Updated on April 15th, 2026 by Nathan Parsh

Bridgemarq Real Estate Services (BREUF) has two appealing investment characteristics:

#1: It is a high-yield stock based on its 9.9% dividend yield.

Related: List of 5%+ yielding stocks.

#2: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all 118 monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

Combining a high dividend yield and a monthly dividend makes Bridgemarq Real Estate Services appealing to income-oriented investors. The company also has a strong business model, with most of its revenues being recurring. In this article, we will discuss the prospects of Bridgemarq Real Estate Services.

Business Overview

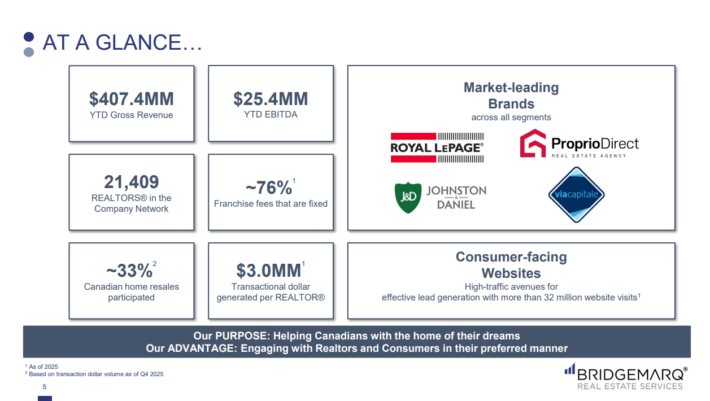

Bridgemarq Real Estate Services provides various services to residential real estate brokers and REALTORS in Canada. It offers information, tools, and services that assist its customers in the delivery of real estate services. The company provides its services under the Royal LePage, Via Capitale, Johnston, and Daniel brand names. The company was formerly known as Brookfield Real Estate Services and changed its name to Bridgemarq Real Estate Services in 2019. Bridgemarq Real Estate Services was founded in 2010 and is headquartered in Toronto, Canada.

Bridgemarq generates cash flow from fixed and variable franchise fees from a national network of more than 21,000 REALTORS operating under the aforementioned brand names. Approximately 81% of the franchise fees are fixed in nature, resulting in fairly predictable and reliable cash flows. Franchise fee revenues are protected via long-term contracts.

Bridgemarq has a solid business relationship with its partners, and thus, it enjoys remarkably high renewal rates. The company has historically achieved a 96% renewal rate whenever a contract has expired.

Source: Investor Presentation

Moreover, Royal LePage’s franchise agreements, which comprise 96% of the company’s REALTORS, are 10-to 20-year contracts, providing great cash flow visibility.

Bridgemarq has a dominant business position in Canada. Through its immense network of REALTORS, the company participated in over 70% of the total home resales in Canada. Bridgemarq’s brands attract franchisees thanks to their reputation and the technological advantages they provide.

Despite its strong business model, Bridgemarq was severely hurt by the fierce recession caused by the coronavirus crisis in 2020. The Canadian real estate market faced an unprecedented downturn that year. Consequently, the company saw its earnings per share plunge 47%, from $0.34 in 2019 to $0.18 in 2020.

On March 13th, 2026, Bridgemarq Real Estate Services reported fourth-quarter and full-year results for the period ending December 31st, 2025. Revenue for the quarter fell 2.9% to $69.6 million, due to a 16% year-over-year contraction in the Canadian residential market and lower transaction volumes in Toronto and Vancouver.

Bridgemarq recorded a quarterly net income of $0.38 per share, a significant turnaround from the loss of $0.68 a year earlier, primarily driven by a non-cash gain on the valuation of exchangeable units. Adjusted EPS for the quarter was a loss of $0.05, down from a loss of $0.02 last year, as higher commission and operating expenses and increased income tax costs outweighed the positive impact of strategic fee increases and a 2% growth in the agent network.

For the full year, Bridgemarq generated earnings-per-share of $0.32, supported by a resilient network of 21,409 realtors despite broader industry headwinds. We expect that the company will produce adjusted EPS of $1.00 this year, which we have applied in our estimates.

Growth Prospects

Bridgemarq pursues growth by continuously increasing the number of its partners.

Source: Investor Presentation

The company has grown the number of REALTORS by more than 6% since 2020. As a result, it now has 21,409 partners operating through 286 franchise agreements at 727 locations.

As mentioned, the vast majority of Bridgemarq’s franchise fees are fixed, which renders the company’s cash flows fairly predictable. However, this is easier said than done.

Bridgemarq has exhibited a somewhat volatile performance record over the last nine years due to the volatility in the real estate market and the swings of the exchange rate between the Canadian dollar and the USD.

Given Bridgemarq’s strong business position, long-term performance record, and some growth limitations due to the company’s size, we expect approximately 0.0% average annual earnings per share growth over the next five years.

Dividend & Valuation Analysis

Bridgemarq is offering an exceptionally high dividend yield of 9.9%, more than eight times the 1.2% yield of the S&P 500. The stock is thus an interesting candidate for income-oriented investors, but U.S. investors should be aware that the dividend they receive is affected by the prevailing exchange rate between the Canadian dollar and the U.S. dollar.

Bridgemarq has routinely had payout ratio of over 100%, with last year’s payout ratio equating to 306%. The projected payout ratio for 2026 is 98%. The company’s balance sheet does not look very good. The company’s net debt is $67 million which compares to the stock’s market capitalization of $94 million. Overall, the company’s dividend is could face reduction or elimination in the face of a severe recession.

On the other hand, investors should be aware that the dividend has remained essentially flat over the last decade. Thus, it is prudent not to expect meaningful dividend growth going forward.

Shares of Bridgemarq are currently trading at 9.9 times our expected earnings-per-share of $1.00 for 2026. We have assumed a fair price-to-earnings ratio of 10.0 for the stock. Reverting to our target valuation by 2031 would add 0.1% to annual returns over this period.

Considering the 0.0% annual growth of earnings per share, the 9.9% dividend yield, and a small tailwind from multiple expansion, Bridgemarq could offer a 8.5% average annual total return over the next five years.

Final Thoughts

Bridgemarq has a dominant position in its business and enjoys fairly reliable cash flows thanks to the recurring nature of most of its fees. It also offers an exceptionally high dividend yield of nearly 10% which makes it attractive for income-oriented investors. The payout ratio is high, which could indicate a potential dividend cut if the business fails to produce strong results.

Given total return potential and the possibility of a dividend cut in a downturn, we place a hold rating on shares of Bridgemarq Real Estate Services.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more