Updated on May 14th, 2026 by Felix Martinez

Timbercreek Financial Corporation (TBCRF) has two appealing investment characteristics:

#1: It is a high-yield stock based on its 10.6% dividend yield.

Related: List of 5%+ yielding stocks.

#2: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

The combination of a high yield and a monthly dividend renders Timbercreek Financial appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Timbercreek Financial.

Business Overview

Timbercreek Financial is a mortgage investment company that provides shorter-duration structured financing solutions to commercial real estate investors in Canada. The company focuses on lending secured by income-producing real estate, such as multi-residential, retail, and office properties in urban markets. Timbercreek Financial was founded in 2016 and is headquartered in Toronto, Canada.

Timbercreek Financial employs a service-oriented business model, offering borrowers faster execution and more flexible terms than Canadian financial institutions. This is one of the reasons why its customers choose Timbercreek Financial over traditional banking channels.

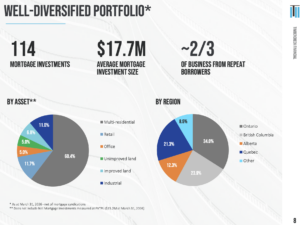

Approximately 86.5% of Timbercreek Financial’s portfolio properties are income-producing.

Source: Investor Presentation

This feature is paramount, as it renders the loans provided by the company much more reliable. Moreover, 97% of the total portfolio is invested in reliable urban markets.

Due to the nature of its business, Timbercreek Financial is sensitive to the underlying economic conditions. Some of its customers cannot borrow funds through traditional banking channels and are therefore often vulnerable during economic downturns.

Indeed, Timbercreek Financial was hurt by the fierce recession caused by the coronavirus crisis. In 2020, the company incurred a 39% decrease in its earnings per share, from $0.51 to $0.31. Fortunately, the recession proved short-lived thanks to the unprecedented fiscal stimulus packages offered by the Canadian government in response to the pandemic. As a result, Timbercreek Financial has fully recovered from this crisis.

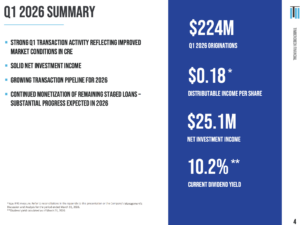

The company reported a solid first quarter of 2026, supported by C$224.2 million in mortgage originations and renewals. This increased the company’s net mortgage portfolio to C$1.24 billion, up 14.9% from the prior year. Management expects continued portfolio growth in 2026, particularly in multi-family residential lending.

Financial results were slightly lower than a year ago. Net investment income declined to C$25.1 million from C$28.6 million, while distributable income totaled C$14.5 million, or C$0.18 per share, compared with C$15.4 million, or C$0.19 per share, in the first quarter of 2025. Net income was C$10.4 million, or C$0.13 per share, primarily due to higher-than-expected credit losses on legacy loans. The company maintained its quarterly dividend of C$0.17 per share, representing a 98.5% payout ratio based on distributable income.

The portfolio remains conservatively positioned, with a weighted-average loan-to-value ratio of 66.5%, 94.7% of investments in first mortgages, and 59.7% allocated to multifamily properties. Management is actively resolving underperforming loans and reinvesting capital into higher-quality mortgage investments, which is expected to improve earnings and support dividend stability through 2026.

Source: Investor Presentation

Growth Prospects

Timbercreek Financial pursues growth by lending funds to new customers at attractive interest rates. It attempts to lend funds secured by income-producing properties to ensure its loans will be serviced without issue.

Unfortunately, this is easier said than done. To be sure, the company has failed to grow its earnings per share over the last seven years. The uninspiring performance has partly resulted from the devaluation of the Canadian dollar vs. the USD. U.S. investors should be aware that fluctuations in the exchange rate between these two currencies significantly affect Timbercreek Financial’s earnings and dividends in U.S. dollars.

Even when the devaluation of the Canadian dollar is taken into account, Timbercreek Financial still has a poor performance record over the last seven years, as it has hardly grown its bottom line. Therefore, it is prudent for investors to be conservative in their growth expectations.

Given the somewhat volatile performance record of Timbercreek Financial and the sensitivity of its earnings to exchange-rate fluctuations, we anticipate earnings per share to be approximately flat over the next five years.

Dividend & Valuation Analysis

Timbercreek Financial is currently offering an exceptionally high dividend yield of 10.6%, more than six times the S&P 500’s yield. The stock is thus an interesting candidate for income-oriented investors, but they should be aware that the dividend is far from safe due to its sensitivity to the aforementioned fluctuations in currency exchange rates.

Moreover, Timbercreek Financial currently has a payout ratio of 100%, which is unsustainable in the long run and does not provide a margin of safety. Furthermore, the company is sensitive to the underlying economic conditions. As a result, whenever it faces a potential recession, it may cut its dividend.

It is also important to note that Timbercreek Financial is sensitive to the yield curve. When the risk of an upcoming recession increases, short-term interest rates exceed long-term interest rates; in that case, Timbercreek Financial’s profit margin on new loans is effectively eliminated. This is precisely what the company is experiencing right now.

In reference to the valuation, Timbercreek Financial is currently trading at 9 times its last 12 months’ earnings per share. Given the company’s volatile performance record, we assume a fair price-to-earnings ratio of 8 for the stock. Therefore, the current earnings multiple is marginally higher than our assumed fair price-to-earnings ratio. If the stock trades at its fair valuation level in five years, it will decrease a marginal 0.5% annualized headwind in its returns.

Considering flat earnings per share over the next five years, the current 10.6% dividend yield, and a 0.5% annualized compression in valuation, Timbercreek Financial could offer an average annual total return of 10.1% over the next five years. This is a decent expected return, but we would require a higher return to recommend buying this volatile stock. Therefore, investors should wait for a significantly lower entry point.

Final Thoughts

Timbercreek Financial offers an exceptionally high dividend yield of 10.6% and pays its dividends monthly, which may entice some income-oriented investors.

However, the company has a payout ratio of 100%, which makes it vulnerable to a potential recession and to a yield curve inversion. Therefore, Timbercreek Financial’s dividend is far from safe.

Moreover, Timbercreek Financial is characterized by extremely low trading volume. This means that it is hard to establish or sell a large position in this stock.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more