Updated on April 24th, 2026 by Josh Arnold

Extendicare (EXETF), a Canadian provider of long-term care, home health care, and managed services, is a rare stock in that it pays its shareholders monthly dividends, rather than the standard quarterly schedule. We’ve compiled a list of monthly dividend stocks, 119 in all as of April 2026.

You can download our full Excel spreadsheet of all 76 monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

While the yield is modest at less than 2%, the monthly dividend makes Extendicare appealing to income-oriented investors. The company is also ideally positioned to benefit from the secular growth of demand for healthcare services. In this article, we will discuss Extendicare’s prospects.

Business Overview

Through its subsidiaries, Extendicare provides care and services for seniors in Canada. The company offers long-term care (LTC) services; home health care services, such as nursing care, occupational, physical, and speech therapy, assistance with daily activities, and contract and consulting services to third parties. It operates LTC homes, retirement communities, and home healthcare operations under the Extendicare, ParaMed, Extendicare Assist, and SGP Partner Network brands. The company was incorporated in 1968 and is based in Markham, Canada.

Extendicare operates or provides contract services to a network of just over 100 long-term care homes and retirement communities, providing approximately 11 million hours of home health care services annually.

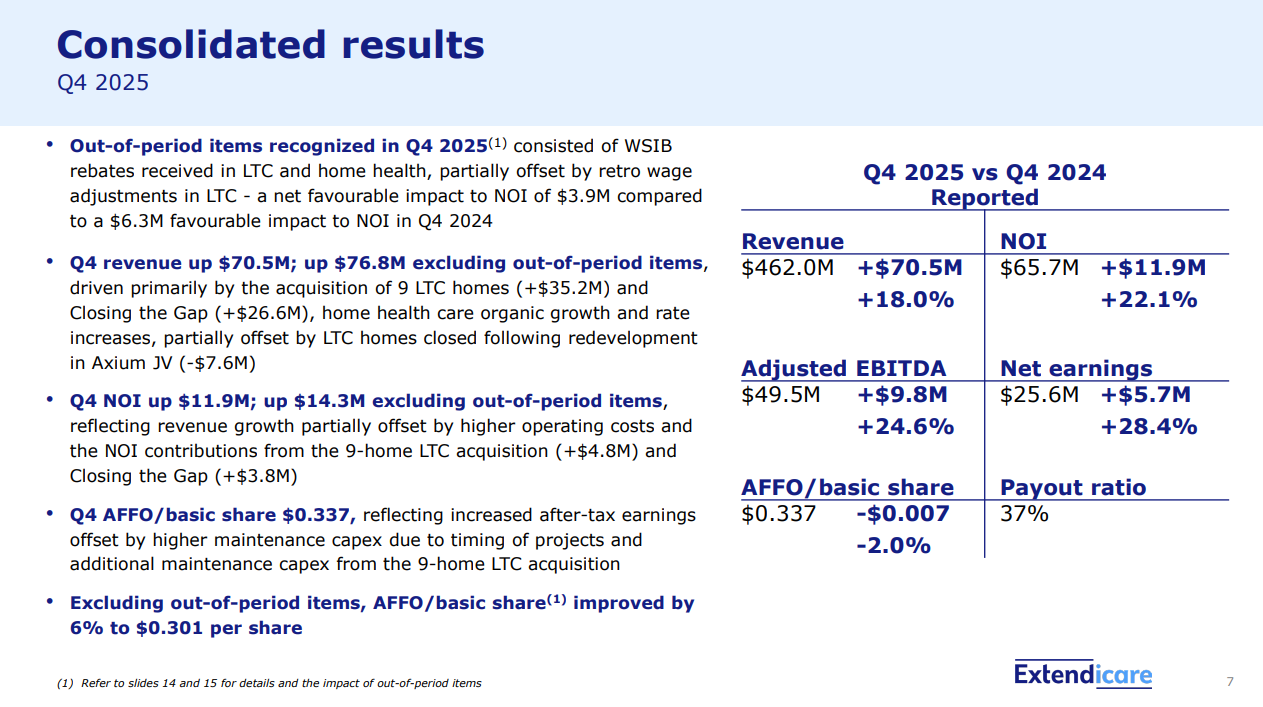

Source: Investor Presentation

Extendicare was been hurt by the coronavirus crisis, which caused many problems in the company’s daily operations. COVID-19, influenza, and other viruses resulted in abnormally high employee absenteeism, thus exacerbating an already tight labor market. As a result, Extendicare has seen its operating costs increase significantly since the onset of the coronavirus crisis.

Still, the company has managed to continue to increase earnings. On February 26th, 2026, Extendicare posted fourth quarter and full-year earnings, which were quite good and capped a very strong year. Revenue was up 18% year-over-year to $337 million, with organic growth driving a very impressive 15.7% gain. The balance of growth was due to the net of acquisitions and divestitures. Higher bill rates helped drive organic revenue growth, partially offset by closure of underperforming homes.

Operating costs were $289 million, reflecting higher labor costs from a variety of factors. Net operating income was up 22% year-over-year to $48 million, with adjusted EBITDA growing to $36 million, or 10.7% of revenue. Net earnings came to 21 cents per share in Q4, up from 17 cents in the year-ago period. For the year, earnings came to 81 cents, up from 60 cents in 2024. We expect $1.06 in earnings-per-share for this year.

Growth Prospects

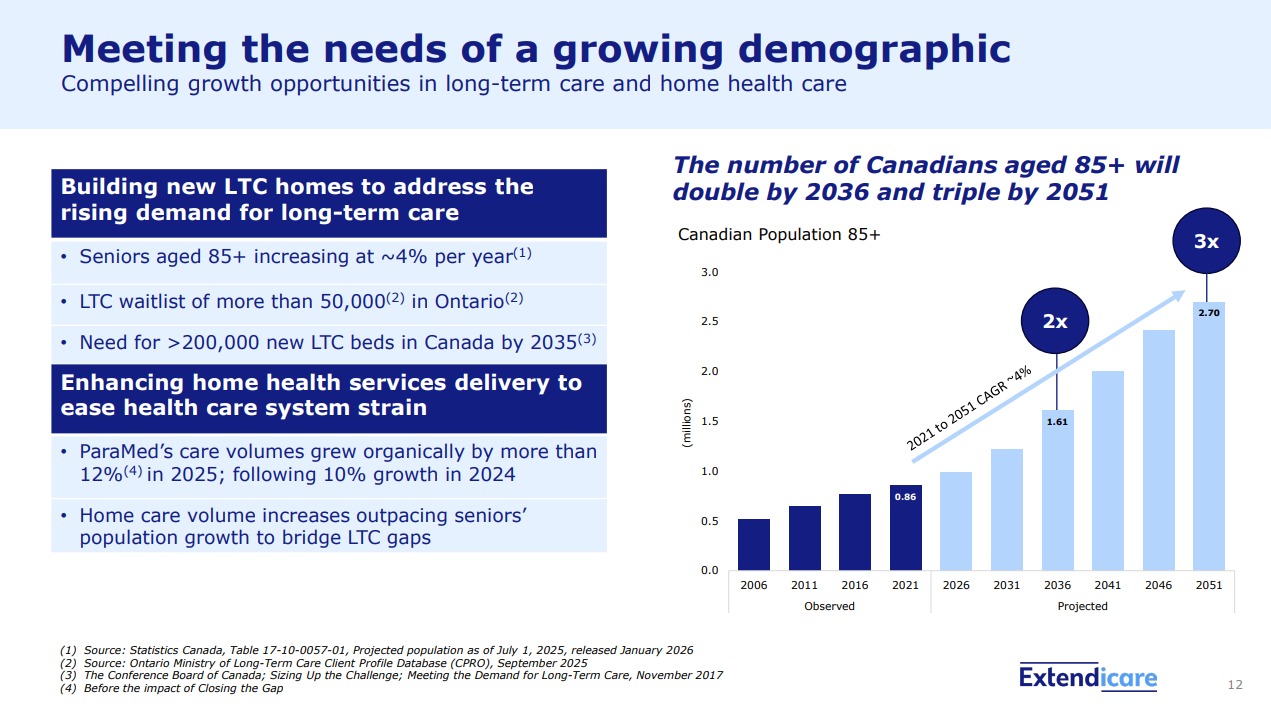

Extendicare is ideally positioned to benefit from a strong secular trend, namely the growing demand for healthcare services. The demand for health care from seniors who are above 85 years old is growing at a rapid rate. Indeed, Extendicare sees that population doubling by 2036, and tripling by 2051.

Source: Investor Presentation

Moreover, there is an immense backlog of demand for long-term care beds, with more than 50,000 seniors waiting for a bed in Ontario alone. According to official estimates, there will be a need for more than 200,000 new long-term care beds in Canada by 2035. Thanks to its 55+ years of experience in this business, Extendicare is ideally poised to benefit from the secular growth in the demand for health care services.

On the other hand, investors should be aware that Extendicare has exhibited a volatile performance record. Due to the aforementioned impact of the pandemic on its business, the company has not grown its earnings per share over the last decade. Therefore, the stock is suitable only for patient investors, who can endure extended periods of poor business performance and stock price volatility and remain focused in the long run. Given the very high comparison base formed this year – which would easily be a record if achieved – we currently expect no growth in earnings in the coming years.

Dividend & Valuation Analysis

Extendicare currently offers a 1.9% dividend yield. It is thus an interesting candidate for income-oriented investors, but the latter should be aware that the dividend may fluctuate significantly over time due to the fluctuation of the exchange rates between the Canadian dollar and the USD.

The company has a very low payout ratio of 35%. The dividend therefore looks very safe, and we don’t see a scenario where the payout should need to be cut anytime soon.

Regarding the valuation, Extendicare is trading for just over 13 times its earnings per share for 2026. We assume a fair price-to-earnings ratio of 10.0 for the stock. Therefore, the current earnings multiple is higher than our assumed fair price-to-earnings ratio. If the stock trades at its fair valuation level in five years, it will have a ~3% annualized compression for the next five years.

Taking into account the 0% projected growth of earnings per share, the 1.9% dividend, and a -3% annualized compression of valuation level, Extendicare could offer very modest annual total returns over the next five years. The stock has doubled in the past six months, causing significant deterioration in the dividend yield and making the valuation much more expensive. Despite the fundamental tailwinds the company is likely to enjoy, the stock offers very unattractive forward returns as it stands today.

Final Thoughts

Extendicare has a solid business model and greatly benefits from the growing demand for healthcare services. The stock offers a modest dividend yield of 1.9% with a healthy payout ratio of 35%, making it a relatively safe candidate for income-oriented investors’ portfolios. The stock has an expected return of close to zero per year over the next five years, however, on a low yield and elevated valuation.

Investors should be aware of the risk resulting from the company’s somewhat weak balance sheet and its choppy business performance. Therefore, the stock is suitable only for patient investors, who can ignore stock price volatility and remain focused in the long run.

Moreover, Extendicare is characterized by exceptionally low trading volume. This means that it is hard to establish or sell a large position in this stock.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more