Updated on March 4th, 2023 by Nikolaos Sismanis

Monthly dividend stocks are highly appealing to individuals such as retirees because they make it significantly easier to budget dividend income against living expenses. We’ve compiled a list of all 84 monthly dividend stocks.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

Superior Plus Corporation (SUUIF) is one such company whose management team has decided to pay a monthly dividend to shareholders. And, the company has a substantial dividend yield.

As of today, Superior Plus yields 6.5% – about four times the 1.6% dividend yield of the S&P 500. The high dividend yield and the monthly dividend payments of Superior Plus are two reasons why investors might take interest in this stock.

This article will analyze the investment prospects of Superior Plus in detail to determine whether the company merits consideration for the portfolios of income-oriented investors.

Business Overview

Superior Plus Corporation is a relatively small industrial company but one of the larger propane distributors in North America. The company is the dominant distributor in Canada (30% of EBITDA), has significant operations in the U.S. (60% of EBITDA), and is also a propane wholesaler (10% of EBITDA). Superior Plus generates around $3.8 billion in annual revenues and is based in Toronto, Canada.

The company previously had a large Specialty Chemicals segment but sold this business in 2021 as part of a broader restructuring. Superior Plus is reorganizing its business to become a pure-play distribution company.

Superior Plus’ Energy Distribution segment is involved in the distribution and retail marketing of propane products, fuels (including heating oil and propane gas), and wholesale liquids marketing services. This segment operates primarily in Canada but has been expanding into the United States through a series of acquisitions that began in 2009. The Energy Distribution segment is operated under the trade names ‘Superior Propane’ or ‘Superior Gas Liquids’.

It should be noted that Superior Plus is an international stock – the company trades on the Toronto Stock Exchange under the ticker SPB and reports financials in Canadian dollars. Buying stocks based outside the U.S. presents a number of unique risks, such as currency risk. During rough economic periods, most foreign currencies weaken against the USD, and thus the earnings of international companies in USD decrease. Regardless, all figures in this article have been converted to USD.

Growth Prospects

Like many energy companies, Superior Plus was negatively impacted by the coronavirus pandemic and the resultant recession in the United States. As a result, the company incurred a 26% decrease in its earnings per share, from $1.63 in 2019 to $1.21 in 2020.

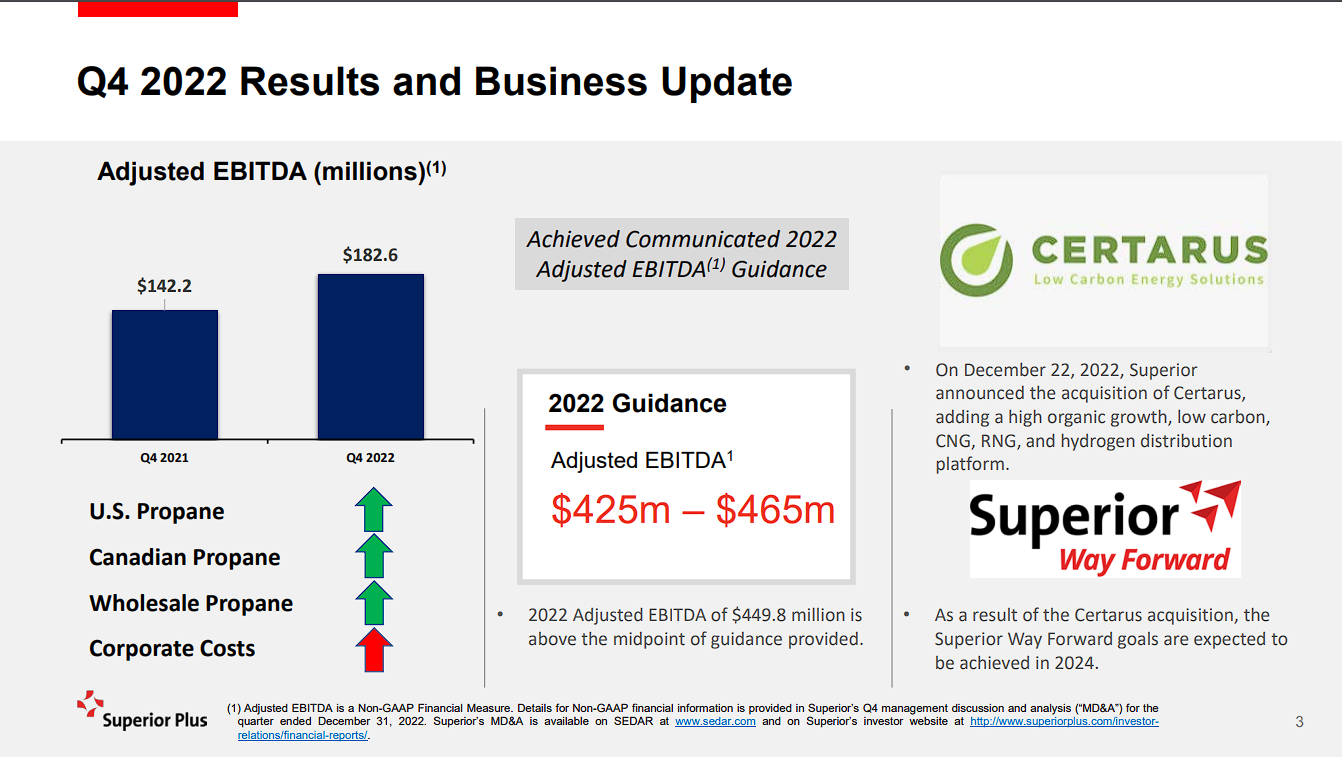

However, the company has stabilized its performance in recent quarters. In Q4 of 2022, the company generated an adjusted EBITDA of $135.7 million, a $30 million increase compared to the prior-year quarter.

Source: Investor Presentation

The increase was due to lower Adjusted EBITDA from all three segments following several acquisitions over the past four quarters. Adjusted operating cash flow per share totaled $0.25, compared to $0.45 last year, primarily due to transaction, restructuring, and other costs related to the company’s recent acquisitions, as well as a higher share count.

For the year, AOCF per share was $0.91, down from $1.22 in fiscal 2021, for the same reasons. Given the strong recovery of oil and gas stocks in 2022, the decline in Superior Plus’s AOCF is somewhat disappointing. Overall, the propane business has proved much more resilient to the pandemic than the oil industry but has much less upside during boom times.

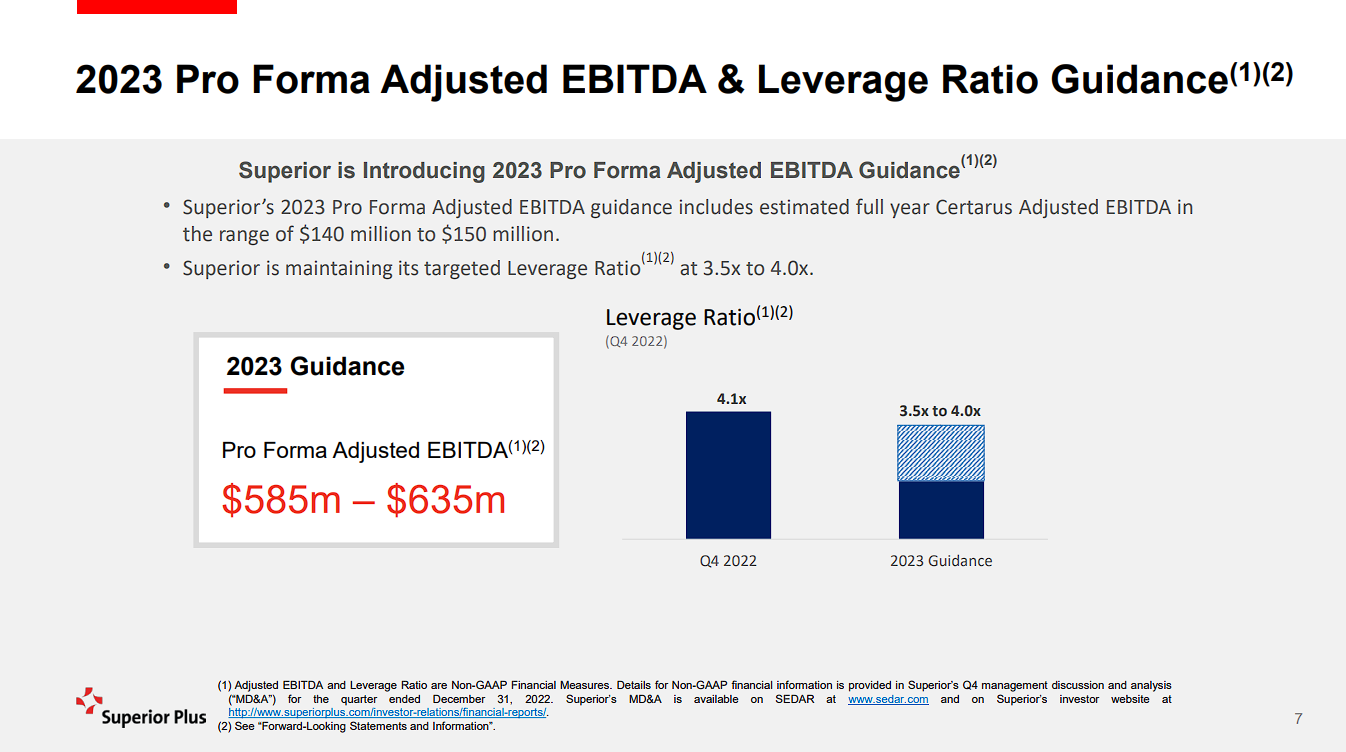

On the bright side, management introduced its FY2023 outlook, expecting adjusted EBITDA to be in the range of C$585 million to C$635 million, suggesting a 35.6% increase year-over-year in its midpoint. Accordingly, for the year, we respect CFPS/share of about $1.00, which takes into account the recent dilution and the possibility for more costs to accrue amid further acquisitions.

Source: Investor Presentation

Our CFPS/share estimate implies a year-over-year increase of 9.9% compared to fiscal 2022.

Competitive Advantages & Recession Performance

As an operator in the energy distribution industry, Superior Plus has competitive advantages, benefiting from regulatory barriers to entry and significant upfront capital outlays to enter the market. Unfortunately, Superior Plus has not proved resilient to all economic environments.

A company showing such outsized earnings-per-share declines can be expected to also cut its dividend when it reports losses. Indeed, Superior Plus cut its dividend twice in 2011. More recently, the company did make it through 2020 without reducing its dividend, a remarkable accomplishment gave the fierce recession caused by the pandemic.

On the other hand, Superior Plus has increased its financial leverage lately. Management has raised its target leverage ratio (Total Debt to Adjusted EBITDA) from 3.0-3.5 to 3.5-4.0 in order to perform more acquisitions. The ratio is elevated right now, standing at 4.1. The increased leverage of Superior Plus has somewhat reduced its resilience to unforeseen downturns.

Dividend Analysis

The dividend yield will likely make up most of the returns of Superior Plus going forward, given the lack of share price growth over the last decade. Superior Plus currently distributes a monthly dividend of $0.06 per share in CAD, or C$0.72 per share annualized. At present exchange rates, this works out to approximately $0.54 per share in U.S. dollars.

The company has distributed the same dividend for several years in a row. U.S. investors need to keep in mind that the company pays its dividend in Canadian currency, which will have an impact on actual capital received based on the fluctuations in exchange rates. Based on an annualized dividend payout of $0.54 per share, Superior stock has a current dividend yield of 6.5%.

Superior Plus is expected to earn $1.00 this year in U.S. dollars, giving the company a projected payout ratio of 54% for 2023. The dividend appears to be safe for the foreseeable future, thanks to the low payout ratio. On the other hand, Superior Plus has not raised its dividend for years and is not expected to in the near future.

As such, we feel that Superior Plus is a risky stock for income investors to hold, particularly during a downturn in commodities or a global recession.

Final Thoughts

The high dividend yield and the monthly dividend payments of Superior Plus help this stock to stand out relative to other dividend investments, particularly for income-focused investors like retirees.

That said, our due diligence reveals that this particular security has an underwhelming track record. Investors should not expect a dividend raise anytime soon.

Moreover, we do not expect material earnings-per-share growth or an expanding valuation multiple, leaving dividends as the primary source of expected returns. Nevertheless, for investors solely interested in income, the stock of Superior Plus could be appealing on that basis.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more