Updated on August 3rd, 2026 by Nikolaos Sismanis

With contributions from Ben Reynolds

Monthly dividend stocks are securities that pay a dividend every month instead of quarterly or annually.

This research report focuses on all 122 individual monthly paying securities. It includes the following resources.

Resource #1: The Monthly Dividend Stock Spreadsheet List

This list contains important metrics, including: dividend yields, payout ratios, buy/hold/sell ratings, fair value prices, expected total returns, and much more.

Note: We strive to maintain an accurate list of all monthly dividend payers. There’s no universal source we are aware of for monthly dividend stocks; we curate this list manually. If you know of any stocks that pay monthly dividends that are not on our list, please email support@suredividend.com.

Resource #2: Sure Analysis Reports On All Monthly Dividend Stocks

We cover all monthly dividend stocks in the Sure Analysis Research Database. Most securities are updated quarterly. This resource has links to our most recent stand-alone analysis on each of these monthly dividend paying securities.

Resource #3: The 10 Best Monthly Dividend Stocks

This research report analyzes the 10 best monthly dividend stocks as ranked by expected total return.

Resource #4: Other Monthly Dividend Stock Research

– Why monthly dividends matter

– The dangers of investing in monthly dividend stocks

– Final thoughts and other income investing resources

Sure Analysis Reports On All Monthly Dividend Stocks

You can see detailed analysis on the individual monthly dividend securities we cover by clicking the links below:

- Agree Realty (ADC)

- AGNC Investment (AGNC)

- Atrium Mortgage Investment Corporation (AMIVF)

- Apple Hospitality REIT, Inc. (APLE)

- Automotive Properties Real Estate Investment Trust (APPTF)

- Allied Properties Real Estate Investment Trust (APYRF)

- ARMOUR Residential REIT (ARR)

- Banco BBVA Argentina S.A. (BBAR)

- Banco Bradesco S.A. (BBD)

- BCP Investment Corp. (BCIC)

- Diversified Royalty Corp. (BEVFF)

- Bird Construction (BIRDF)

- Banco Macro S.A. (BMA)

- Boardwalk Real Estate Investment Trust (BOWFF)

- Boston Pizza Royalties Income Fund (BPZZF)

- Bridgemarq Real Estate Services (BREUF)

- BSR Real Estate Investment Trust (BSRTF)

- BTB Real Estate Investment Trust (BTBIF)

- Canadian Apartment Properties REIT (CDPYF)

- Cardinal Energy Ltd. (CRLFF)

- ChemTrade Logistics Income Fund (CGIFF)

- CION Investment Corporation (CION)

- Canadian Net REIT (CNNRF)

- Chiron Real Estate (XRN)

- Choice Properties REIT (PPRQF)

- Crombie Real Estate Investment Trust (CROMF)

- Cross Timbers Royalty Trust (CRT)

- Capital Southwest Corp. (CSWC)

- CT Real Estate Investment Trust (CTRRF)

- Chartwell Retirement Residences (CWSRF)

- SmartCentres Real Estate Investment Trust (CWYUF)

- Decisive Dividend Corp. (DEDVF)

- Dynacor Group Inc (DNGDF)

- Dream Office REIT (DRETF)

- Dream Industrial REIT (DREUF)

- Dynex Capital (DX)

- Ellington Residential Mortgage REIT (EARN)

- Ellington Financial (EFC)

- Nexus Industrial REIT (EFRTF)

- EPR Properties (EPR)

- Exchange Income (EIFZF)

- Extendicare Inc. (EXETF)

- Fibra Mty (FMTYF)

- Four Corners REIT (FCPT)

- Freehold Royalties Ltd. (FRHLF)

- Firm Capital Mortgage Investment Trust (FCMGF)

- First Capital Real Estate Investment Trust (FCXXF)

- Firm Capital Property Trust (FRMUF)

- Flagship Communities REIT (MHCUF)

- Fortitude Gold (FTCO)

- Gladstone Capital Corporation (GLAD)

- Gladstone Commercial Corporation (GOOD)

- Gladstone Investment Corporation (GAIN)

- Gladstone Land Corporation (LAND)

- Global Water Resources (GWRS)

- Granite Real Estate Investment Trust (GRTUF)

- Grupo Aval Acciones y Valores S.A. (AVAL)

- Grupo Financiero Galicia S.A. (GGAL)

- Gamehost Inc. (GHIFF)

- GO Residential REIT (GONYF)

- Healthpeak Properties (DOC)

- H&R Real Estate Investment Trust (HRUFF)

- Horizon Technology Finance (HRZN)

- Himalaya Shipping Ltd. (HSHP)

- InPlay Oil Corp. (IPOOF)

- Itaú Unibanco (ITUB)

- Invesco Mortgage Capital (IVR)

- Janus Living (JAN)

- K-Bro Linen Inc. (KBRLF)

- Killam Apartment REIT (KMMPF)

- LTC Properties (LTC)

- Sienna Senior Living (LWSCF)

- Main Street Capital (MAIN)

- Mesa Royalty Trust (MTR)

- Modiv Inc. (MDV)

- Morguard Real Estate Investment Trust (MGRUF)

- Minto Apartment REIT (MIAPF)

- Mullen Group Ltd. (MLLGF)

- Morguard North American REIT (MNARF)

- MSC Income Fund (MSIF)

- Northland Power Inc. (NPIFF)

- Northview Residential REIT (NRRUF)

- Olympia Financial Group (OLYFF)

- Orchid Island Capital (ORC)

- Oxford Square Capital (OXSQ)

- Plaza Retail REIT (PAZRF)

- Permian Basin Royalty Trust (PBT)

- Phillips Edison & Company (PECO)

- Pennant Park Floating Rate (PFLT)

- Peyto Exploration & Development Corp. (PEYUF)

- Pine Cliff Energy Ltd. (PIFYF)

- Primaris REIT (PMREF)

- PennantPark Investment Corporation (PNNT)

- Paramount Resources Ltd. (PRMRF)

- PermRock Royalty Trust (PRT)

- Pro Real Estate Investment Trust (PRVFF)

- Prospect Capital Corporation (PSEC)

- Petrus Resources Ltd. (PTRUF)

- Permianville Royalty Trust (PVL)

- Pizza Pizza Royalty Corp. (PZRIF)

- Realty Income (O)

- Richards Group Inc. (RPKIF)

- RioCan Real Estate Investment Trust (RIOCF)

- Saratoga Invesmtent Corp. (SAR)

- Sabine Royalty Trust (SBR)

- Stellus Capital Investment Corp. (SCM)

- Savaria Corp. (SISXF)

- San Juan Basin Royalty Trust (SJT)

- Sir Royalty Income Fund (SIRZF)

- SmartStop Self Storage REIT (SMA)

- Source Rock Royalties Ltd. (SRRRF)

- Slate Grocery REIT (SRRTF)

- Stag Industrial (STAG)

- Surge Energy Inc. (ZPTAF)

- Timbercreek Financial Corp. (TBCRF)

- Trinity Capital (TRIN)

- True North Commercial REIT (TUERF)

- Telefonica Brasil S.A. (VIV)

- UDR, Inc. (UDR)

- U.S. Global Investors (GROW)

- Vital Industries Property Trust (NWHUF)

- Whitecap Resources Inc. (WCPRF)

The 10 Best Monthly Dividend Stocks

This research report examines the 10 monthly dividend stocks from our Sure Analysis Research Database that match the following criteria:

- Sort by Dividend Risk Score (safest first)

- Rank by expected total return (highest first)

- All expected total returns must be 5.5% or higher

- Qualitative exclusions from this Top 10 list apply

Example: The #1 ranked stock in this article will be the highest expected total return monthly dividend payer from the safest Dividend Risk cohort of monthly dividend payers.

Use the table below to quickly jump to analysis on any of the top 10 best monthly dividend stocks.

Top 10 Monthly Dividend Stocks Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- Monthly Dividend Stock #10: Saratoga Investment Corp. (SAR)

- Monthly Dividend Stock #9: Morguard North American Residential REIT (MNARF)

- Monthly Dividend Stock #8: Grupo Aval Acciones y Valores (AVAL)

- Monthly Dividend Stock #7: Agree Realty Corporation (ADC)

- Monthly Dividend Stock #6: UDR, Inc. (UDR)

- Monthly Dividend Stock #5: Savaria Corporation (SISXF)

- Monthly Dividend Stock #4: Boardwalk Real Estate Investment Trust (BOWFF)

- Monthly Dividend Stock #3: Realty Income Corporation (O)

- Monthly Dividend Stock #2: Dynacor Group (DNGDF)

- Monthly Dividend Stock #1: Bird Construction Inc. (BIRDF)

Monthly Dividend Stock #10: Saratoga Investment Corp. (SAR)

- 5-Year Expected Total Return: 18.6%

- Dividend Risk Score: F

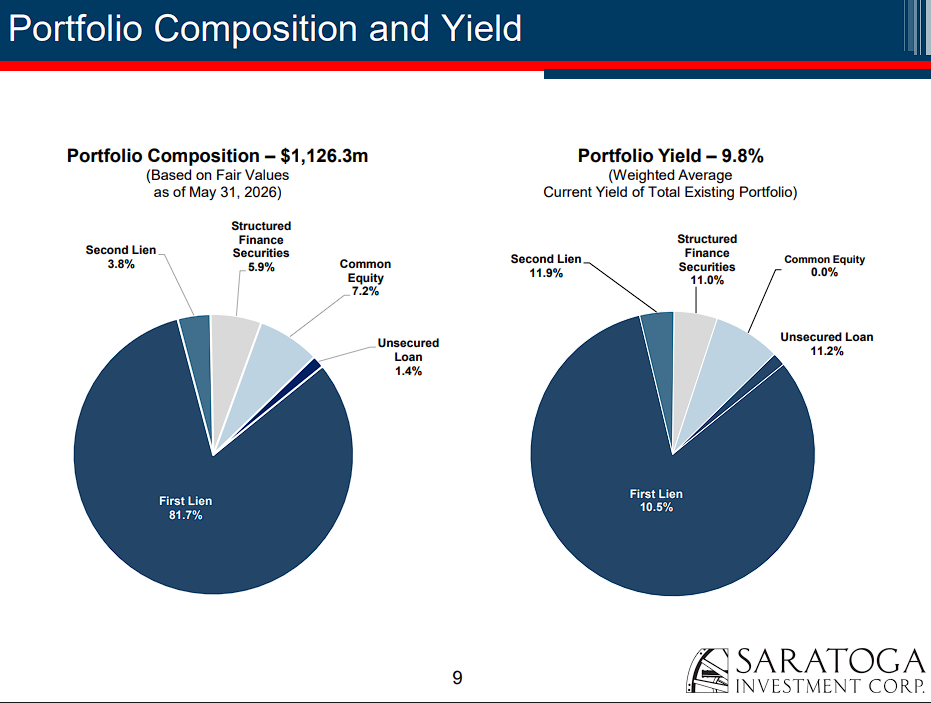

Saratoga Investment Corp. is a business development company that lends primarily to U.S. middle-market businesses.

Its portfolio is concentrated in first-lien loans, with smaller allocations to second-lien debt, unsecured loans, structured-finance securities, and equity investments.

This structure can generate substantial income, but credit losses, leverage, and declining short-term rates can pressure results.

For the fiscal first quarter of 2027, ended May 31st, 2026, total investment income was $30.8 million, while net investment income declined to $7.6 million, or $0.47 per share, from $0.66 per share one year earlier.

Assets under management increased 1.6% sequentially to $1.126 billion, aided by $31 million of net originations.

However, net asset value fell to $23.23 per share from $24.42 at the prior quarter-end, reflecting portfolio markdowns.

Saratoga declared three monthly dividends of $0.25 per share for its fiscal second quarter, maintaining the $0.75 aggregate base dividend established when it adopted monthly payments in 2025.

Still, quarterly NII covered only about 63% of that amount.

Non-accruals were zero at fair value, but the high yield, weaker coverage, and NAV erosion explain the F Dividend Risk Score.

You may treat the projected return as compensation for elevated dividend and credit risk.

Monthly Dividend Stock #9: Morguard North American Residential REIT (MNARF)

- 5-Year Expected Total Return: 5.9%

- Dividend Risk Score: D

Morguard North American Residential REIT owns 43 apartment properties containing 13,089 suites in Canada and the United States.

Geographic diversification and generally resilient apartment demand support recurring cash flow, although occupancy, operating expenses, financing costs, and currency movements can influence results.

In the second quarter of 2026, net operating income declined 4.7% to C$54.2 million. Basic funds from operations fell 10.6% to C$0.42 per unit, as lower occupancy and higher costs outweighed rent growth.

Canadian occupancy was 91.4%, compared with 95.2% a year earlier, while U.S. occupancy was 92.8%, versus 94.8%.

Average monthly rent still increased 3.5% in Canada and 1.8% in the U.S.

The REIT ended the quarter with C$304 million of liquidity and a debt-to-gross-book-value ratio of 40.0%.

Morguard pays C$0.06583 per unit monthly, or C$0.78996 annualized.

Second-quarter distributions consumed 46.8% of FFO, providing a meaningful coverage cushion despite weaker operating results.

A planned roughly C$1 billion investment for an approximately 20% interest in up to 106 multifamily properties could materially expand the platform during the second half of 2026.

The transaction also increases execution and financing risk, making balance-sheet discipline particularly important for the dividend outlook.

Monthly Dividend Stock #8: Grupo Aval Acciones y Valores (AVAL)

- 5-Year Expected Total Return: 6.1%

- Dividend Risk Score: D

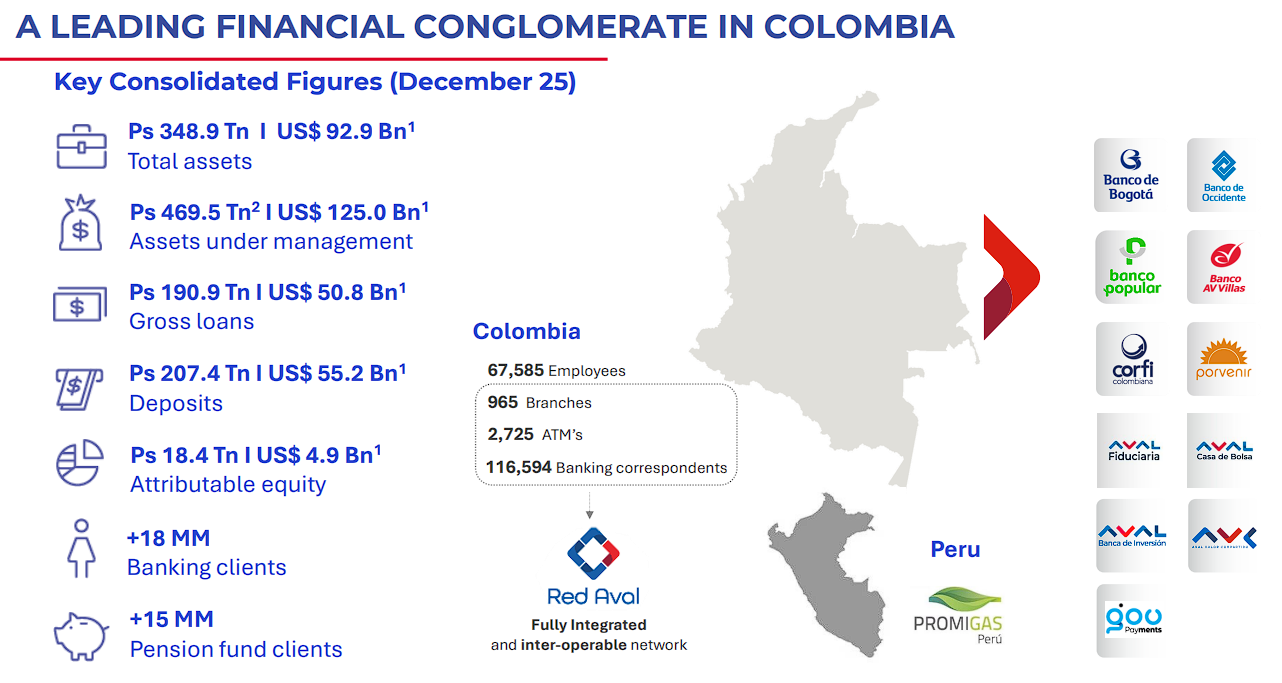

Grupo Aval Acciones y Valores is one of Colombia’s largest financial groups.

Through its banking subsidiaries and Corficolombiana, it provides commercial and consumer banking, pensions, investment banking, infrastructure, and other financial services.

Its earnings are sensitive to Colombian interest rates, credit quality, economic growth, regulation, and currency movements.

For the first quarter of 2026, attributable net income was COP336.6 billion, or COP14.2 per share, down 6.9% year over year.

Results included a one-time equity tax that reduced attributable profit by COP210.1 billion. Reported return on average equity was 7.4%, but management calculated 12.0% excluding that charge.

Gross loans grew 6.0% from the prior year, deposits increased 11.7%, and the 90-day past-due-loan ratio improved 69 basis points to 3.13%.

Total net interest margin was 3.34%, including a 4.15% banking margin.

Shareholders approved a monthly dividend of COP2.65 per share from April 2026 through March 2027.

That rate is level in Colombian pesos, even though the U.S.-dollar value received by ADR holders can fluctuate with exchange rates.

The payout represented about 39% of the database’s projected 2026 earnings, but Colombia’s economic volatility and the group’s capital-intensive financial operations support the D Dividend Risk Score.

Investors should monitor normalized profitability and asset quality rather than interpreting FX-driven dividend changes as policy changes.

Monthly Dividend Stock #7: Agree Realty Corporation (ADC)

- 5-Year Expected Total Return: 8.7%

- Dividend Risk Score: D

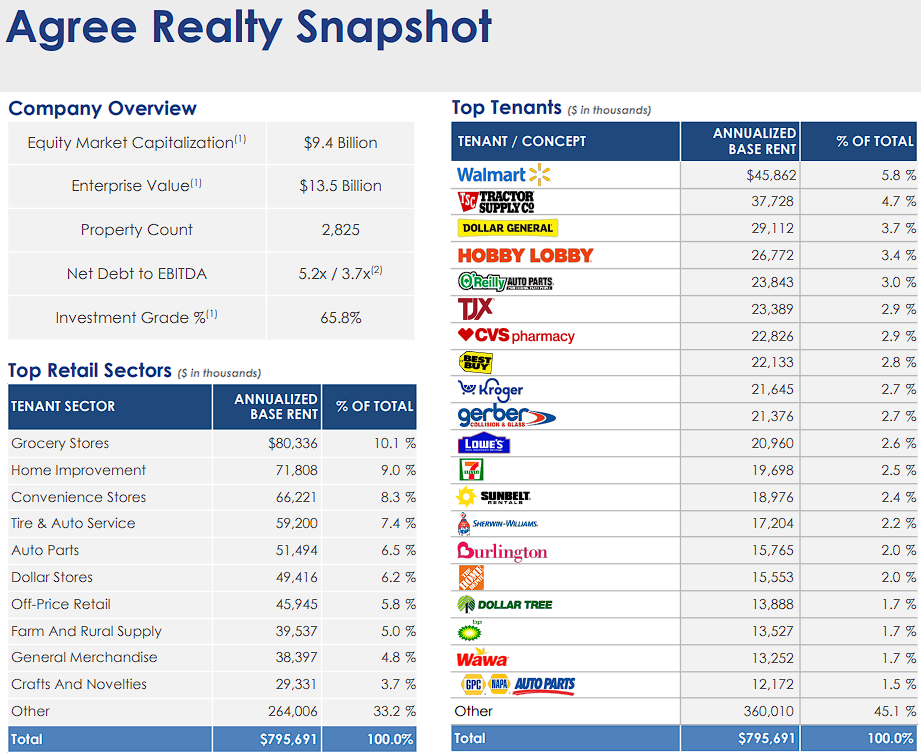

Agree Realty Corporation is a net-lease REIT focused on freestanding retail properties leased to large, creditworthy tenants.

Long lease terms and tenant responsibility for most property-level expenses produce relatively predictable cash flow, while acquisition spreads, tenant health, and the cost of capital are central to growth.

In the second quarter of 2026, net income rose 11.5% to $52.8 million, or $0.44 per share.

Core FFO increased 17.3% to $136 million, while AFFO also advanced 17.3% to $138 million. On a per-share basis, AFFO grew 7.4% to $1.14.

Agree invested a record of about $925 million during the first half of the year across 187 properties and ended the quarter with roughly $1.9 billion of liquidity.

Management raised full-year AFFO guidance to $4.57 to $4.59 per share and its investment-volume outlook to $1.6 billion to $1.8 billion.

The monthly dividend is $0.267 per share, equal to $3.204 annually and 4.3% above the year-earlier rate.

The payout consumed about 70% of quarterly AFFO, leaving reasonable coverage for a REIT.

Agree’s acquisition pipeline and liquidity support continued growth, but rapid capital deployment must remain accretive after financing costs.

The D Dividend Risk Score also reflects the structural sensitivity of REIT valuations and cash flows to interest rates and capital-market access.

Monthly Dividend Stock #6: UDR, Inc. (UDR)

- 5-Year Expected Total Return: 11.0%

- Dividend Risk Score: D

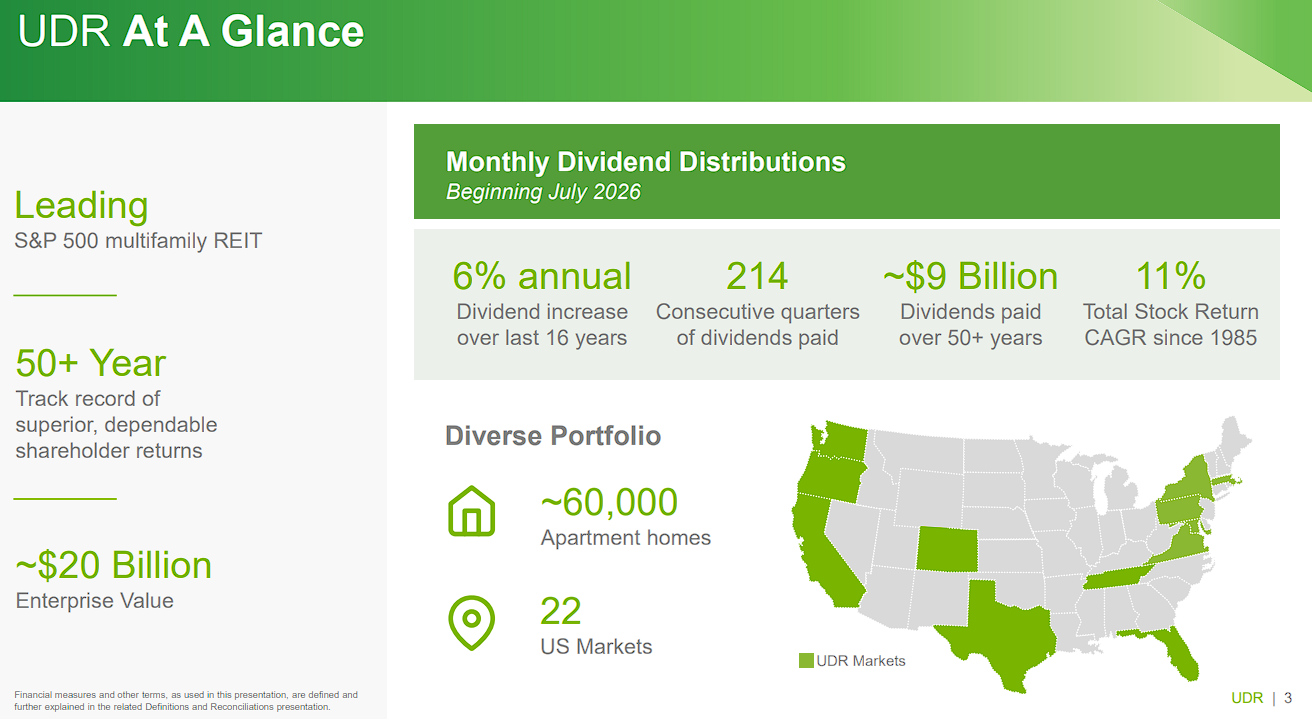

UDR, Inc. is a large apartment REIT with communities in many of the most attractive U.S. coastal and Sunbelt markets.

Its scale, operating platform, and geographically diversified portfolio support recurring rental income, while supply growth, affordability, resident turnover, and interest rates influence near-term performance.

For the second quarter of 2026, net income was $0.21 per share, up from $0.11 a year earlier.

FFO was $0.60 per share, compared with $0.61, while FFO as adjusted held steady at $0.64.

Same-store revenue increased 1.8%; expenses rose 2.6%; and net operating income advanced 1.4%.

Management raised the midpoint of full-year FFOA guidance by $0.01 to a range of $2.49 to $2.57 per share and lifted its same-store NOI growth midpoint by 50 basis points.

UDR also repurchased 5.5 million shares for $200.3 million during the quarter.

Beginning in July 2026, UDR changed its payment schedule from quarterly to monthly without altering the annualized dividend.

The current rate is $0.145 per month, or $1.74 per year, 1.2% above the prior-year amount.

This equals roughly 68% of projected FFOA, a manageable REIT payout.

More than five decades of dividend payments are reassuring, though modest operating growth and sensitivity to apartment-market conditions warrant the D Dividend Risk Score.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on UDR, Inc. (UDR).

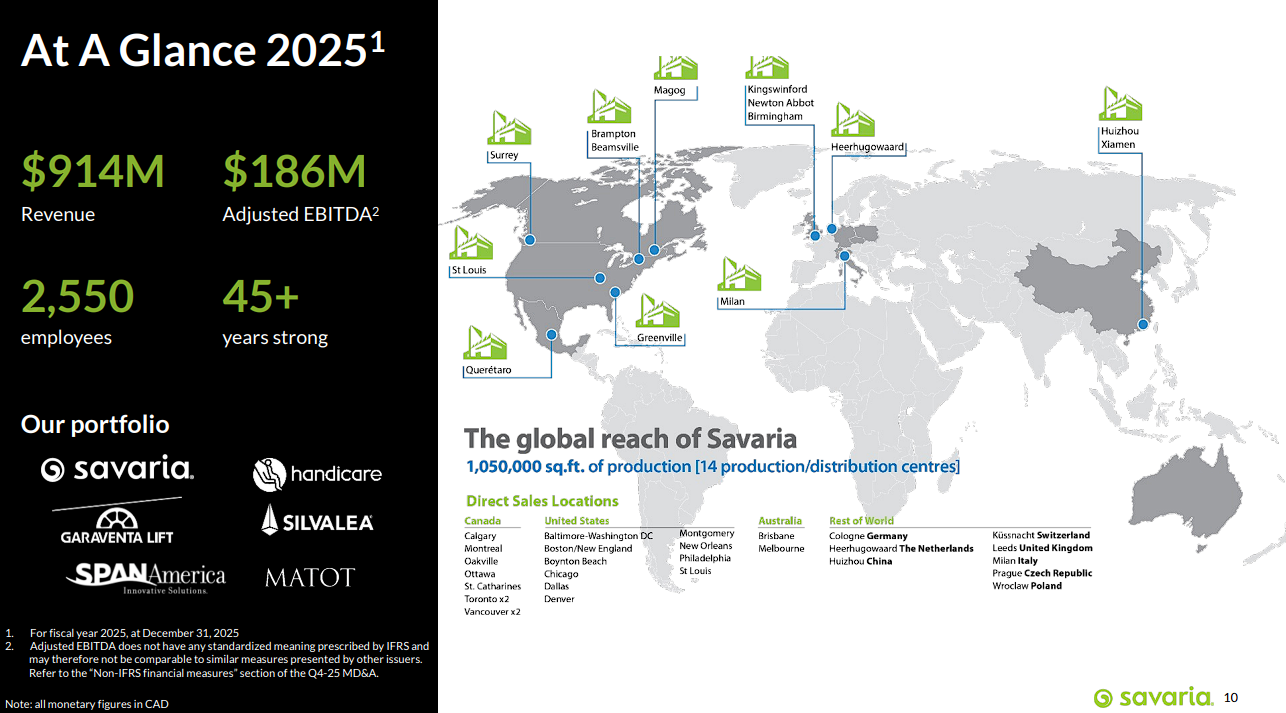

Monthly Dividend Stock #5: Savaria Corporation (SISXF)

- 5-Year Expected Total Return: 5.8%

- Dividend Risk Score: C

Savaria Corporation designs and manufactures accessibility products, including stairlifts, home elevators, wheelchair lifts, and patient-handling equipment.

An aging global population provides a favorable long-term demand backdrop, while acquisitions and manufacturing integration are important elements of its growth strategy.

First-quarter 2026 revenue increased 7.0% to C$235.5 million, including 5.7% organic growth. Accessibility revenue rose 7.9%, and Patient Care revenue grew 3.8%.

Gross margin improved 110 basis points to 38.9%, helping adjusted EBITDA rise 18.4% to C$48.1 million.

Adjusted EBITDA margin expanded 190 basis points to 20.4%, while net earnings climbed to C$22.7 million, or C$0.31 per share, from C$12.5 million, or C$0.17. Net leverage remained modest at 0.92 times.

Savaria’s latest monthly dividend is C$0.0467 per share, equivalent to approximately C$0.56 annualized.

The payout is about 41% of projected earnings, providing room to absorb normal volatility and fund growth.

In July, Savaria acquired Italy-based Vipal, which generated approximately C$13.3 million of trailing revenue and adds European elevator manufacturing capacity.

The transaction expands the addressable market but introduces integration risk.

For U.S. investors, changes in the translated dividend can reflect Canadian-dollar exchange rates even when the declared local-currency payment remains stable.

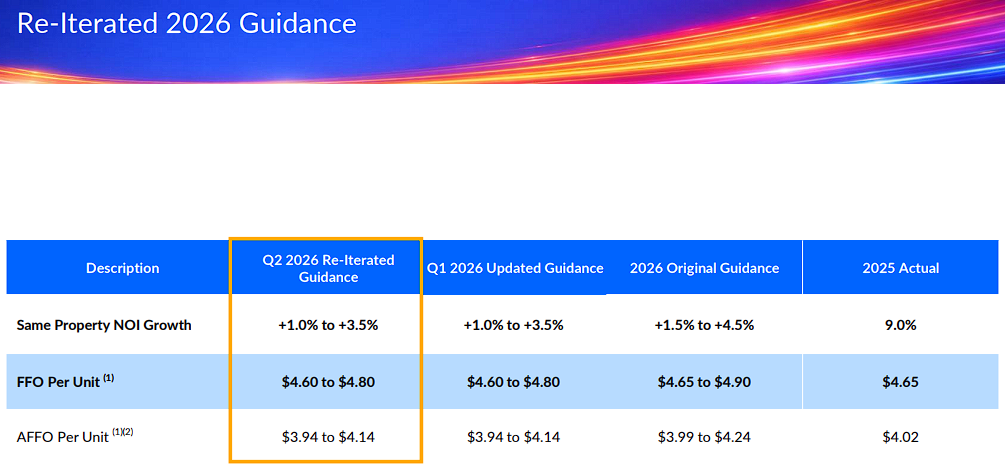

Monthly Dividend Stock #4: Boardwalk Real Estate Investment Trust (BOWFF)

- 5-Year Expected Total Return: 9.0%

- Dividend Risk Score: C

Boardwalk Real Estate Investment Trust owns and operates apartment communities across Canada, with its largest exposure in Alberta.

The REIT benefits from scale, high occupancy, and recurring residential demand, but regional supply, rent affordability, operating costs, and interest rates can affect results.

In the second quarter of 2026, net operating income rose 2.9% to C$107.2 million.

Funds from operations increased 2.6% to C$1.19 per unit, and the operating margin improved 40 basis points to 66.6%.

Same-property revenue and NOI grew 1.7%, with portfolio occupancy of 97.0%. For the first half, FFO per unit advanced 5.0% to C$2.33.

Management reaffirmed 2026 FFO guidance of C$4.60 to C$4.80 per unit and same-property NOI growth of 1.0% to 3.5%.

Boardwalk raised its monthly distribution 11.1% beginning in March 2026 to C$0.15 per unit, or C$1.80 annualized.

The payout remains below 40% of projected FFO, providing unusually strong coverage for a REIT.

Management is also recycling capital, as it sold nine non-core communities for C$222 million and repurchased more than three million units through July.

These actions can improve per-unit value when executed well, although investors should weigh acquisition and financing decisions against the security of the distribution.

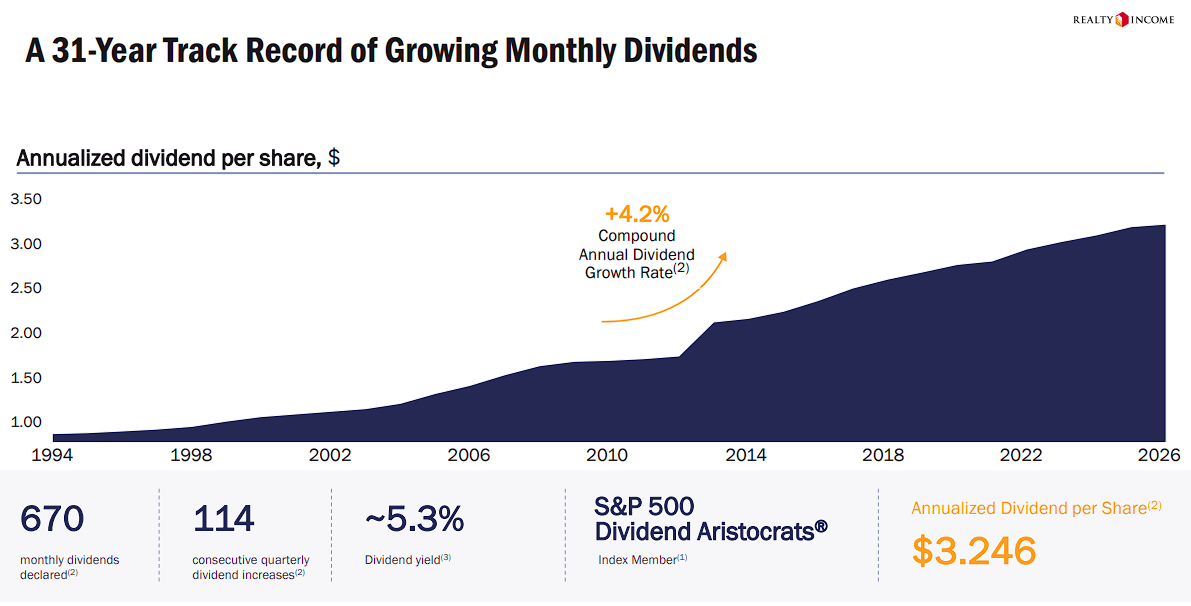

Monthly Dividend Stock #3: Realty Income Corporation (O)

- 5-Year Expected Total Return: 9.8%

- Dividend Risk Score: C

Realty Income Corporation is a diversified net-lease REIT with more than 15,500 properties across the United States and Europe.

Its tenants generally pay property-level taxes, insurance, and maintenance, producing durable cash flow from long leases.

Scale, tenant diversification, and access to multiple capital sources are important competitive advantages.

In the first quarter of 2026, revenue rose to $1.55 billion from $1.38 billion.

Net income increased to $311.8 million, or $0.33 per share, while AFFO per share grew 6.6% to $1.13.

Realty Income invested $2.8 billion at a 7.1% initial cash yield, maintained 98.9% occupancy, and recaptured 103.4% of expiring rent on re-leased properties.

Net debt to annualized pro forma EBITDAre was 5.2 times.

The company also formed a programmatic data-center joint venture after quarter-end, broadening its opportunity set while limiting direct balance-sheet concentration through institutional capital.

The current monthly dividend is $0.271 per share, or $3.252 annualized.

Realty Income has declared 673 consecutive monthly dividends and increased its dividend for 32 consecutive years.

First-quarter dividends consumed 71.7% of AFFO, a sound level for a net-lease REIT.

The C Dividend Risk Score reflects this strong record and coverage, balanced against leverage, interest-rate sensitivity, and the capital required to sustain acquisition-led growth.

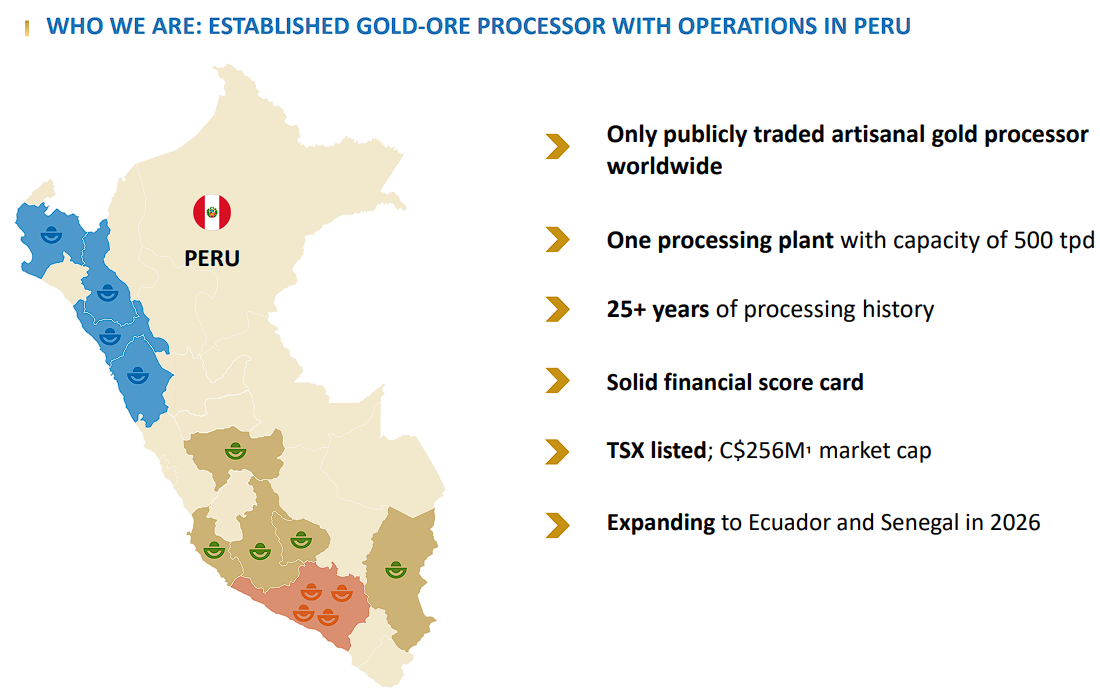

Monthly Dividend Stock #2: Dynacor Group (DNGDF)

- 5-Year Expected Total Return: 14.2%

- Dividend Risk Score: B

Dynacor Group is a Canadian gold-ore processor that purchases ore from artisanal and small-scale miners, primarily in Peru, and processes it at the Veta Dorada plant.

Because Dynacor does not operate mines, growth depends on sourcing sufficient ore, maintaining processing margins, and expanding its model into additional jurisdictions.

First-quarter 2026 revenue surged 92.6% to a record $154.1 million, driven by stronger gold prices and higher sales volumes.

Gold-equivalent production increased to 32,791 ounces from 27,050 ounces.

Net income rose to a record $7.3 million, or $0.17 per share, from $5.1 million, or $0.13 per share, while EBITDA increased to $13.6 million from $7.3 million.

Cash and short-term investments totaled $31 million at quarter-end, supporting expansion spending without excessive leverage.

Dynacor pays C$0.01333 per share monthly, equivalent to C$0.16 annually.

The payout is only about 20% of projected earnings, giving the dividend a wide coverage margin, although gold prices and ore-supply economics remain important risks.

The company is commissioning a pilot plant in Senegal and targets initial production from its Svetlana facility in Ecuador during the fourth quarter.

These projects could diversify earnings beyond Peru, but successful ramp-ups will be essential.

U.S.-dollar payments can vary or appear lower with exchange rates even when the Canadian-dollar dividend is unchanged or growing.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on Dynacor Group (DNGDF).

Monthly Dividend Stock #1: Bird Construction Inc. (BIRDF)

- 5-Year Expected Total Return: 10.9%

- Dividend Risk Score: A

Bird Construction Inc. is a Canadian construction and infrastructure-services company serving industrial, institutional, commercial, and civil markets.

Its broad project mix, recurring service work, and national operating footprint reduce dependence on any single end market, although project execution, labor availability, and input costs remain key risks.

First-quarter 2026 revenue increased 9.2% to C$783.4 million. Net income rose 21.5% to C$11.4 million, or C$0.21 per share, while adjusted earnings advanced 8.1% to C$13.9 million, or C$0.25 per share.

Adjusted EBITDA grew to C$37.1 million from C$34.1 million. Most importantly for future visibility, contracted backlog reached a record C$5.4 billion, up 23.8% year over year, and pending backlog was C$5.6 billion.

In July, Bird announced about C$1 billion of additional awards and agreements across Canada.

Bird pays a monthly dividend of C$0.07 per share, or C$0.84 annualized.

The projected payout ratio is approximately 33%, leaving substantial room for reinvestment and normal construction-cycle volatility.

The company also completed a C$250 million senior-note placement and received an inaugural investment-grade credit rating, strengthening financial flexibility as backlog expands.

The conservative payout, earnings growth, and improving project visibility support Bird’s A Dividend Risk Score.

For U.S. investors, the translated dividend will fluctuate with the Canadian dollar even when the local payment is unchanged.

Other Monthly Dividend Stock Resources

Why Monthly Dividends Matter

Monthly dividend payments are beneficial for one group of investors in particular; retirees who rely on dividend stocks for income.

With that said, monthly dividend stocks are better under all circumstances (everything else being equal), because they allow for returns to be compounded on a more frequent basis. More frequent compounding results in better total returns, particularly over long periods of time.

Consider the following performance comparison:

Over the long run, monthly compounding generates slightly higher returns over quarterly compounding. Every little bit helps.

With that said, it might not be practical to manually re-invest dividend payments on a monthly basis. It is more feasible to combine monthly dividend stocks with a dividend reinvestment plan to dollar cost average into your favorite dividend stocks.

The last benefit of monthly dividend stocks is that they allow investors to have – on average – more cash on hand to make opportunistic purchases. A monthly dividend payment is more likely to put cash in your account when you need it versus a quarterly dividend.

The Dangers of Investing In Monthly Dividend Stocks

Monthly dividend stocks have characteristics that make them appealing to do-it-yourself investors looking for a steady stream of income. Typically, these are retirees and people planning for retirement.

Investors should note many monthly dividend stocks are highly speculative. On average, monthly dividend stocks tend to have elevated payout ratios. An elevated payout ratio means there’s less margin for error to continue paying the dividend if business results suffer a temporary (or permanent) decline.

As a result, we have real concerns that many monthly dividend payers will not be able to continue paying rising dividends in the event of a recession.

Additionally, a high payout ratio means that a company is retaining little money to invest for future growth. This can lead management teams to aggressively leverage their balance sheet, fueling growth with debt. High debt and a high payout ratio is perhaps the most dangerous combination around for a potential future dividend reduction.

With that said, there are a handful of high-quality monthly dividend payers around. Realty Income (O) is an excellent example. Realty Income has paid increasing dividends (on an annual basis) every year since 1994.

The Realty Income example shows that there are high-quality monthly dividend payers around, but they are the exception rather than the norm. We suggest investors do ample due diligence before buying into any monthly dividend payer.

Final Thoughts & Other Income Investing Resources

Financial freedom is achieved when your passive investment income exceeds your expenses. But the sequence and timing of your passive income investment payments can matter.

Monthly payments make matching portfolio income with expenses easier. Most personal expenses recur monthly whereas most dividend stocks pay quarterly. Investing in monthly dividend stocks matches the frequency of portfolio income payments with the normal frequency of personal expenses.

Additionally, many monthly dividend payers offer investors high yields. The combination of a monthly dividend payment and a high yield should be especially appealing to income investors.

But not all monthly dividend payers offer the safety that income investors need. A monthly dividend is better than a quarterly dividend, but not if that monthly dividend is reduced soon after you invest. The high payout ratios and shorter histories of most monthly dividend securities mean they tend to have elevated risk levels.

Because of this, we advise investors to look for high-quality monthly dividend payers with reasonable payout ratios, trading at fair or better prices.

Additionally, see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- 20 Highest Yielding Monthly Dividend Stocks

- Dividend Kings: 50+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- High Dividend Stocks: 4%+ dividend yields