Updated on April 30th, 2026 by Josh Arnold

Banks in the US are generally well regarded for income investing. They tend to pay decent yields, and the best-run banks offer relative dividend security and the potential for dividend growth. Internationally, however, banks have proven riskier due to a variety of factors, including geopolitical risk, localized economic weakness, currency risk, and others.

Itaú Unibanco (ITUB) is a Brazilian bank that pays a relatively small dividend to shareholders but one that is quite secure. In addition, it pays its dividend monthly instead of quarterly, allowing for faster wealth compounding and current income.

Itaú Unibanco is one of the stocks we cover that makes monthly dividend payments. You can download our full list of 119 monthly dividend stocks (along with price-to-earnings ratios, dividend yields, and payout ratios) by clicking on the link below:

The payout ratio is modest, which implies good levels of dividend safety, but we see many growth challenges ahead for Itaú Unibanco. With the earnings outlook quite murky and Brazil’s economic growth in doubt, we have concerns about the bank’s near-term future.

Given this, we are cautious on Itaú Unibanco’s prospects as an investment at this time, despite its attractive monthly payout schedule.

Business Overview

Itaú Unibanco is a very large bank that is headquartered in Brazil. ITUB is a large cap stock with a market capitalization above $94 billion.

Itaú Unibanco conducts business in more than a dozen countries worldwide, but its core business is in Brazil. It also has significant operations in other Latin American countries and select businesses in Europe and the US.

Its scale is huge in relation to other Latin American banks. Itaú is the largest financial conglomerate in the Southern Hemisphere, and the largest Latin American bank by assets and market capitalization.

The bank offers its customers an impressive list of services, running the entire spectrum of financial products. This huge list of offerings has helped Itaú Unibanco grow to its current size while diversifying its revenue streams.

Its business has two main segments – Retail Banking and Wholesale Banking. Retail Banking serves smaller consumer accounts, while Wholesale Banking serves larger, mostly business accounts. The retail business produces about two-thirds of the company’s total net income, with the wholesale business making up the balance.

Both are critically important to the bank’s profit outlook, but like many other large banks, Itaú Unibanco’s business is heavily dependent upon consumers.

Given Itaú Unibanco’s reliance upon Brazil and other South American countries for its earnings, we have concerns about its ability to grow reliably.

Growth Prospects

Itaú Unibanco’s strategy of trying to be everything to every consumer and business isn’t unusual in the world of banking. The major US banks have adopted a similar strategy over time, providing core banking services like deposits and loans, but also insurance products, equity investing, and a host of other products to help attract customers.

However, what sets Itaú Unibanco apart is its exposure to emerging economies rather than established ones in Europe or the US. Emerging markets tend to offer stronger growth prospects, but at the expense of risks like geopolitical instability, currency translation, and deeper recessions.

Indeed, Brazil’s economy has struggled for many years, and many of the other countries Itaú Unibanco operates in similar, if not worse, situations.

This is a primary concern for us regarding the company’s ability to grow because a bank’s business model requires broad economic growth for its own expansion. Without this growth, Itaú Unibanco will have a difficult time producing profit expansion.

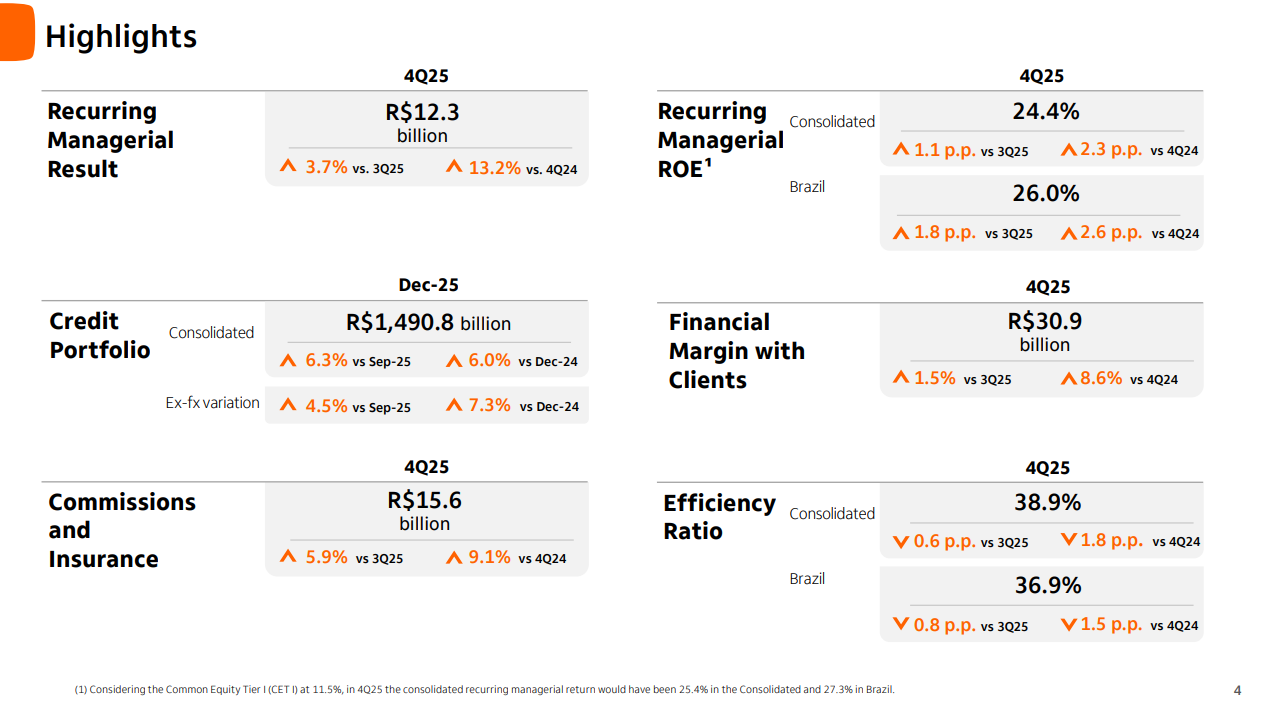

Itau Unibanco posted fourth quarter and full-year results on February 4th, 2026, and results were decent. The bank’s measure of profit – called recurring managerial profit – was $2.4 billion. That was up nearly 4% from the fourth quarter. Recurring ROE was 24.4% on a consolidated basis and 26% in the bank’s home country of Brazil. Total loans reached $291 billion, rising 6.3% for the fourth quarter. Loan growth was strong across consumer and corporate segments, including 8% in credit cards and 3.4% in mortgages.

Source: Investor Presentation

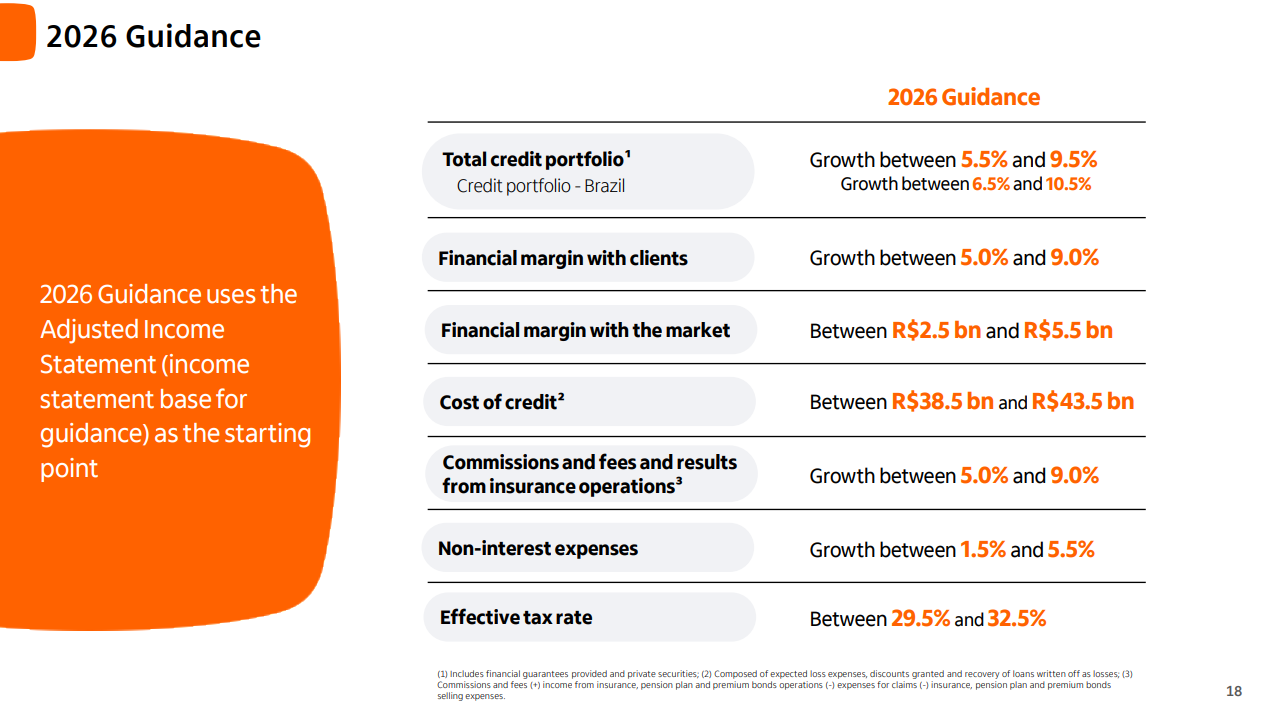

We see 90 cents in adjusted earnings-per-share for 2026, which would represent another strong year of growth should it come to fruition.

Dividend Analysis

Itaú Unibanco takes a conservative approach to dividend payments. The bank pays dividends to shareholders based on its projected earnings and losses, with the goal of being able to continue to pay the dividend under various economic conditions. The bank is on a streak of five consecutive years of dividend increases.

On the plus side, the bank’s yield is strong at about 6.5%, but we are also cautious about future growth given the uncertain outlook for Brazil’s economy.

Source: Investor Presentation

We see the short dividend increase streak and inherent economic risk of the countries the bank serves as cautionary, but the yield is excellent and the payout ratio is quite manageable today. The stock has also performed extremely well in the past year on strong recent earnings growth.

Final Thoughts

We 5% annual earnings growth ahead for Itaú Unibanco. With 5% projected earnings growth under normalized conditions and a nearly-7% dividend yield, we think the stock could be attractive for investors that can handle the risk.

Buying international stocks carries multiple unique risk factors, including geopolitical and currency risks. Itaú stock provides geographic diversification for investors particularly interested in investing outside the United States.

Given all of the above factors, we have a hold rating on Itau Unibanco.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more