Published on April 30th, 2026 by Josh Arnold

Real estate investment trusts, or REITs, can offer highly attractive income yields. They are required to pay the majority of their profits as dividends to their shareholders.

This is why many retirees and other income investors like to invest in REITs, although not all REITs are equally well-liked. It can make sense to look for REITs outside of the US, as there are attractive and reliable dividend payers in other countries as well. This includes RioCan Real Estate Investment Trust (RIOCF), for example, which is a Canadian REIT.

RioCan REIT is a somewhat special REIT because it pays monthly dividends. While some other REITs also pay monthly dividends, most offer quarterly dividend payments to their owners.

There are currently just 119 monthly dividend stocks. You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

RioCan REIT offers a dividend yield of 5.5% at current prices, more than five times the S&P 500’s yield of 1%.

The above-average dividend yield and RioCan’s monthly dividend payments make the REIT worthy of research for income investors. This article will discuss the investment prospects of RioCan REIT in detail.

Business Overview

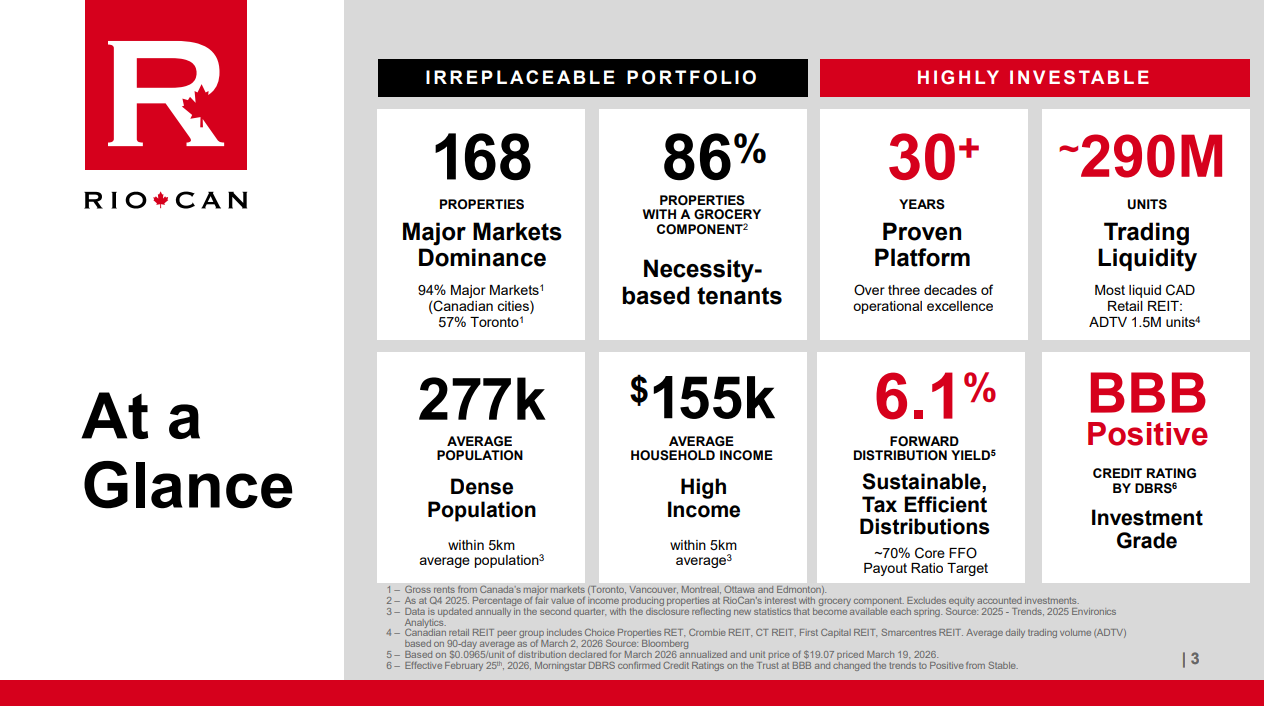

RioCan is a real estate investment trust that was founded in 1993 by Ed Sonshine, making it one of the first REITs in Canada overall. RioCan is headquartered in Toronto, Canada, and is one of the largest REITs in the country. The company currently has a market capitalization of $3.5 billion.

The REIT invests in commercial properties with a retail real estate focus. Still, the company has been diversifying its asset base in recent years, which is why RioCan describes its portfolio as retail-focused and increasingly mixed-use.

Some of the REIT’s headline numbers can be seen here:

Source: Investor Relations

RioCan focuses on large urban markets, where demand for properties is generally higher, and average rents are higher as well. Thanks to urbanization, people are moving into these markets, which is why the longer-term outlook for these properties is positive. More than half of its properties (by square footage) are located in the Greater Toronto Area.

RioCan owns nearly 170 properties, with about 31 million square feet of net leasable area. On top of that, there’s a huge pipeline of high-quality assets that RioCan plans to develop over time amounting to about 17 million square feet, although this will take years.

While retail REITs can be vulnerable to recessions and other macro shocks when they have a focus on (lower-quality) malls where tenants aren’t resilient, RioCan’s focus is different. Many of its tenants are necessity-based, i.e. drug stores, grocers, and so on. These tend to remain resilient during recessions, which is why there is little risk that RioCan’s tenants will default or run into trouble in a big way.

Under its RioCan Living brand, RioCan also offers residential real estate. Like in the commercial portfolio, the focus here is on high-class assets in the largest and fastest-growing markets. While average lease yields in the residential space are lower relative to commercial assets, residential real estate is very resilient; thus, the buildout of this business lessens some of the risk with RioCan.

In addition, rent growth in the residential space is higher than in many other real estate markets; thus, the residential business could allow for an improved organic growth rate in the future.

RioCan posted fourth quarter and full-year earnings on February 17th, 2026, and results were decent. Revenue was up 3.5% year-over-year to $285 million during the quarter. FFO-per-share fell 5.1% year-over-year, while core FFO fell 4.7% for the quarter.

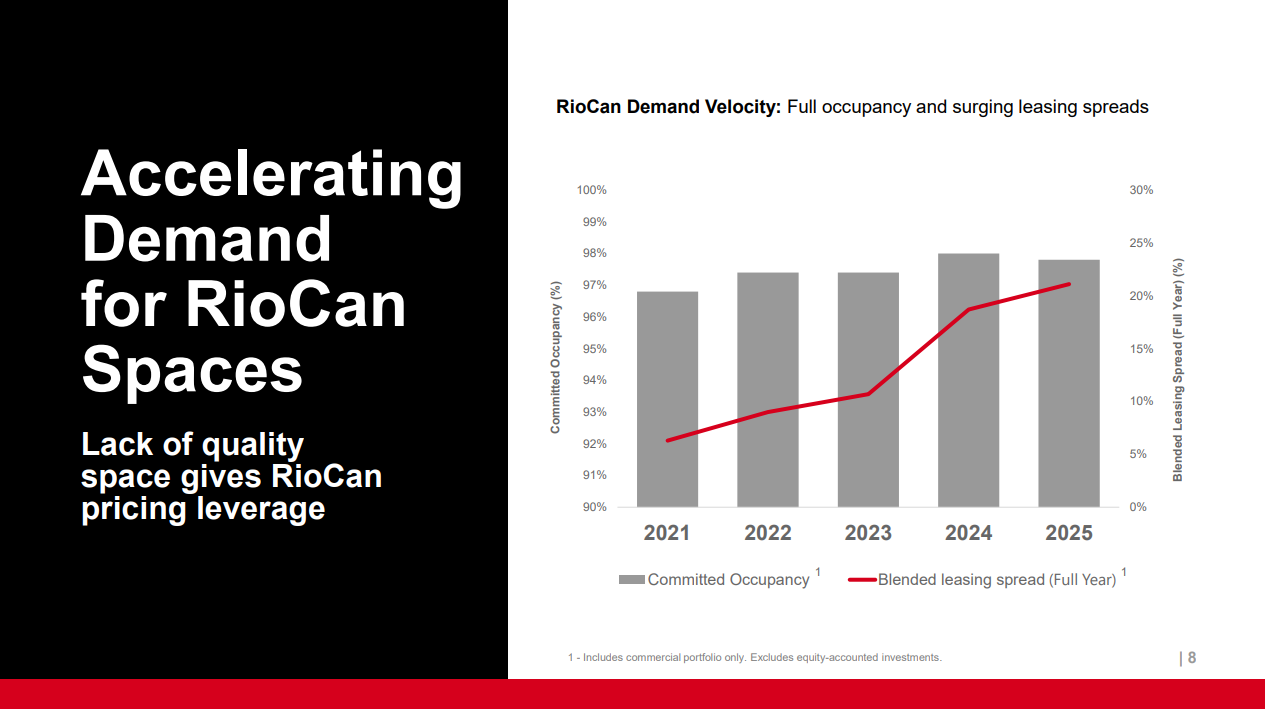

New leasing spreads were 37.3% for the year, while blended leasing spreads were 21.1%. These reflected continued strong supply and demand fundamentals for the trust’s properties. Commercial same-property net operating income grew 4.5% for the fourth quarter, and 3.6% for the year. Total capital repatriation was $742 million, while debt to adjusted EBITDA was down to a still-elevated 8.6X. The trust also repurchased $179 million in its own stock.

We see $1.14 in adjusted FFO-per-share for 2026, largely in line with 2025.

Growth Prospects

RioCan has grown its funds from operations-per-share at a solid pace in the past and targets 5% to 7% annual FFO-per-share growth in the coming years. We are more cautious, however, at 2.5% projected medium-term growth.

This funds from operations growth was made possible by several contributing factors. First, the company can increase its same-property rents over time:

Source: Investor Relations

We note that leasing spreads have been in the 5% to 10% range per year in the recent past before surging in the past two years. While leasing spreads will likely not be as high as the level seen over the past few years going forward, it can be expected that RioCan’s high-quality assets and underlying market growth will allow for ongoing solid lease rate growth at existing properties. Growing rents at existing properties allow for positive same-property net operating income growth, an essential driver for the company’s FFO.

Second, RioCan’s development pipeline and asset purchases should increase the company’s cash flows going forward. RioCan targets a payout ratio of 55% to 65% of its funds from operations via dividends, which means that considerable additional cash is retained. That cash can be used to finance the development of new projects, while using it for acquisitions is another possibility. It should be noted that this is a much lower payout ratio than many of the monthly dividend-paying stocks in our coverage universe. We reiterate that the trust has been buying back shares as well.

RioCan’s healthy balance sheet also allows the REIT to finance some of its future investments via debt. The company’s capital recycling activity of selling non-core assets also generates cash that can be used to pay for the development of new and attractive properties in RioCan’s pipeline.

Dividend Analysis

RioCan REIT is seen primarily as an income investment like many other REITs. And rightfully so, as the company offers an attractive dividend yield of 5.5%, based on a monthly dividend payout of CAD$0.0965. At the current exchange rate to USD, shares of RioCan REIT are trading at USD$15.47.

With FFO of USD$1.14 for 2026 and projected dividends of USD$0.85, the payout ratio is projected to be 74%. This indicates that the dividend is relatively safe, as that is not a high payout ratio for a REIT, as many peers operate with much higher payout ratios.

When FFO keeps growing per share, even in a tough economic environment, there is little reason to worry about the dividend as coverage improves over time, all else equal.

The balance sheet further indicates that there is little reason to worry about a dividend cut. RioCan’s debt to assets stand at only about half, which is relatively conservative for a REIT.

Final Thoughts

RioCan REIT is one of Canada’s largest and oldest REITs that operates with a retail-focused portfolio but that has been expanding in the mixed-use and residential space in recent years. The REIT offers an attractive dividend yield of more than 5%.

The focus on high-quality assets in large and growing markets means that RioCan’s portfolio is likely positioned well for the long run, as rents should continue to climb over time, as they have done in the past.

With its strong high-quality asset base and a well-covered dividend, monthly-paying RioCan REIT has merit as an income investment at current prices.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more