Updated on October 27th, 2023

Like it protected castles from plunderers in olden times, a moat protects a company from competitors in the business world. A company’s moat can be thought of as its competitive advantages, namely its advantages over competitors.

This moat can be narrow or it can be wide. A narrow moat is a smaller competitive advantage over peers, while a wide moat can mean the company has a significant advantage over peers, which likely protects its results through multiple economic cycles.

Narrow and wide moats have minimum life expectancy of 10+ and 20+ years, respectively, which they are anticipated to benefit the company.

We often see that companies with wide moats are better able to continue growing earnings and as a result, grow their dividends for many years. These companies also usually have strong margins in relation to their peers, as their moats protect their profits and market share.

Companies with wide moats can offer investors more peace of mind as they are generally more stable blue-chip stocks.

We created a full list of all 51 Dividend Kings. You can download the full list, along with important financial metrics such as dividend yields and price-to-earnings ratios, by clicking on the link below:

Below are ten wide moat dividend stocks that can be found in the VanEck Morningstar Wide Moat ETF (MOAT), which have respectable expected annual returns over the next five years.

Table of Contents

- Wide Moat Stock #10: Blackrock (BLK)

- Wide Moat Stock #9: Applied Materials (AMAT)

- Wide Moat Stock #8: MarketAxess Holdings Inc. (MKTX)

- Wide Moat Stock #7: Microsoft (MSFT)

- Wide Moat Stock #6: KLA Corp. (KLAC)

- Wide Moat Stock #5: Polaris (PII)

- Wide Moat Stock #4: Intercontinental Exchange Inc (ICE)

- Wide Moat Stock #3: State Street Corp. (STT)

- Wide Moat Stock #2: 3M Company (MMM)

- Wide Moat Stock #1: Comcast Corp. (CMCSA)

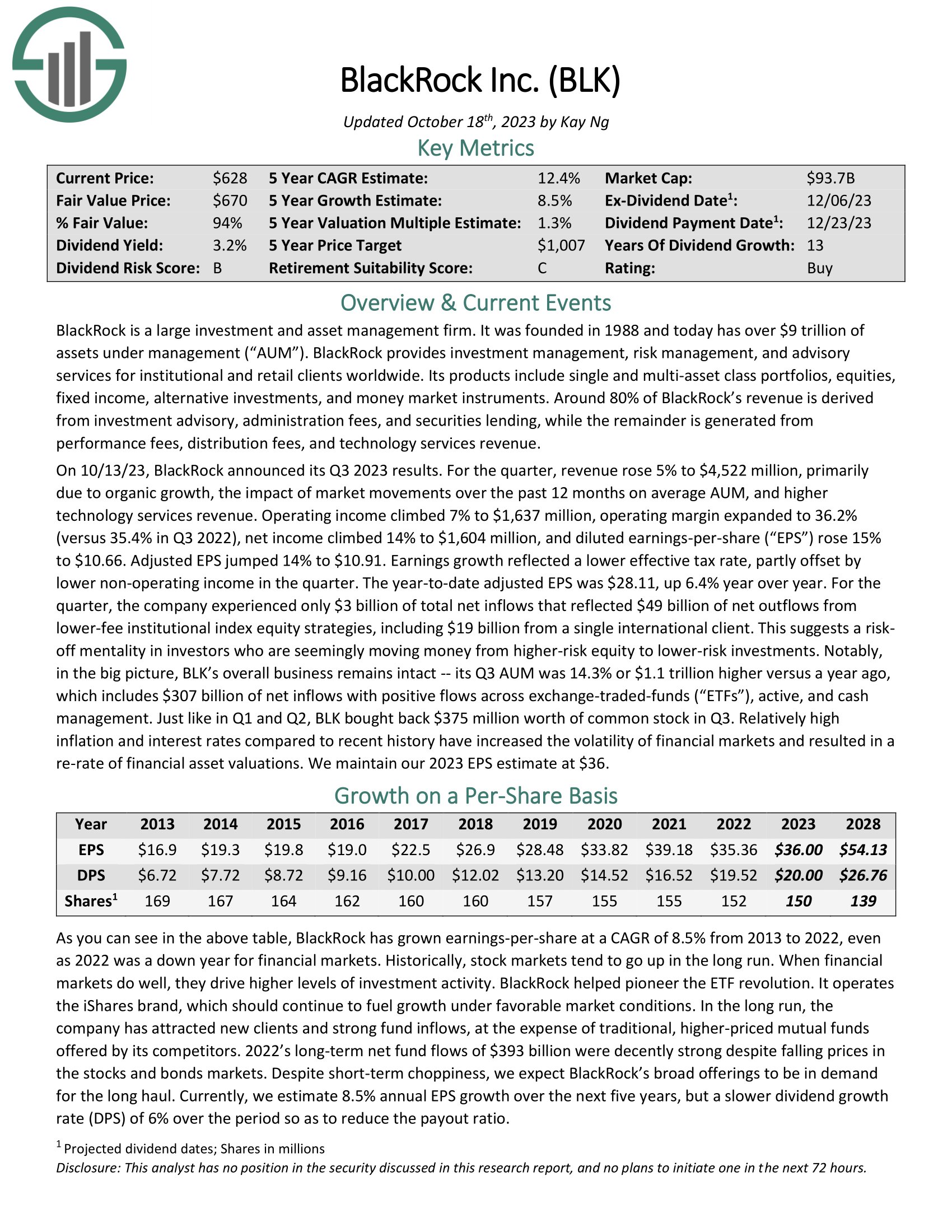

Wide Moat Stock #10: Blackrock (BLK)

BlackRock is a large investment and asset management firm. It was founded in 1988 and today has over $9 trillion of assets under management (“AUM”). BlackRock provides investment management, risk management, and advisory services for institutional and retail clients worldwide. Its products include single and multi-asset class portfolios, equities, fixed income, alternative investments, and money market instruments.

Around 80% of BlackRock’s revenue is derived from investment advisory, administration fees, and securities lending, while the remainder is generated from

performance fees, distribution fees, and technology services revenue.

On 10/13/23, BlackRock announced its Q3 2023 results. For the quarter, revenue rose 5% to $4,522 million, primarily due to organic growth, the impact of market movements over the past 12 months on average AUM, and higher technology services revenue.

Operating income climbed 7% to $1,637 million, operating margin expanded to 36.2% (versus 35.4% in Q3 2022), net income climbed 14% to $1,604 million, and diluted earnings-per-share (“EPS”) rose 15% to $10.66. Adjusted EPS jumped 14% to $10.91. Earnings growth reflected a lower effective tax rate, partly offset by lower non-operating income in the quarter.

Click here to download our most recent Sure Analysis report on Blackrock (preview of page 1 of 3 shown below):

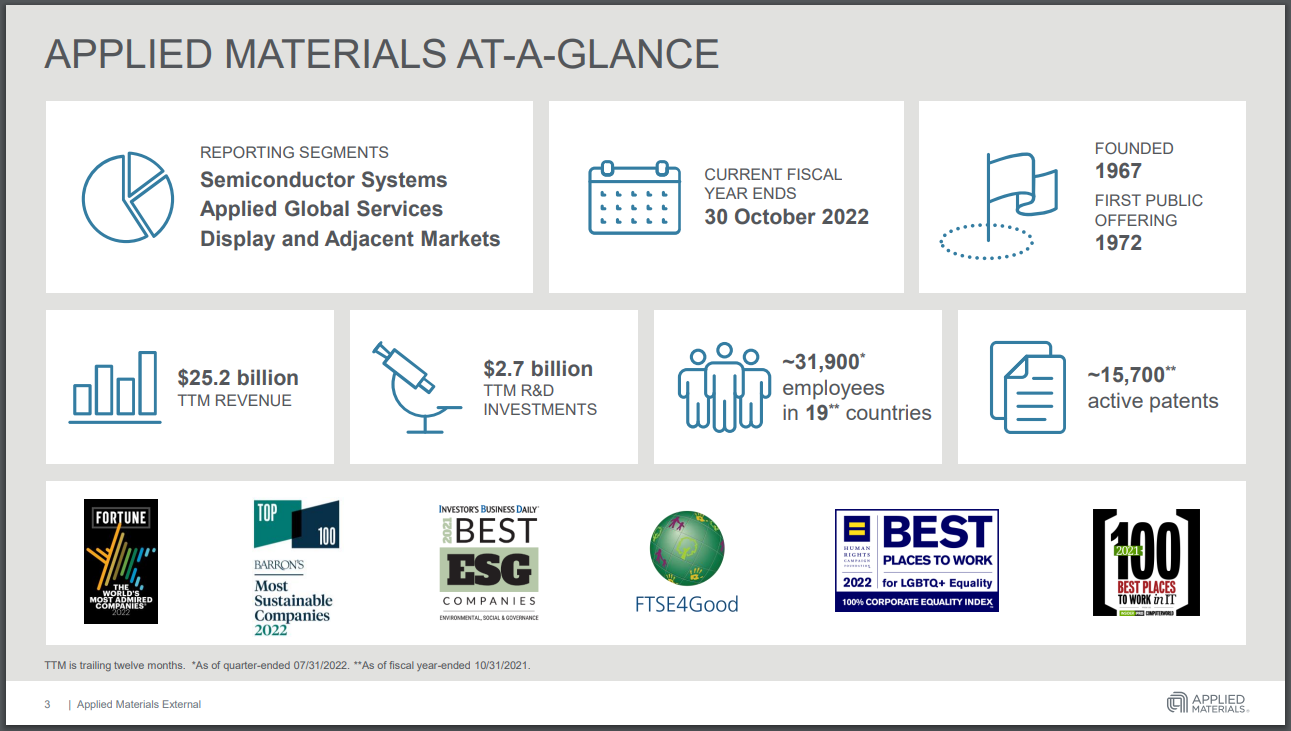

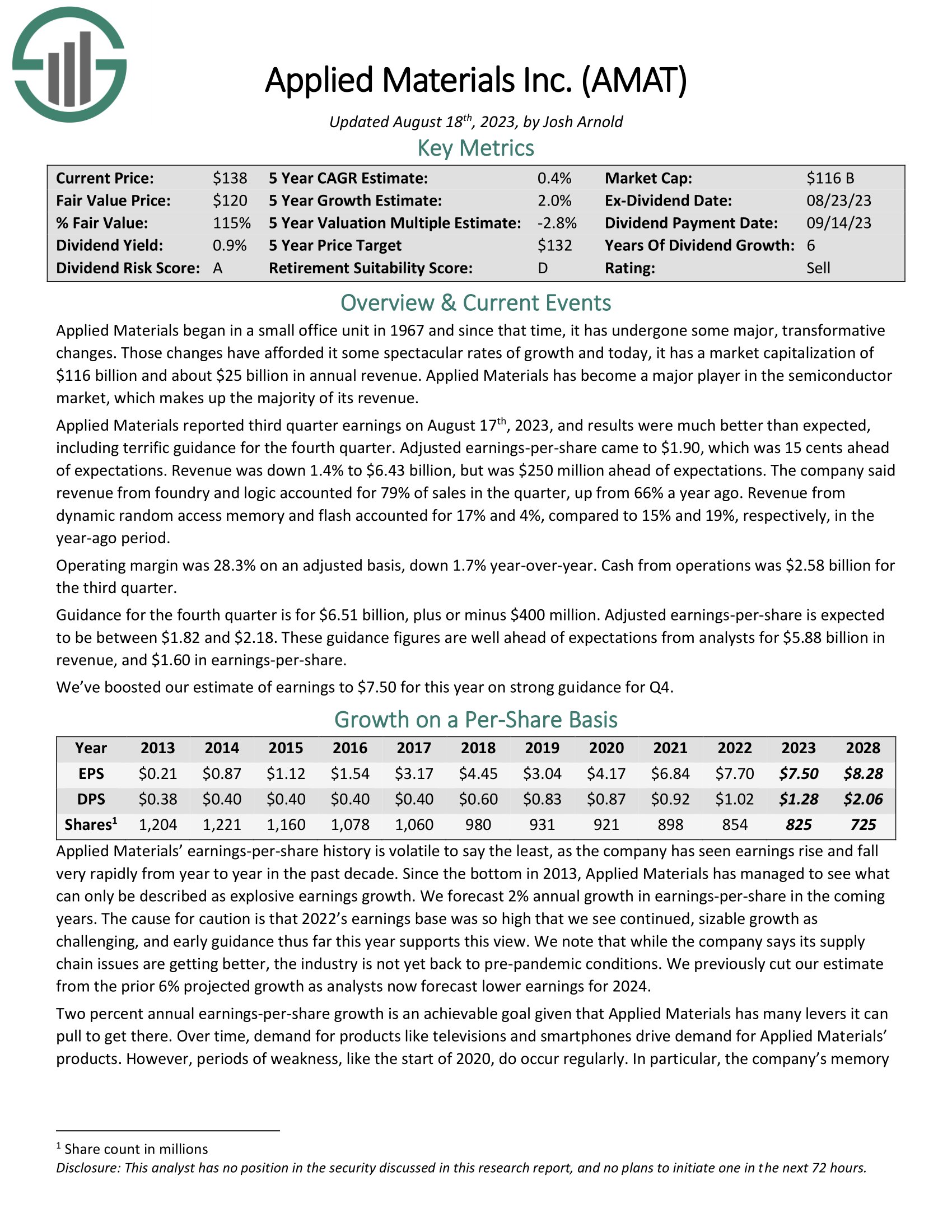

Wide Moat Stock #9: Applied Materials (AMAT)

Applied Materials began in a small office unit in 1967; since then, it has undergone some major, transformative changes. Those changes have afforded it some spectacular growth rates; today, it has a market capitalization of $85 billion and more than $25 billion in annual revenue. Applied Materials has become a major player in the semiconductor market, making up most of its revenue.

Source: Investor Presentation

Applied Materials reported third-quarter earnings on August 18th, 2022, and results beat analysts’ expectations on both the top and bottom lines. Adjusted earnings-per-share equaled $1.94, which was 15 cents ahead of estimates. Revenue grew 5.2% to $6.52 billion and beat expectations by $250 million.

Applied Materials’ long history of solving complex engineering problems and its entrenched customers is a benefit to the company. The company has created high customer switching costs with its excellent products, which we think is a long-term competitive advantage in a very competitive field. It is also seeing high rates of growth in its subscription business, which is well over half of its revenue now.

Click here to download our most recent Sure Analysis report on Applied Materials (preview of page 1 of 3 shown below):

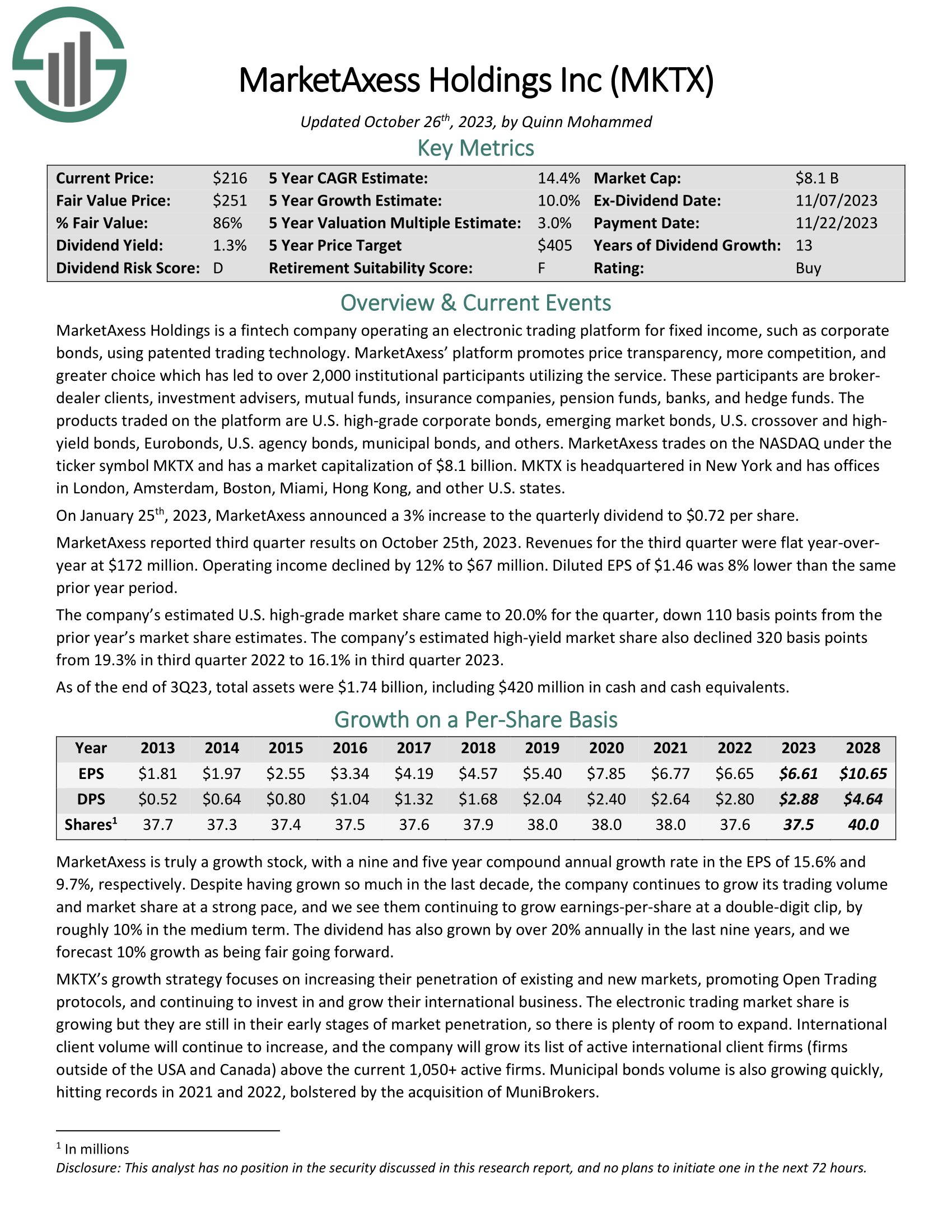

Wide Moat Stock #8: MarketAxess Holdings Inc. (MKTX)

MarketAxess Holdings is a fintech company operating an electronic trading platform for fixed income, such as corporate bonds, using patented trading technology. Over 1,900 institutional participants utilize the company’s service. These participants are broker-dealer clients, investment advisers, mutual funds, insurance companies, pension funds, banks, and hedge funds.

The products traded on the platform are U.S. high-grade corporate bonds, emerging market bonds, U.S. crossover, and high-yield bonds, Eurobonds, U.S. agency bonds, municipal bonds, and others.

MarketAxess reported third quarter results on October 25th, 2023. Revenues for the third quarter were flat year-over-year at $172 million. Operating income declined by 12% to $67 million. Diluted EPS of $1.46 was 8% lower than the same prior year period.

The company’s estimated U.S. high-grade market share came to 20.0% for the quarter, down 110 basis points from the prior year’s market share estimates. The company’s estimated high-yield market share also declined 320 basis points from 19.3% in third quarter 2022 to 16.1% in third quarter 2023.

Click here to download our most recent Sure Analysis report on MarketAxess Holdings Inc. (preview of page 1 of 3 shown below):

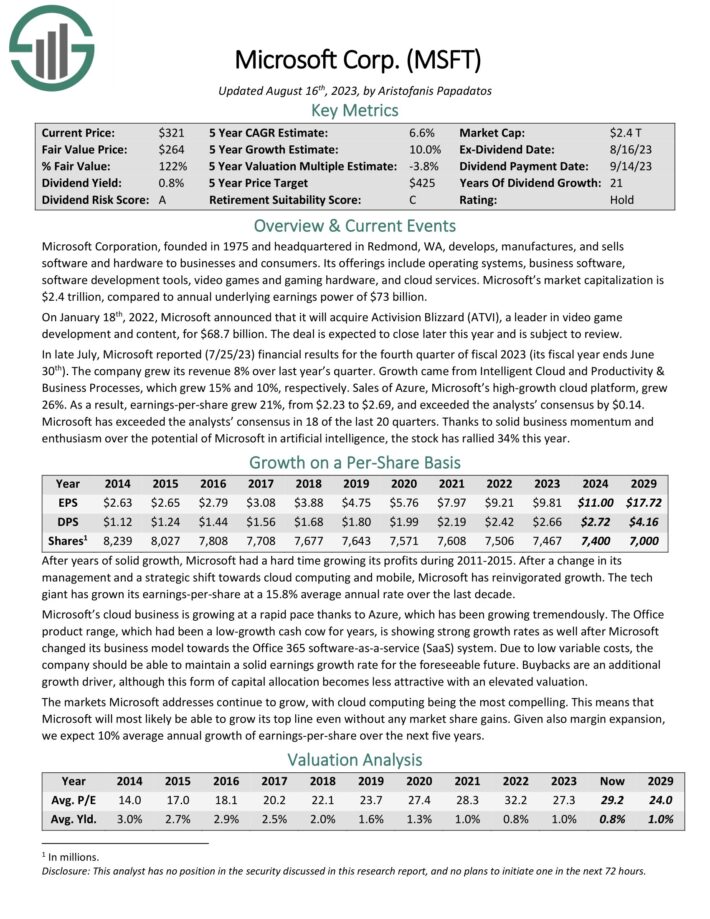

Wide Moat Stock #7: Microsoft (MSFT)

Microsoft Corporation, founded in 1975 and headquartered in Redmond, WA, develops, manufactures and sells both software and hardware to businesses and consumers.

Its offerings include operating systems, business software, software development tools, video games and gaming hardware, and cloud services.

In late July, Microsoft reported (7/25/23) financial results for the fourth quarter of fiscal 2023 (its fiscal year ends June 30th). The company grew its revenue 8% over last year’s quarter. Growth came from Intelligent Cloud and Productivity & Business Processes, which grew 15% and 10%, respectively.

Sales of Azure, Microsoft’s high-growth cloud platform, grew 26%. As a result, earnings-per-share grew 21%, from $2.23 to $2.69, and exceeded the analysts’ consensus by $0.14.

Click here to download our most recent Sure Analysis report on Microsoft (preview of page 1 of 3 shown below):

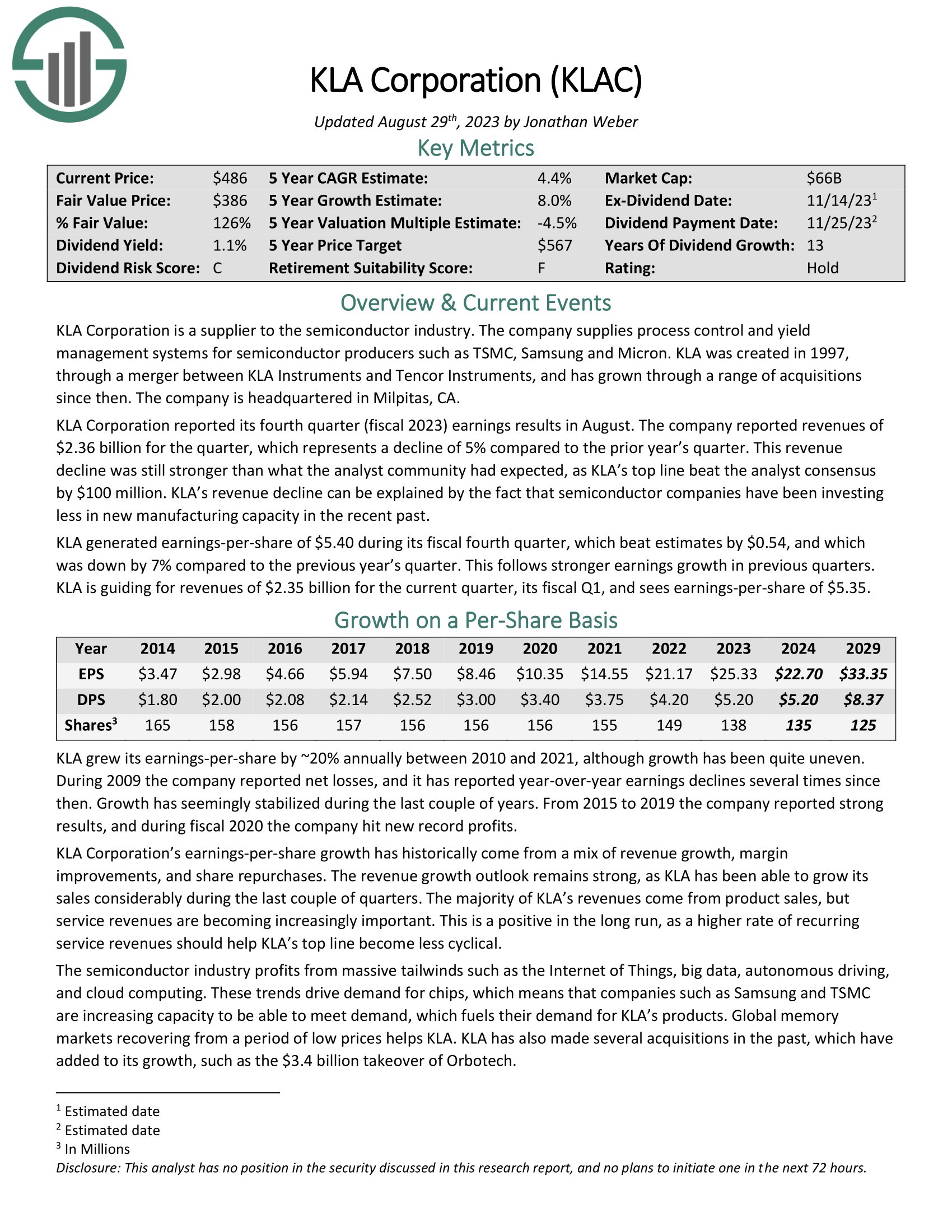

Wide Moat Stock #6: KLA Corp. (KLAC)

KLA Corporation is a supplier to the semiconductor industry. The company supplies process control and yield management systems for semiconductor producers such as TSMC, Samsung and Micron. KLA was created in 1997 through a merger between KLA Instruments and Tencor Instruments and has grown through a range of acquisitions since then.

KLA Corporation reported its fourth quarter (fiscal 2023) earnings results in August. The company reported revenues of $2.36 billion for the quarter, which represents a decline of 5% compared to the prior year’s quarter. This revenue decline was still stronger than what the analyst community had expected, as KLA’s top line beat the analyst consensus by $100 million. KLA’s revenue decline can be explained by the fact that semiconductor companies have been investing less in new manufacturing capacity in the recent past.

Click here to download our most recent Sure Analysis report on KLA Corp. (preview of page 1 of 3 shown below):

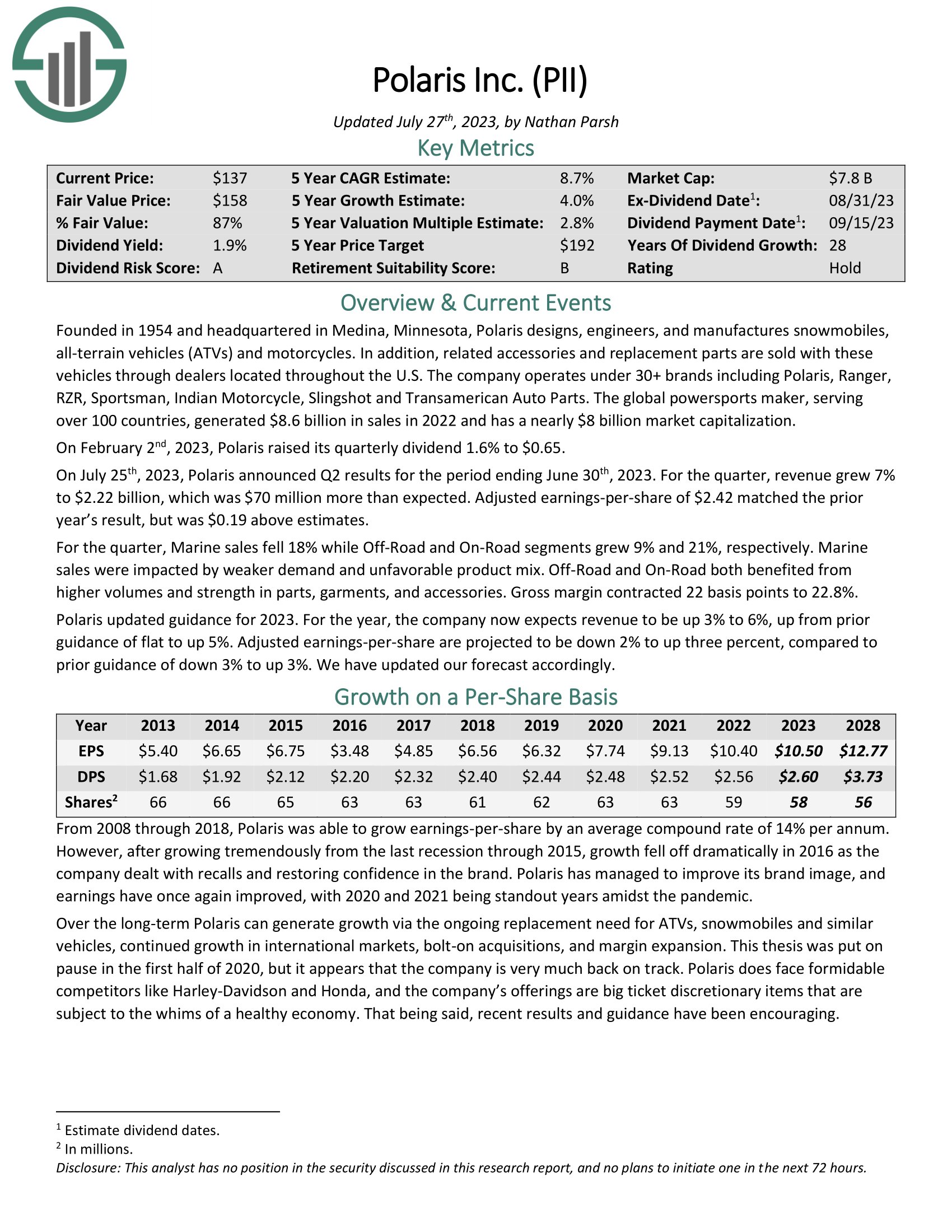

Wide Moat Stock #5: Polaris (PII)

Polaris designs, engineers, and manufactures snowmobiles, all-terrain vehicles (ATVs), and motorcycles. In addition, related accessories and replacement parts are sold with these vehicles through dealers located throughout the U.S.

The company operates under 30+ brands, including Polaris, Ranger, RZR, Sportsman, Indian Motorcycle, Slingshot, and Transamerican Auto Parts.

On October 25th, 2022, Polaris released Q3 results. Revenue increased 19.4% to $2.34 billion, beating estimates by $140 million. Adjusted earnings-per-share of $3.25 compared favorably to $2.85 in the prior year and was $0.47 above expectations.

Polaris enjoys a competitive advantage through its brand names, low-cost production, and long history in its various industries, allowing the company to be the leader in ATVs and number two in snowmobiles and domestic motorcycles.

Click here to download our most recent Sure Analysis report on Polaris (preview of page 1 of 3 shown below):

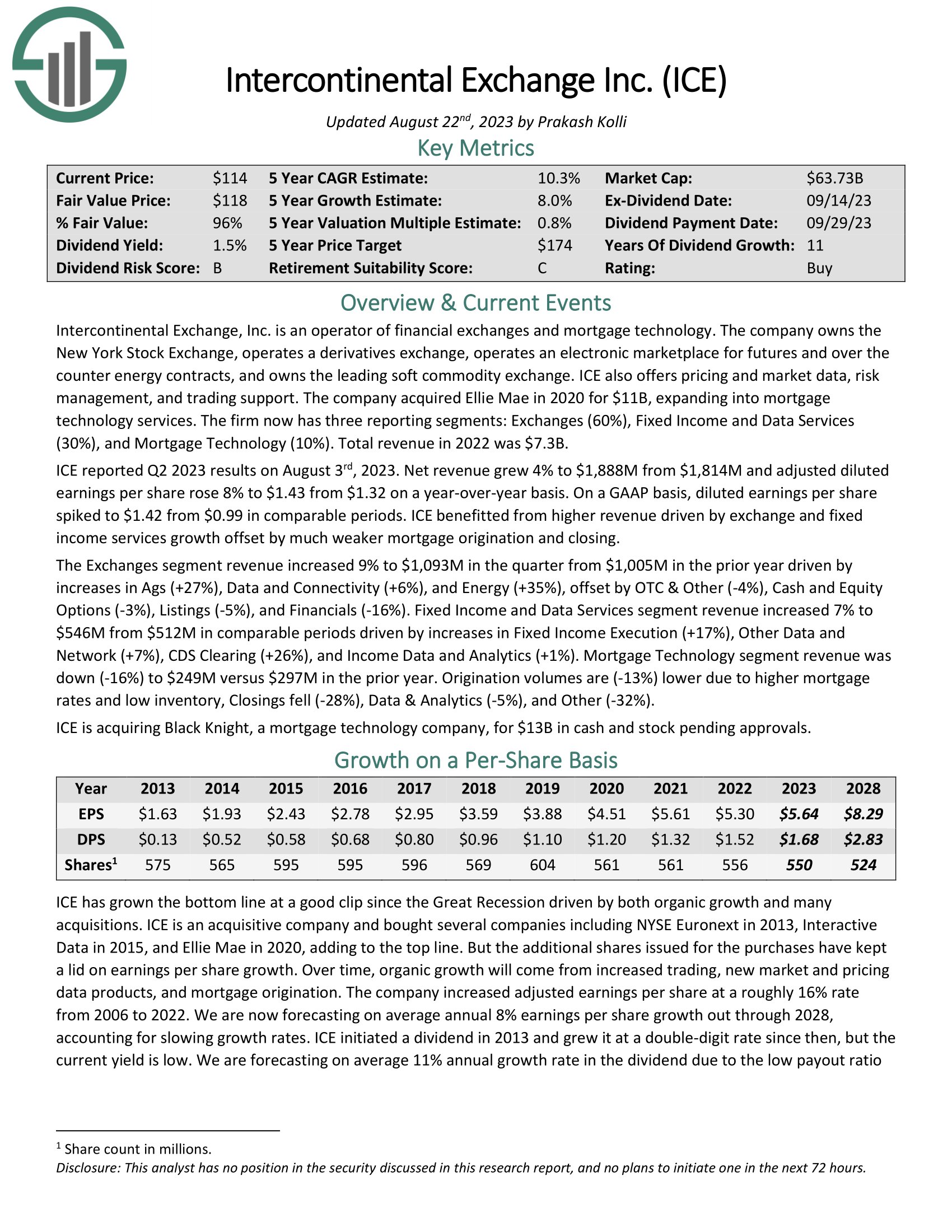

Wide Moat Stock #4: Intercontinental Exchange Inc (ICE)

Intercontinental Exchange, Inc. is an operator of financial exchanges and mortgage technology. The company owns the New York Stock Exchange, a derivatives exchange, an electronic marketplace for futures and over-the-counter energy contracts, and the leading soft commodity exchange.

ICE offers pricing, market data, risk management, and trading support. The company acquired Ellie Mae in 2020 for $11B, expanding into mortgage technology services.

ICE reported Q2 2023 results on August 3rd, 2023. Net revenue grew 4% to $1,888M from $1,814M and adjusted diluted earnings per share rose 8% to $1.43 from $1.32 on a year-over-year basis. On a GAAP basis, diluted earnings per share spiked to $1.42 from $0.99 in comparable periods. ICE benefited from higher revenue driven by exchange and fixed income services growth offset by much weaker mortgage origination and closing.

Click here to download our most recent Sure Analysis report on Intercontinental Exchange (preview of page 1 of 3 shown below):

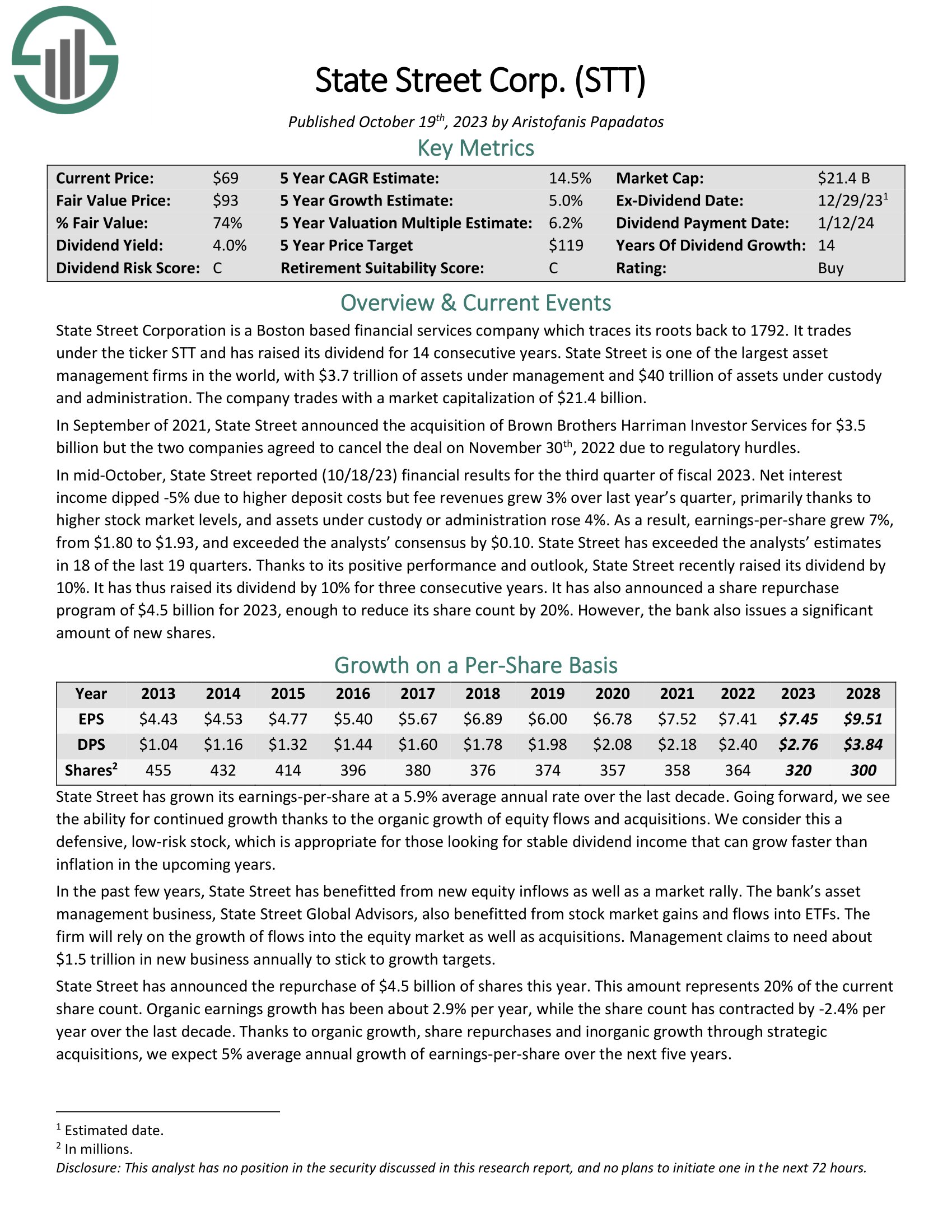

Wide Moat Stock #3: State Street Corp (STT)

is one of the largest asset management firms in the world, with more than $3 trillion of assets under management and $36 trillion of assets under custody and administration. The company has annual revenue of $12 billion.

In mid-October, State Street reported (10/18/23) financial results for the third quarter of fiscal 2023. Net interest income dipped -5% due to higher deposit costs but fee revenues grew 3% over last year’s quarter, primarily thanks to higher stock market levels, and assets under custody or administration rose 4%. As a result, earnings-per-share grew 7%, from $1.80 to $1.93, and exceeded the analysts’ consensus by $0.10. State Street has exceeded the analysts’ estimates in 18 of the last 19 quarters.

Shares of State Street yield 4.3%, and the company has a dividend growth streak of 14 years, which is the longest of the names discussed in this article.

Click here to download our most recent Sure Analysis report on State Street Corp. (preview of page 1 of 3 shown below):

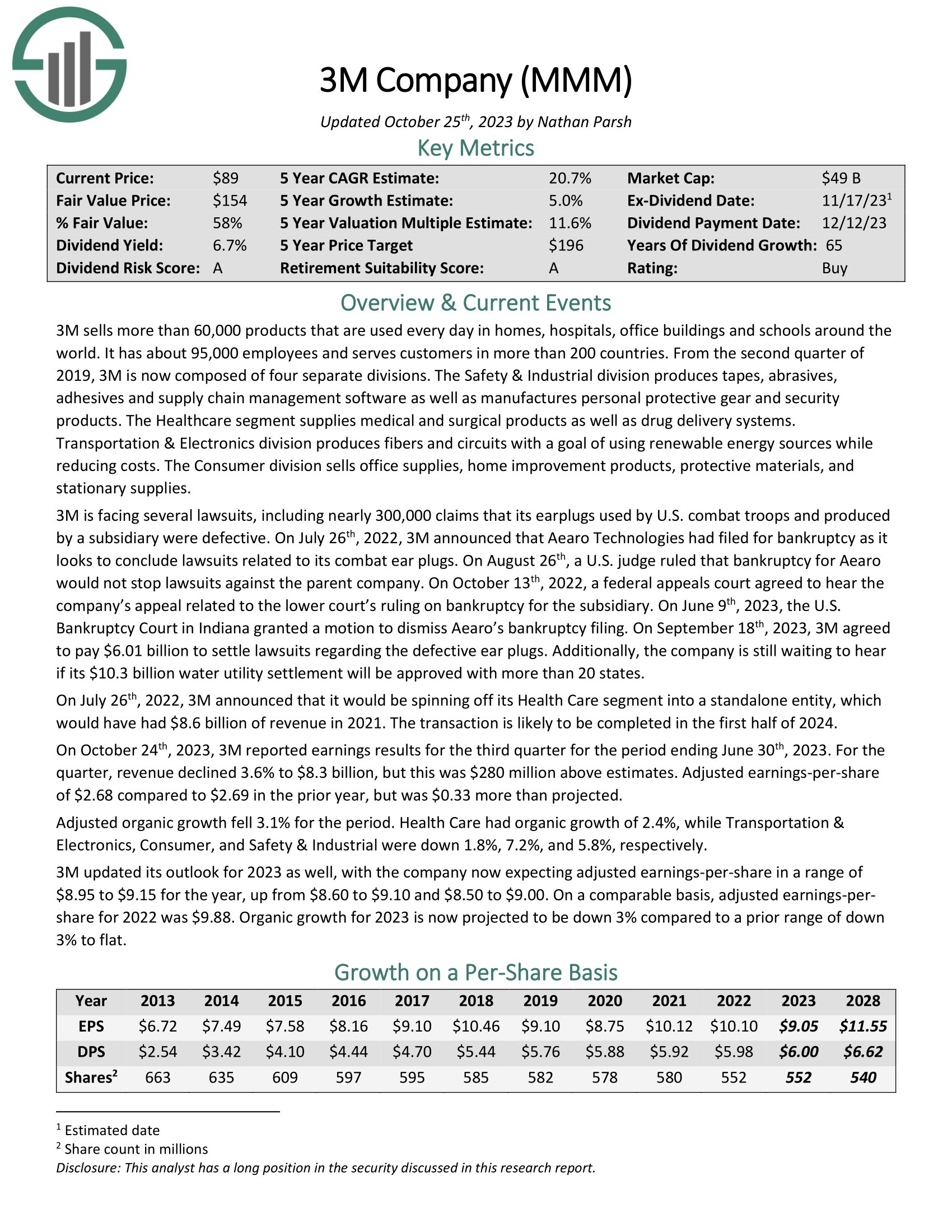

Wide Moat Stock #2: 3M Company (MMM)

3M is an industrial manufacturer that sells more than 60,000 products used daily in homes, hospitals, office buildings, and schools worldwide. It has about 95,000 employees and serves customers in more than 200 countries.

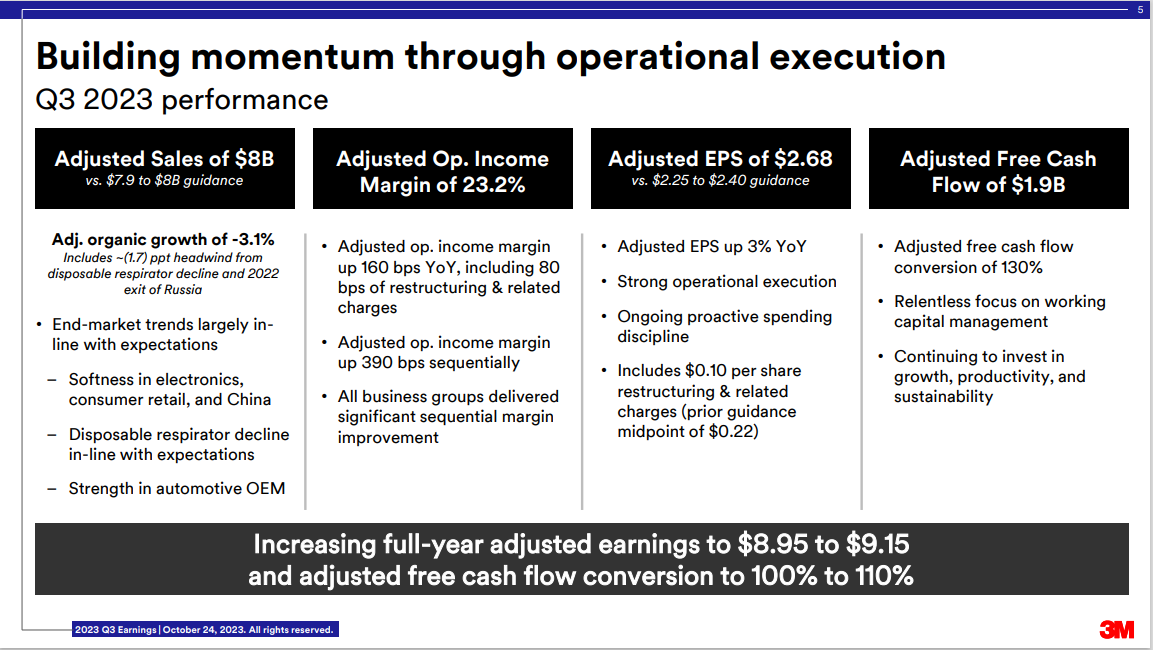

On October 24th, 2023, 3M reported earnings results for the third quarter for the period ending June 30th, 2023.

Source: Investor Presentation

For the quarter, revenue declined 3.6% to $8.3 billion, but this was $280 million above estimates. Adjusted earnings-per share of $2.68 compared to $2.69 in the prior year, but was $0.33 more than projected.

Adjusted organic growth fell 3.1% for the period. Health Care had organic growth of 2.4%, while Transportation & Electronics, Consumer, and Safety & Industrial were down 1.8%, 7.2%, and 5.8%, respectively.

Click here to download our most recent Sure Analysis report on 3M Company (preview of page 1 of 3 shown below):

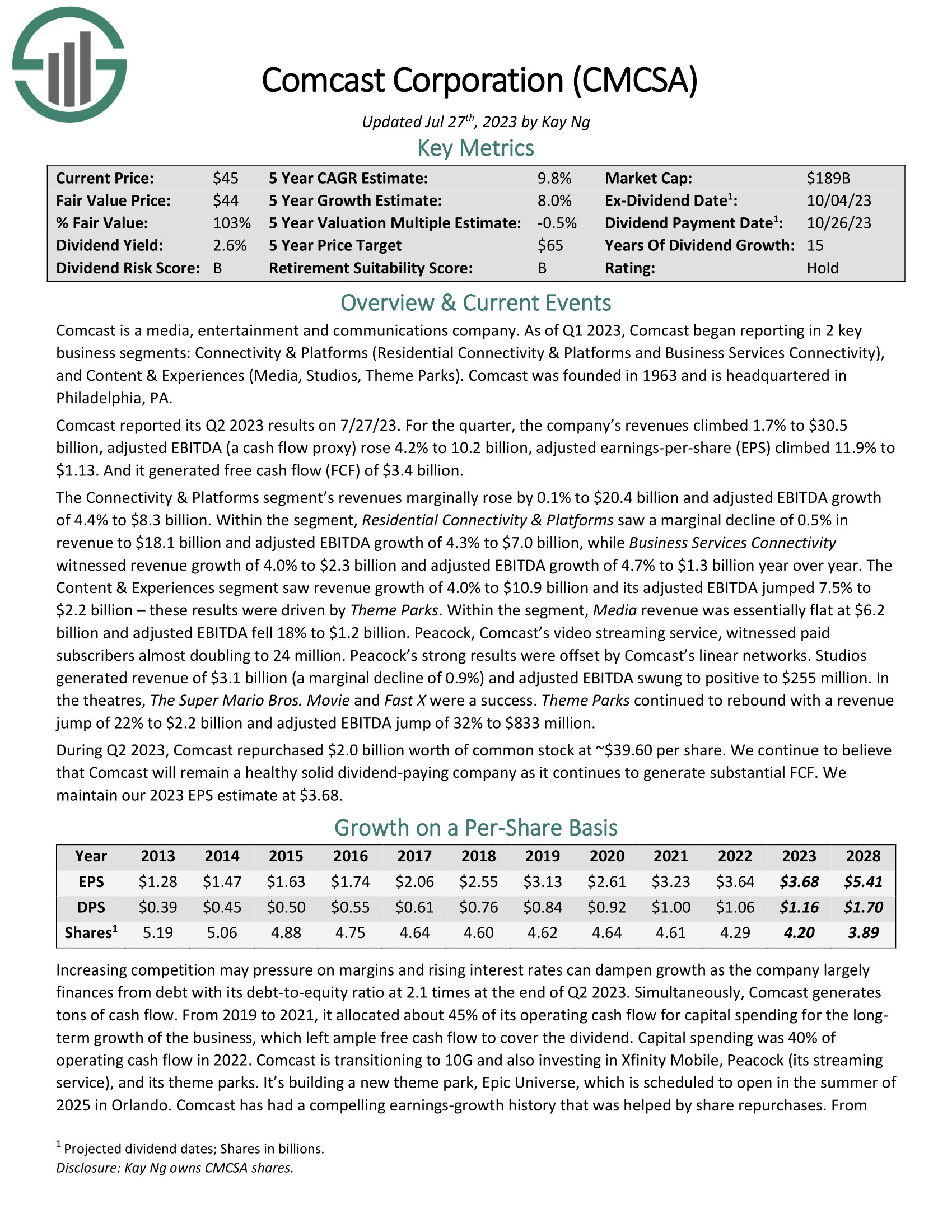

Wide Moat Stock #1: Comcast Corp. (CMCSA)

Comcast is a media, entertainment, and communications company. Its business units include Cable Communications (High-Speed Internet, Video, Business Services, Voice, Advertising, Wireless), NBCUniversal (Cable Networks, Theme Parks, Broadcast TV, Filmed Entertainment), and Sky, a leading entertainment company in Europe that provides Video, High-speed internet, Voice, and Wireless Phone Services directly to consumers.

Comcast reported its Q2 2023 results on 7/27/23. For the quarter, the company’s revenues climbed 1.7% to $30.5 billion, adjusted EBITDA (a cash flow proxy) rose 4.2% to 10.2 billion, adjusted earnings-per-share (EPS) climbed 11.9% to $1.13. And it generated free cash flow (FCF) of $3.4 billion.

The Connectivity & Platforms segment’s revenues marginally rose by 0.1% to $20.4 billion and adjusted EBITDA growth of 4.4% to $8.3 billion. Within the segment, Residential Connectivity & Platforms saw a marginal decline of 0.5% in revenue to $18.1 billion and adjusted EBITDA growth of 4.3% to $7.0 billion, while Business Services Connectivity witnessed revenue growth of 4.0% to $2.3 billion and adjusted EBITDA growth of 4.7% to $1.3 billion year over year.

Click here to download our most recent Sure Analysis report on Comcast Corp. (preview of page 1 of 3 shown below):

Final Thoughts

Wide moat stocks have great competitive advantages with staying power. These advantages often allow the company to flourish through multiple economic cycles with growing earnings. As a result, these companies frequently sport strong dividend increase records.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Aristocrats List: S&P 500 Index stocks with 25+ years of dividend increases.

- The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields.

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The 20 Highest Yielding Monthly Dividend Stocks

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.