Published on April 22nd, 2026 by Nathan Parsh

Freehold Royalties (FRHLF) has two appealing investment characteristics:

#1: It is a high-yield stock based on its 6.2% dividend yield.

Related: List of 5%+ yielding stocks.

#2: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all 119 monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

Combining a high dividend yield and a monthly dividend renders Freehold Royalties appealing to income-oriented investors. In addition, the company is ideally positioned to benefit from high production growth in exceptionally rich resource areas in North America. In this article, we will discuss the prospects of Freehold Royalties.

Business Overview

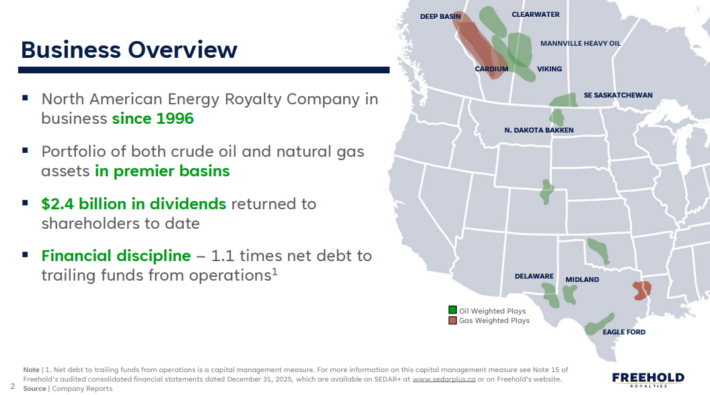

Freehold Royalties is focused on acquiring and managing royalty interest in crude oil, natural gas, natural gas liquids, and potash properties in Western Canada and the United States. The company was founded in 1996 and is headquartered in Calgary, Canada.

Freehold Royalties aims to deliver growth and attractive risk-adjusted returns to its shareholders by acquiring high-quality assets with acceptable risk profiles and long economic lives. It then tries to generate highly profitable lease-out programs for the development of its properties.

Freehold Royalties generates approximately 90% of its revenues from oil and natural gas liquids and the remaining 10% from natural gas.

Source: Investor Presentation

Moreover, the company generates 53% of its revenue and 45% of production from its properties in U.S. and the remaining revenue and production from its properties in the Canada.

As an oil and gas royalty company, it is only natural that Freehold Royalties has exhibited a highly volatile performance record. The royalties that its new customers are willing to pay are greatly affected by the prevailing oil and gas market conditions and the underlying prices of oil and gas.

In addition, the oil and gas production of its existing customers significantly varies from year to year, as it is dependent on the prevailing oil and gas prices. Thus, it is not surprising that Freehold Royalties has posted losses in three of the last ten years.

Freehold Royalties Ltd. reported disappointing fourth-quarter 2025 results on March 11th, 2026. The company’s revenues fell more than 9% to C$70 million versus the fourth-quarter of 2024. This was a particularly disappointing result as the company spent significantly on M&A over the past couple years and taken on a large amount of debt without moving the needle operationally.

Q4 earnings-per-share of $0.09 cents declined significantly from $0.33 last year, triggered by a decrease in revenues and unfavorable foreign exchange. The company made a sizable acquisition of Midland basin royalties in late 2024 that was supposed to help drive earnings growth last year, but falling oil prices fully offset that growth in 2025. The price of oil has surged to start this year, which we believe could lead to a much more favorable view of the company’s earnings potential in light of recent geopolitical developments.

We expect earnings-per-share of $0.75 for 2026, which would be nearly double last year’s result. However, we remain unimpressed with the company’s recent capital allocation strategy and the heightened EPS outlook is entirely based on higher oil and gas price.

Growth Prospects

Freehold Royalties currently enjoys decent business momentum. The company has grown its production by 45% over the last five years to a new record level.

Such a high production growth rate is extremely rare in the oil and gas industry. To provide a perspective, most oil majors, such as Shell (SHEL) and BP (BP), have failed to grow their output over the last several years. This is a key difference between Freehold Royalties and most oil and gas producers.

On the other hand, Freehold Royalties is inevitably sensitive to the oil and gas industry cycles. This is clearly reflected in the company’s volatile performance record. During the last decade, Freehold Royalties has failed to grow its earnings per share on a regular basis. In addition, the company has posted losses in two of the last ten years and negligible profits in several other years.

Freehold Royalties currently enjoys decent business momentum, not only thanks to its high production growth but also thanks to the deep production cuts implemented by OPEC in an effort of the cartel to support the price of oil in recent years. Production in the Gulf Arab states have also been dramatically reduced as the Strait of Hormuz has been closed. The price of natural gas has remained depressed this year, but oil prices have remained above average due to the ongoing conflict in the Middle East. As a result, Freehold Royalties is likely to post above-average profits this year.

Given the decent business momentum and the cyclical nature of the Freehold Royalties business, we expect approximately 1% earnings-per-share annually over the next five years.

Dividend & Valuation Analysis

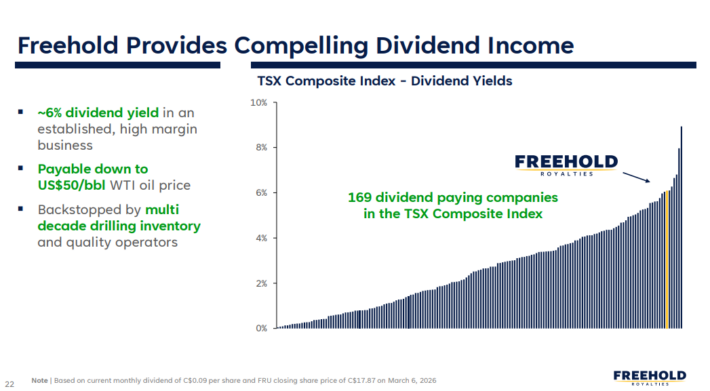

Freehold Royalties is currently offering a high dividend yield of 6.2%, which is five times as much as the 1.2% yield of the S&P 500.

Source: Investor Presentation

The stock is thus an interesting candidate for income-oriented investors, but the latter should be aware that the dividend is not safe due to the cyclical nature of the oil and gas industry.

Freehold Royalties is paying a generous dividend, but its earnings have decreased significantly vs. the 10-year high earnings per share of $1.02 in 2022. As a result, the payout ratio has risen from 68% in 2022 to 188% last year. Such a payout ratio is unsustainable over the long run.

Given its dramatic cycles, management should be praised for its pristine balance sheet, which is paramount in the energy sector. On the other hand, due to the inevitable swings in oil and gas prices, Freehold Royalties’ dividend is far from safe. Notably, the company has cut its dividend several times in the last ten years.

In addition, U.S. investors should be aware that the dividend received from this stock depends on the exchange rate between the Canadian and U.S. dollar.

In reference to the valuation, Freehold Royalties trades at 16.6 times its expected earnings-per-share for 2026. We assume a fair price-to-earnings ratio of 14.0 for the stock. Therefore, the current earnings multiple is higher than our assumed fair price-to-earnings ratio. If the stock were to trade at our target P/E by 2031 then valuation could act as a 3.4% headwind to annual returns over this period.

Taking into account our expectation for 1.0% earnings growth, the 6.2% dividend yield, and a -3.4% annualized valuation headwind, Freehold Royalties could offer just a 3.6% average annual total return over the next five years. This is a low expected total return given the risk profile of the company. With the lack of dividend growth for U.S. investors and a very high expected payout ratio, we rate shares of Freehold Royalties as a sell.

Final Thoughts

Freehold Royalties has much better prospects in growing its production and reserves than most of its peers and offers an above-average dividend yield of 6.2%. The company also has a rock-solid balance sheet, which is likely to entice some income-oriented investors.

However, the company’s performance record has been highly volatile due to its business cycles, and it seems more than fully valued right now and we encourage investors to look elsewhere for income.

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more