Updated on May 6th, 2026 by Josh Arnold

Pine Cliff Energy (PIFYF) has a rather unique, appealing investment characteristic: it pays dividends monthly instead of quarterly. There are only 119 such stocks today, a list of which you can find below.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

However, despite the fact that it pays dividends monthly, the company is facing significant issues, and its dividend yield is very low to reflect its worsening fortunes.

But there’s more to the company than just these factors. Keep reading this article to learn more about Pine Cliff Energy.

Business Overview

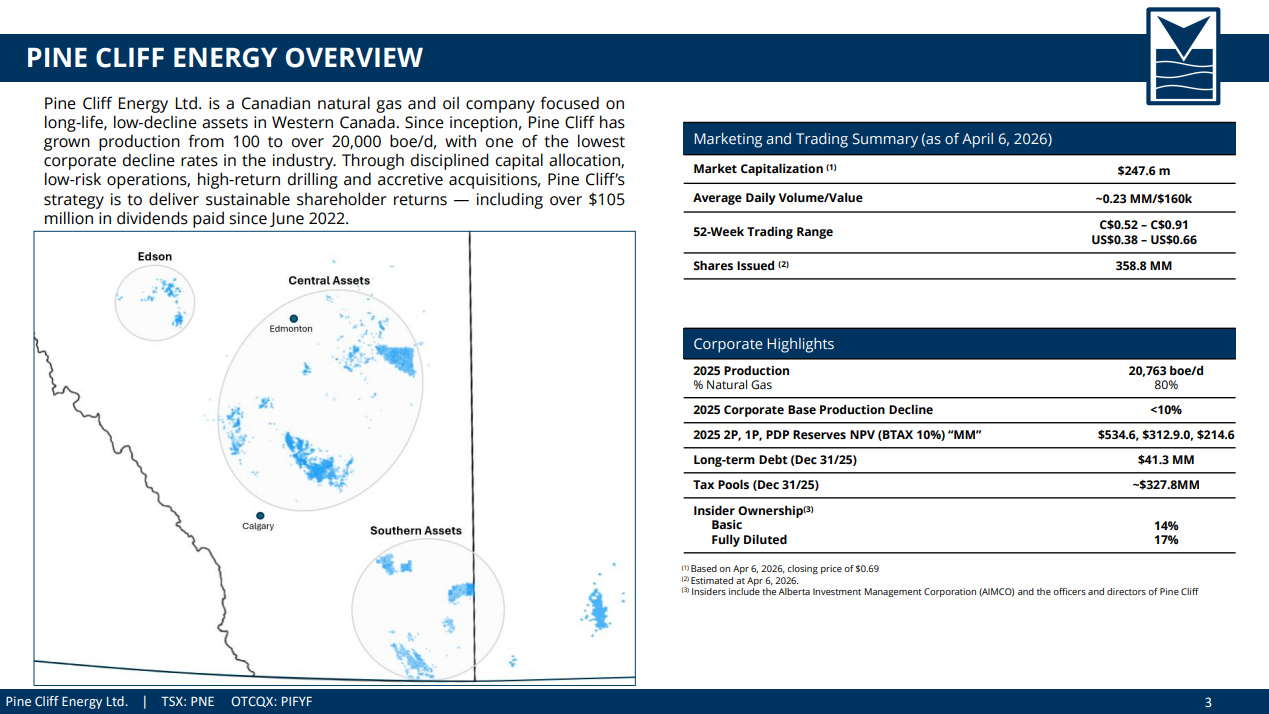

Pine Cliff Energy acquires, explores, develops, and produces oil, natural gas, and natural gas liquids in the Western Canadian Sedimentary Basin.

The company primarily holds interests in oil and gas properties in Southern Alberta, Southern Saskatchewan, and the Edson area, as well as in the Viking and Ghost Pine areas of Central Alberta. It was formed in 2004 and is headquartered in Calgary, Canada.

Pine Cliff Energy produces oil and gas at a ratio of about 20/80, so it should be considered primarily a natural gas producer. As a gas producer, Pine Cliff Energy is highly cyclical due to the dramatic swings in the price of natural gas. Notably, the company has reported losses in seven of the last ten years and initiated a dividend only in 2022.

On the other hand, Pine Cliff Energy claims to have some advantages over well-known oil and gas producers.

First, the company claims to have a decent balance sheet, which is paramount in the oil and gas industry, characterized by frequent downturns every few years.

Source: Investor Presentation

Additionally, Pine Cliff Energy’s management team owns 14% of the company, ensuring alignment with the shareholders. This is an essential characteristic that investors should not undervalue.

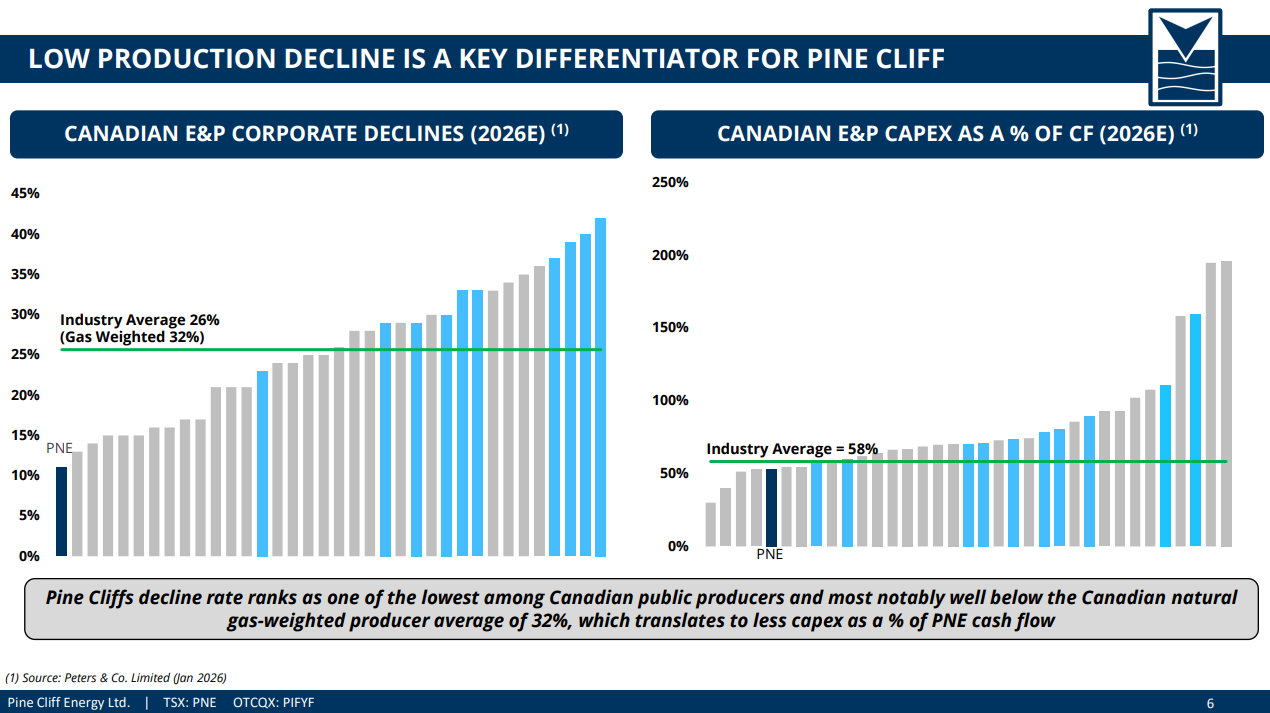

Moreover, Pine Cliff Energy has the lowest natural production decline rate among all Canadian public producers. This reduces the capital expenses required to sustain a given level of production.

Like almost all oil and gas producers, Pine Cliff Energy incurred losses in 2020 due to the collapse of oil and gas prices caused by the coronavirus crisis.

However, global demand for oil and gas recovered in 2021, and thus, the company became profitable in that year.

Even better for Pine Cliff Energy, the Ukrainian crisis triggered a rally in oil and gas prices to 13-year highs in 2022. As a result, the company reported a 10-year high in earnings per share of $0.22 that year. It also initiated a dividend in June 2022, after more than a decade without one.

However, the price of natural gas has declined since early last year due to two consecutive years of abnormally warm winter weather. This has resulted in exceptionally high gas inventories in North America. As a result, earnings have fluctuated around zero in the years since.

The dividend was slashed by 75% in April 2025 as a consequence of these factors.

Pine Cliff posted fourth quarter and full-year earnings on March 4th, 2026, and results showed weakness once again. Total commodity sales were $31.1 million, driven by an 11% decrease in production volumes despite strengthening AECO natural gas prices at the end of the year. Adjusted funds flow was $5.7 million, declining year-over-year on the impact of lower production and a volatile commodity backdrop, which outweighed improvements in realized pricing and ongoing capital discipline. Net income was $2.8 million compared to a loss of $4.1 million in the comparable period a year earlier. This was a reflection of the benefit of significant asset dispositions and higher year-end pricing, which helped offset reduced volumes and higher capex.

We see earnings of just six cents per share for 2026.

Growth Prospects

As mentioned above, Pine Cliff Energy has the lowest natural production decline rate among all Canadian public producers.

Source: Investor Presentation

The natural decline of the producing wells is paramount in the oil and gas industry, as high decline rates result in excessive capital expenses required to sustain a given level of production. Thus, Pine Cliff Energy has a significant competitive advantage over its peers.

On the other hand, as an oil and gas producer, Pine Cliff Energy is highly sensitive to the inevitable cycles of oil and gas prices. More precisely, since the company produces 80% gas and 20% oil, it is particularly sensitive to the fluctuations in natural gas prices.

Thanks to the rally in oil and gas prices to 13-year highs in 2022, Pine Cliff Energy posted a 10-year high earnings per share in 2022. However, both prices have plunged from their highs in 2022. As a result, the company is likely to post much lower earnings per share this year.

Given the highly cyclical nature of the oil and gas industry and our expectations for slightly higher gas prices in the upcoming years, we expect Pine Cliff Energy’s earnings per share to remain steady for the next five years.

Dividend & Valuation Analysis

Pine Cliff Energy is currently offering a decent dividend yield of 2.3%. It is thus not a pure play for income-oriented investors, and those investors should be aware that the dividend is far from secure due to the dramatic fluctuations in oil and gas prices.

Pine Cliff Energy’s forward payout ratio is 15%, which is low, particularly for the energy sector.

Overall, the balance sheet has weakened in recent quarters; therefore, the company will be vulnerable whenever the next downturn in the energy sector occurs.

Moreover, it is critical to note that Pine Cliff Energy initiated a dividend only in 2022, amid multi-year high commodity prices. It failed to offer a dividend in the preceding years, as it incurred material losses in most of those years. Therefore, it is evident that the company’s dividend is far from safe.

Regarding valuation, Pine Cliff Energy is currently trading at 7.8 times its expected earnings per share for this year. Given the company’s high cyclicality, we assume a fair price-to-earnings ratio of 7 for the stock.

Therefore, the current earnings multiple is just ahead of our assumed fair price-to-earnings ratio. If the stock trades at its fair valuation level in five years, it will incur a very modest annualized headwind in its returns.

Taking into account the 0% annual growth of earnings per share, the 2.3% current dividend yield, and a fractional annualized headwind of valuation level, Pine Cliff Energy could offer a slightly negative average annual total return over the next five years.

The stock is highly risky right now, and hence, investors should wait for the next downturn in the energy sector before evaluating it again, particularly in light of the lack of dividend increases.

Final Thoughts

Pine Cliff Energy offers a dividend yield of just 2.3%, which is about double the S&P 500’s ~1% dividend yield. But as a result of weak fundamentals and dividend history, the stock isn’t particularly enticing for income investors.

However, the company has a weakening balance sheet. Additionally, it has proven highly vulnerable to the fluctuations in oil and gas prices.

As these prices appear to have peaked in this cycle, the stock is currently highly risky. Therefore, investors should wait for a much lower entry point.

Moreover, Pine Cliff Energy is characterized by extremely low trading volume. This means that it is hard to establish or sell a large position in this stock. We think investors should avoid the stock given the low yield, unfavorable valuation, and lack of growth catalysts.

Additional Reading

Don’t miss the resources below for more monthly dividend stock investing research.

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 5%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more