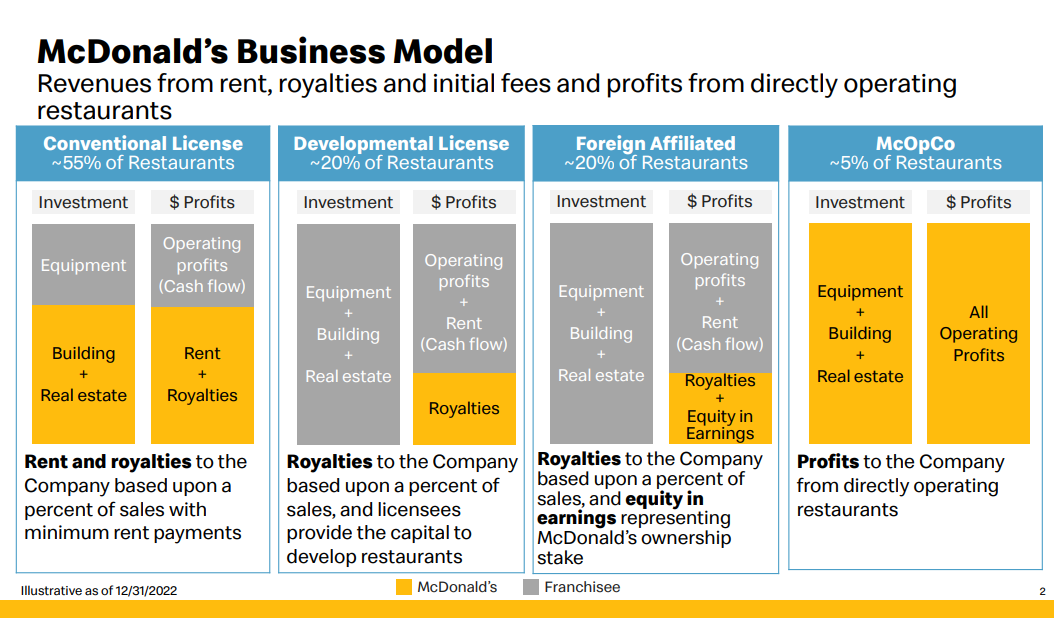

Revenues come primarily from franchise fees. McDonald’s has accelerated its franchising over the past several years. While this effort initially led to lower sales, it allowed McDonald’s to expand its profitability through higher margins. And with the franchising efforts lapped, McDonald’s is back to reporting impressive sales growth in addition to earnings growth.

Source: Investor Presentation

On February 5th, McDonald’s reported Q4 2023 results. For the quarter, total revenue came in at $6.40 billion, a +8% increase compared to Q4 2022 on a 6% rise in system-wide sales adjusting for currency headwinds. Revenue climbed 12% at company-owned stores, while revenue increased 6% at franchised restaurants.

Diluted earnings climbed 8% to $2.80 per share compared to $2.59 per share in comparable periods on higher sales offset by pre-tax charges and impairments. On a geographic basis, sales increased +4.3% in the US, +4.4% in the international markets, and +0.7% in the international developmental licensed markets.

For the year, revenue rose 10% to $25.5B from $23.2B while diluted EPS was up 38% to $11.56 from $8.33.

Growth Prospects

McDonald’s performance has improved in the past few years due mainly to the strategic initiatives put in place to restore growth. These initiatives are working well and put McDonald’s in an excellent position to continue growing moving forward.

For example, it has partnered with third-party delivery services such as Uber (UBER) Eats and GrubHub (GRUB), while it also recently acquired voice technology firm Apprente. Apprente makes artificial intelligence technology to provide faster and more accurate fulfillment of drive-through orders. McDonald’s has also rolled out mobile ordering and kiosks at many of its restaurants to simplify the ordering process even further.

The company generates lower revenue now (sales peaked at $28 billion in 2013) but its costs are lower, increasing margins. McDonald’s is now asset-light and low-cost, collecting franchise and real estate fees from thousands of restaurants. This strategy has been successful, with earnings per share growing at a strong pace.

McDonald’s continues to perform better than many of its peers when it comes to generating rising revenues from existing restaurants. Earnings per share growth should be driven by higher sales, declining operating costs, new restaurants, and share repurchases.

We expect McDonald’s to generate 6% annual earnings-per-share growth over the next five years.

Competitive Advantages & Recession Performance

McDonald’s enjoys several competitive advantages that separate it from its industry peers. First, it is the largest publicly-traded fast-food company in the world. It has an enormous scale, which allows it to keep prices low. And it has one of the most valuable and widely-recognized brands worldwide.

One of the big reasons why McDonald’s continues to increase its dividend each year is because it has a defensive business model. When the economy takes a downturn, consumers tighten their belts, particularly when it comes to dining.

Rather than go to higher-priced sit-down restaurants, consumers will often shift down to fast food during a recession.

McDonald’s earnings-per-share during the Great Recession are shown below:

- 2007 earnings-per-share of $2.91

- 2008 earnings-per-share of $3.67 (26% increase)

- 2009 earnings-per-share of $3.98 (8% increase)

- 2010 earnings-per-share of $4.60 (16% increase)

McDonald’s grew earnings each year of the recession at a double-digit compound annual rate. This is highly impressive and speaks to its recession-resistant business model.

Investors can be reasonably assured the company can continue raising the dividend, even if another recession hits. The company has increased its dividend for 49 consecutive years.

Valuation & Expected Returns

Using the current share price of ~$283 and expected earnings-per-share for 2024 of $12.44, the stock has a price-to-earnings ratio of 22.7.

Over the past decade, shares of McDonald’s have held an average P/E ratio of 21. This is our fair value estimate for MCD stock. Therefore, McDonald’s appears to be overvalued, based on relative comparisons to the broader market and its own historical average.

If MCD shares decline to a P/E of 21 over the next five years, it would reduce annual returns by 1.5% per year.

Fortunately, the impact of overvaluation will be offset by earnings-per-share growth and dividends. In addition to the expected EPS growth of 6% per year, the stock also offers a current dividend yield of 2.3%.

Overall, McDonald’s is expected to generate total returns of 6.8% per year, which makes the stock a hold in our view.

Final Thoughts

McDonald’s has paid a rising dividend for 49 years in a row. Over the decades, it has had to reinvent itself from time to time to stay on top of changing trends in the restaurant industry. But it has consistently succeeded in its various turnarounds, a testament to the strength of its brand and business model.

That said, investors aren’t likely to see sizable gains with the stock’s high valuation. As a result, we believe investors should wait for a pullback before buying McDonald’s.

If you are interested in finding high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings List: considered to be the best-of-the-best among dividend growth stocks, the Dividend Kings are a group of exceptional dividend stocks with 50+ years of consecutive dividend increases.

- The Blue Chip Stocks List: contains stocks on either the Dividend Achievers, Dividend Aristocrats, or Dividend Kings list.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: