Updated on April 30th, 2026 by Nathan Parsh

Mullen Group (MLLGF) has two appealing investment characteristics:

#1: It is offering an above-average dividend yield of 4.2%.

#2: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of 119 monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

The combination of an above-average dividend yield and a monthly dividend makes Mullen Group appealing to income-oriented investors. In addition, the company is one of the largest logistics providers in Canada, with an immense network and strong business momentum. In this article, we will discuss Mullen Group’s prospects.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

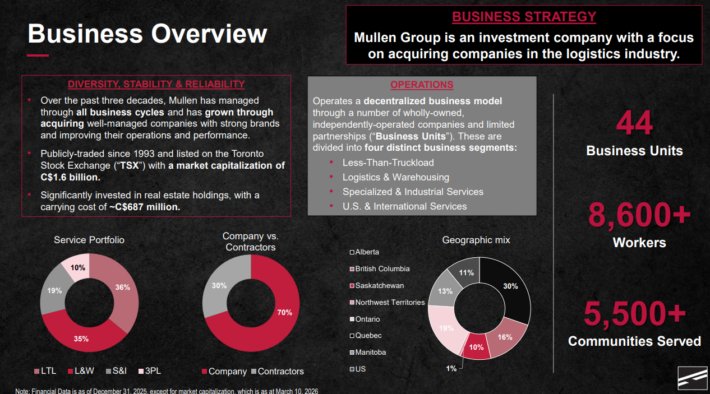

Business Overview

Mullen Group is one of the largest logistics providers in Canada. It started with just one truck in 1949 and has become an immense logistics provider with 40 business units. It is headquartered in Okotoks, Alberta, Canada.

Its network of independently operated businesses provides a wide range of service offerings, including less-than-truckload, truckload, warehousing, logistics, transload, oversized, third-party logistics and specialized hauling transportation. In addition, the company provides diverse specialized services related to the energy, mining, forestry, and construction industries in western Canada, including water management, fluid hauling and environmental reclamation.

Mullen Group operates in four business segments: Less Than Truckload, Logistics & Warehousing, Specialized & Industrial Services, and the U.S. & International Logistics segment.

The Less Than Truckload segment is the largest first and final-mile network in western Canada and Ontario.

Source: Investor Presentation

This segment is tied to consumer needs and offers delivery services with controlled temperatures throughout the delivery. It has 11 business units, more than 168 terminals, and more than 5400 points of service. This segment performs more than 3 million deliveries every year.

The Logistics and Warehousing segment has 11 business units and is focused on North America.

Source: Investor Presentation

This segment has approximately 20,000 subcontract trucks and operates under an integrated technology platform.

As a logistics company, Mullen Group is sensitive to the underlying economic conditions and, hence, vulnerable to recessions. The company incurred a 22% decrease in its earnings-per-share in 2020 due to the fierce recession and the supply chain disruptions caused by the coronavirus crisis.

However, thanks to the massive distribution of vaccines worldwide, the pandemic has ended, and the economy has recovered. As a result, Mullen Group has fully recovered from the pandemic. It exceeded its pre-pandemic profits in 2021 and posted 9-year high earnings-per-share of $1.20 in 2022.

On April 23rd, 2026, Mullen Group reported its first quarter results on April 23rd, 2026. Revenue grew 10.2% to a record $399.8 million. EPS rose to $0.16 from $0.15 last year, due to a change in margin expansion, AI-led efficiency gains, and disciplined cost controls amid weak growth and fuel price volatility.

Growth was driven by recent acquisitions, most notably the Cole Group, and strong growth rates in the Logistics & Warehousing and U.S. & International Logistics segments. These gains were partially offset by weakness in Specialized & Industrial Services following the completion of non-recurring 2025 projects, as well as lower LTL revenue resulting from severe winter weather and the strategic “demarketing” of specific customers.

Mullen is projected to earn $0.93 per share in 2026, which would be a 25.7% improvement from the prior year.

Growth Prospects

Mullen Group tries to grow its earnings in many ways. It seeks opportunities to expand its network, optimize its existing operations, and minimize costs to enhance its operating margins. Overall, management has preferred enhancing operating margins instead of gaining market share at all costs.

On the other hand, the company has struggled at time to grow its earnings-per-share over the last decade. Currency exchange has played a part in this as the company is at the mercy of the value of the Canadian dollar vs the U.S. dollar.

Overall, though, the company has experienced solid growth. In U.S. dollars, earnings-per-share have a compound annual growth rate of 7.4% over the last 10 years and 9.5% over the last five years.

We forecast that the company can grow EPS at 3% annually through 2031. .

Dividend & Valuation Analysis

Mullen Group is currently offering an above-average dividend yield of 4.2%, nearly four times the 1.1% yield of the S&P 500. The stock is thus an interesting candidate for income-oriented investors, but U.S. investors should be aware that the dividend they receive is affected by the prevailing exchange rate between the Canadian dollar and the USD.

Mullen Group’s expected payout ratio for 2026 is 67%, which is healthy. In addition, the company has a strong balance sheet, with net debt of ~$660 million, which is about 50% of the stock’s market capitalization. As a result, the company is not likely to cut its dividend significantly anytime soon.

On the other hand, it is important to note that Mullen Group has significantly reduced its dividend over the last decade. To be sure, the company has offered a dividend of $0.61 in 2025, which is 48% lower than the dividend of $1.17 that the company offered in 2013.

The significant dividend reduction has resulted from the depreciation of the Canadian dollar vs. the USD and a decline in the company’s earnings-per-share amid volatile business performance. To cut a long story short, Mullen Group is offering a solid dividend yield, but it is prudent for U.S. investors to expect minimum dividend growth going forward.

In reference to valuation, Mullen Group is trading at 16x times its expected earnings-per-share for the year. Given the company’s strong business model and its volatile performance record, we assume a fair price-to-earnings ratio of 12.0x for the stock. Therefore, the current earnings multiple is higher than our assumed fair price-to-earnings ratio. If the stock trades at its fair valuation level in five years, then multiple contraction would reduce annual returns by 5.6% over this period of time.

Considering earnings-per-share growth of 3.0%, the starting dividend yield of 4.2%, and a mid-single-digit headwind from multiple contraction, total annual returns could be just 1.8%through 2031.

Final Thoughts

Mullen Group has a dominant position in its business thanks to its immense network. However, the company has exhibited a volatile performance record and has struggled at times to grow its earnings-per-share over the last 10 years. Therefore, investors should make sure to establish a wide margin of safety before investing in this stock.

Mullen Group is offering a dividend yield of more than 4%. The company has a solid payout ratio of 67% and a strong balance sheet. As a result, its dividend should be considered safe, though investors should not expect meaningful dividend growth anytime soon. Overall, the stock seems more than fully valued right now, and hence investors should wait for a more attractive entry point in order to enhance their future returns. Shares earn a hold rating as a result

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more