Published on April 16th, 2026 by Nathan Parsh

Investing in real estate investment trusts, or REITs, can be a fruitful option for investors seeking high-income yields. This is due to their obligation to distribute the majority of their profits to shareholders in the form of dividends. Many income-focused investors, particularly retirees, find REITs appealing but usually focus on the U.S.-based ones.

Exploring opportunities beyond the U.S. market may be wise, as reliable dividend-paying REITs exist in other countries. Canada, in particular, features several REITs that boast decades of consistent shareholder value creation. Canadian Apartment Properties Real Estate Investment Trust (CDPYF) is one such company.

Canadian Apartment Properties REIT stands out among other REITs because it offers monthly dividend payments, whereas most REITs provide dividends quarterly.

While a few other REITs also offer monthly dividends, this distinguishing feature sets Canadian Apartment Properties REIT apart from the pack. This is especially true in this case, as the company has paid a monthly dividend consistently since 1998 and has never cut it despite the hardships that have arisen since.

There are currently just 118 monthly dividend stocks.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

Canadian Apartment Properties REIT offers a dividend yield of 4.2% at current prices, which is notably higher than the broad market’s dividend yield, which stands at about 1.2% right now.

The above-average dividend yield and Canadian Apartment Properties monthly dividend payments make the REIT worthy of research for income investors. This article will discuss the investment prospects of Canadian Apartment Properties (in short, CAPREIT) in detail.

Business Overview

CAPREIT is Canada’s largest real estate investment trust. The company owns approximately 45,905suites, including townhomes and manufactured housing sites, in Canada.

Further, the company, directly and indirectly, owns a 66% equity stake in European Residential Real Estate Investment Trust, another publicly traded Canadian REIT. The company also owns approximately suites in the Netherlands through this investment. It was announced on March 2nd, 2026, that CAPREIT would purchase all the units of European Residential Real Estate Investment Trust that it didn’t already own.

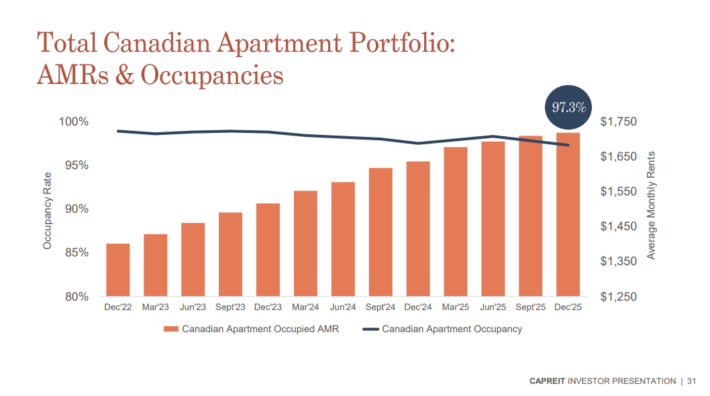

Source: Investor Presentation

The company’s Canadian portfolio enjoys exceptionally high occupancy, ending the fourth-quarter of 2025 with a 97.3%

occupancy rate. CAPREIT remaining suites are in the Netherlands. These were 90.6% occupied to close out the year.

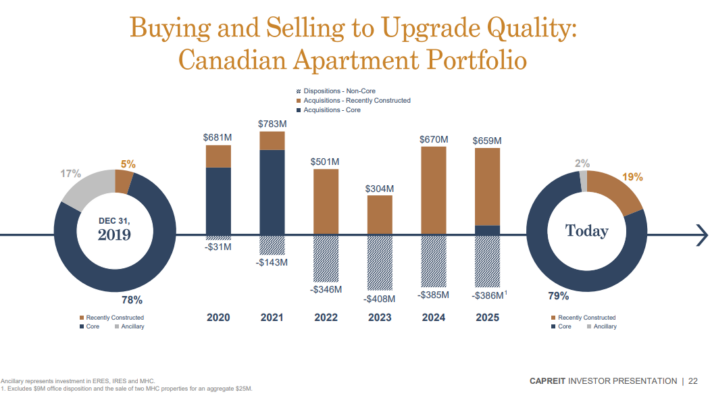

In 2025, the company strategically disposed of $1.2 billion CAD of properties in Canada and the Netherlands. These deals were completed at prices at or above previously reported IFRS fair values at the time of negotiation. The proceeds from these dispositions are being used to acquire recently constructed mid-market rental properties at prices that are meaningfully below replacement cost, as well as unit repurchases.

On February 12th, CAPREIT reported results for the fourth-quarter and full year for the period ending December 31st, 2025. The company’s operating revenue in CAD currency fell 12.0% year-over-year to $243.3 million during the quarter. That was linked to dispositions, which were mostly completed in the first half of 2025.

Adjusting for foreign currency translation, CAPREIT’s operating revenue was lower by 13.6% over the year-ago period to $176.3 million in the quarter (based on average CAD to USD exchange rates in Q4 2024 and Q4 2025). The company’s diluted FFO per unit improved 1.6% for the quarter to $0.632 CAD. Factoring in foreign currency translation, CAPREIT’s FFO per unit was down by 0.2% to $0.458 during the quarter.

Growth Prospects

Moving forward, we expect CAPREIT to drive growth through accretive acquisitions and organic rent growth, as it has done in the past.

Management believes that acquiring newly built properties should be a favorable strategy these days, as such properties should reduce the company’s future capital investment needs and, therefore, its exposure to inflationary pressures.

Source: Investor Presentation

Like all REITs, CAPREIT taps into both debt and equity markets to finance its future growth. As interest rates are now higher, one valid concern investors could have is the potential challenges to the company’s expansion efforts due to financing becoming notably more expensive lately. Despite this, CAPREIT has established an impressive credit profile over the years, which allows it to access financing at highly competitive rates.

CAPREIT’s improved its financial position in 2024, reducing total debt to gross book value to 38.4% (down from 41.6% in 2023). This was driven by $2.5 billion in non-core asset sales, which helped lower leverage and focus on high-quality properties. The company maintained a strong liquidity position of $688.2 million, including $565.3 million in available borrowing capacity.

The trust finished 2025 with a total debt to gross book value of 39.3%, up slightly from the prior year.

The company’s balance sheet remains solid, with a weighted average mortgage interest rate of 3.3% and a focus on maintaining a sustainable debt structure while growing its high-performing assets.

Dividend & Valuation Analysis

CAPREIT boasts an impressive track record of paying monthly dividends for more than 25 consecutive years. Most importantly, the company never had to cut its dividend, even during challenging times like the Great Financial Crisis and the COVID-19 pandemic, when most REITs struggled significantly. It should be noted that the dividend was frozen in 2023.

Except for the years between 2004 and 2011, when the dividend remained stable at C$1.08 annually, CAPREIT has consistently increased its dividend every other year during its history.

Although the current annual rate of $1.13 for U.S. investors yields just over 4.0%, which is below average for the sector and somewhat underwhelming given today’s interest rates, we remain highly confident in CAPREIT’s dividend safety. Not only has the company proven its resilience in harsh economic conditions, but with a comfortable FFO payout ratio of 59% for 2026, there is ample room for future hikes and no concerns about potential cuts.

Furthermore, total returns will also be aided by FFO growth and possible multiple expansion. We project FFO-per-share growth of 3.5% per year through 2031.

Shares of CAPREIT trade at 14.2 expected FFO-per-share for the year, which is below our target multiple of 18.5 times FFO. Reaching our target multiple by 2031 would add 5.4% to annual returns over this period.

In total, we project that CAPREIT could provide annual returns of 12.2% per year over the next five years. This stems from our FFO growth rate target of 3.5%, the 4.2% starting yield, and a mid-single-digit tailwind from multiple expansion.

Final Thoughts

CAPREIT is one of Canada’s most reputable REITs, with a proven track record of growing its financials and dividends.

Overall, while CAPREIT’s yield is among the largest in the REIT sector, the stock is likely to continue satisfactorily serving income-oriented investors who seek a predictable payout. After all, the company’s number one objective is long-term, stable, and predictable monthly cash dividends.

We project double-digit returns annually through 2031, but maintain our hold rating on the stock due to a lack of dividend growth in U.S. dollars.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more