Updated on May 6th, 2026 by Josh Arnold

Energy stocks often offer highly attractive income yields since they do not spend much on growth. Instead, many energy stocks keep their production more or less stable while returning a large portion of their cash flows to their investors.

This is why many retirees and other income investors like to invest in energy stocks and their above-average dividend yields. Most energy stocks pay quarterly dividends, but there are outliers.

Peyto Exploration & Development Corp. (PEYUF) is an outlier, making monthly dividend payments.

There are currently just 119 monthly dividend stocks.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

Peyto Exploration & Development (PEYUF) offers a dividend yield of 5.1% at current prices. This is a decently high yield, which, combined with the monthly dividend payments, provides a vast and very smooth income stream.

These dividend properties make Peyto Exploration & Development attractive to income investors. This article will discuss Peyto Exploration & Development’s investment prospects in detail.

Business Overview

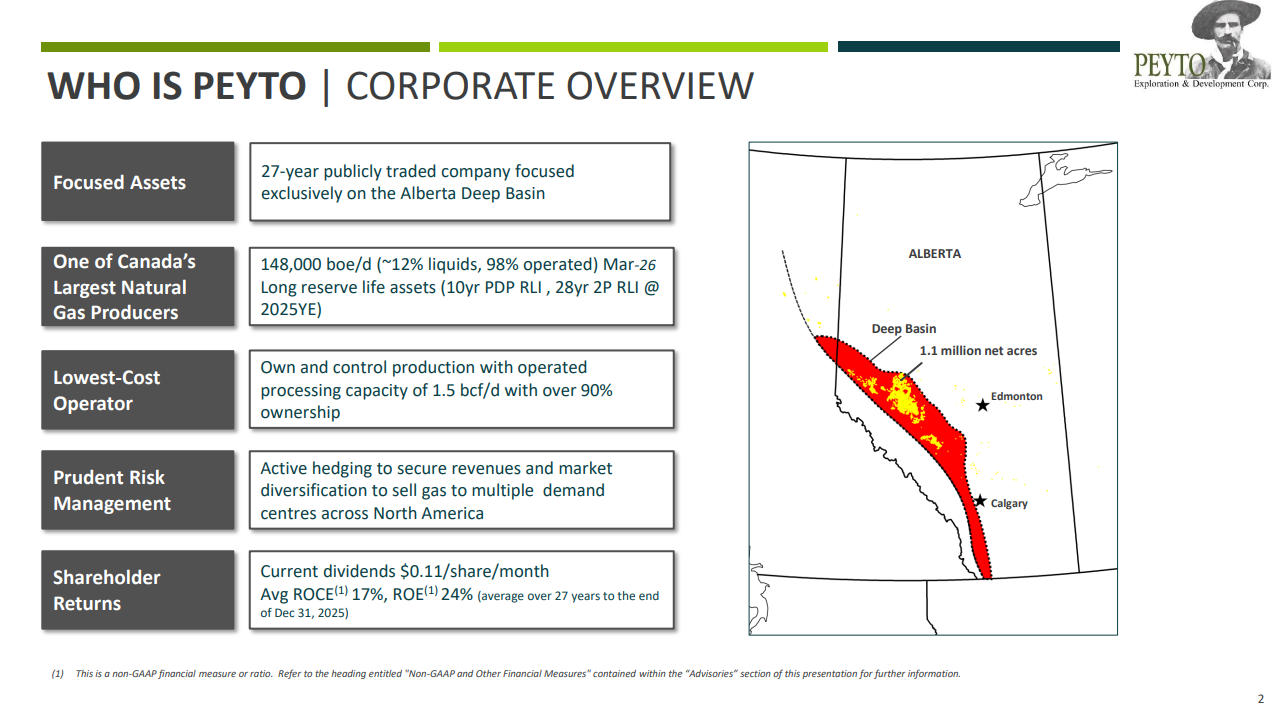

Peyto Exploration & Development, which was once known as Peyto Energy Trust, is a Canadian upstream energy company headquartered in Calgary. Peyto engages in the exploration, development, and production of oil and natural gas.

Today, its market capitalization is US$3.9 billion, meaning it is not among the largest oil companies in Canada or the world. Still, at least in the natural gas space, Peyto is among the top five producers in Canada in terms of production volume.

Source: Investor Presentation

Peyto is focused on the Alberta Deep Basin region, which holds a sizeable asset base with vast proven reserves. These reserves give Peyto a long reserve life, meaning the company could produce from its existing assets for a long period of time. But since Peyto adds to its reserves constantly via new exploration, its reserve life can be expected to remain on the rise.

Importantly, Peyto is the lowest-cost producer in the region in which it is active. As a result, Peyto will generate above-average margins in all market environments, and it might still be profitable in a commodity price environment where many of its peers are no longer profitable.

The low breakeven costs help avoid losses in bad times and make Peyto a less risky investment, relative to higher-cost producers, which will more easily be forced to generate net losses during bad times. With the massive surge in energy prices in recent months, Peyto stands to benefit enormously.

Growth Prospects

While many energy companies do not invest heavily in growth, Peyto has a pretty strong growth track record. This was partly made possible by the fact that Peyto was still a pretty small company in the past, which made it easier to maintain a strong relative growth rate for a longer period of time.

Source: Investor Presentation

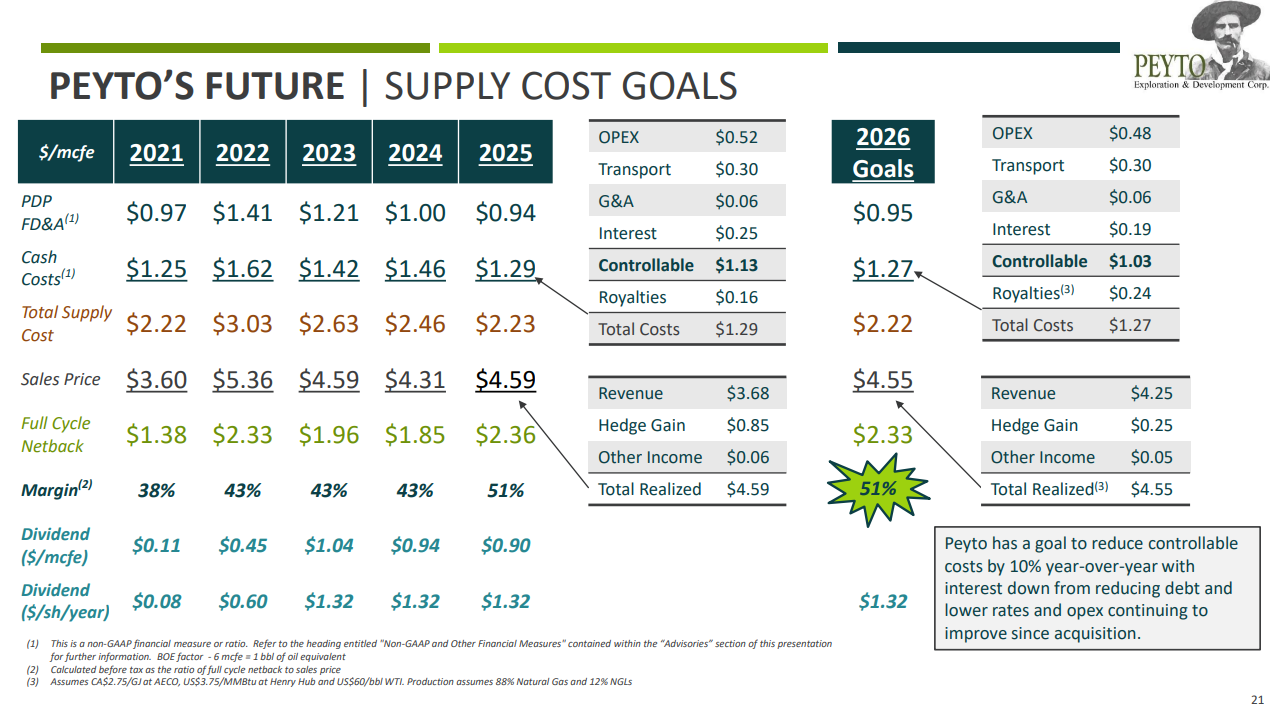

The company posted fourth quarter and full-year earnings on March 10th, 2026, and results were quite strong. Revenue from natural gas sales, including realized hedging gains, was up by a very impressive 14% year-over-year at $255 million. This was driven by record levels of production and a strong hedging program that significantly offset lower spot prices.

Net income was up 61% to $89 million, or 43 cents per share. That was due primarily to a 6% year-over-year increase in production to 140,800 equivalent barrels per day of production and cost efficiencies, which resulted in soaring operating margins of 72%. For 2026, we think the company can reach $3.30 in adjusted earnings-per-share, but that is pending how long energy prices stay elevated near current levels. For now, Peyto’s outlook is easily good enough for what would be a new record.

Dividend Analysis

Like many other energy stocks, Peyto is seen as an income investment by many individual investors. And rightfully so, since the company offers an attractive dividend yield of 5.1%, based on a monthly dividend payout of CAD$0.11 and a current exchange rate of CAD$1.36 per USD, with Peyto trading at US$19 right now.

Based on Peyto’s forecasted 2026 earnings-per-share of US$3.30, the payout ratio is 48%. This is a very manageable payout ratio, provided earnings come in somewhere near current targets. If prices decline precipitously, the dividend could be at risk.

Since Peyto hedges a large portion of its production, it somewhat mitigates the swings in its profits caused by the cycles of oil and gas prices, but it remains sensitive to these cycles.

Final Thoughts

Peyto Exploration & Development Corp. is not very well known, but the company has a highly successful track record. That holds true for production and earnings growth and for returning cash to the company’s owners via dividends.

Peyto trades with a 5.1% dividend yield today, and that dividend is covered based on the forecasted earnings for the current year. Since Peyto makes monthly dividend payments, investors get around 0.5% of their principal per month at current prices, which is intriguing for retirees and other income investors who live off their dividends.

Peyto is currently trading near 6 times this year’s expected net profit, which is a reasonable valuation for an energy stock. It would not be surprising to see Peyto’s valuation expand somewhat over the coming years, which would add to Peyto’s total return outlook.

Thanks to its good dividend yield, business and earnings growth potential, and potential for some expansion of its valuation level, Peyto could deliver highly compelling total returns going forward.

Of course, investors should remember that Peyto is still an E&P company and is thus exposed to commodity price movements.

While its low break-even costs make it more resilient than most peers, Peyto is still greatly affected by oil and natural gas price movements, and hence, it carries a significant amount of risk.

The stock is suitable only for the investors who can stomach the dramatic cycles of the oil and gas prices. And with shares rising very sharply so far in 2026, the risk of buying today is much higher than it was. That includes a much lower dividend yield.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more