Updated on September 26th, 2024 by Bob Ciura

Investors looking for companies that generate strong profits and pay dividends should take a closer look at the major alcohol stocks. These are companies that manufacture and distribute a variety of alcoholic beverages, including beer, wine, and liquor.

The top companies in this industry have many attractive qualities. They have popular brands, which give them pricing power and strong cash flow. This allows them to pay dividends to shareholders.

Alcohol stocks also tend to perform well during periods of economic downturns, meaning they can provide diversification and recession-resistance to a portfolio.

To the point, one alcohol stock even makes the exclusive Dividend Aristocrats list, an elite group of S&P 500 stocks with 25+ years of rising dividends.

There are currently 66 Dividend Aristocrats. You can download an Excel spreadsheet of all 66 Dividend Aristocrats (with metrics that matter such as dividend yields and payout ratios) by clicking the link below:

More information can be found in the Sure Analysis Research Database, which ranks stocks based upon the combination of their dividend yield, earnings-per-share growth potential and valuation changes to compute total returns.

This article will rank the top alcohol stocks right now.

Table of Contents

The top alcohol stocks are listed here. Stocks are ranked according to their 5-year expected returns. Stocks are listed in order of attractiveness, from lowest to highest.

- Alcohol Stock #5: Anheuser-Busch InBev (BUD)

- Alcohol Stock #4: Brown-Forman (BF.B)

- Alcohol Stock #3: Molson Coors (TAP)

- Alcohol Stock #2: Diageo plc (DEO)

- Alcohol Stock #1: Constellation Brands (STZ)

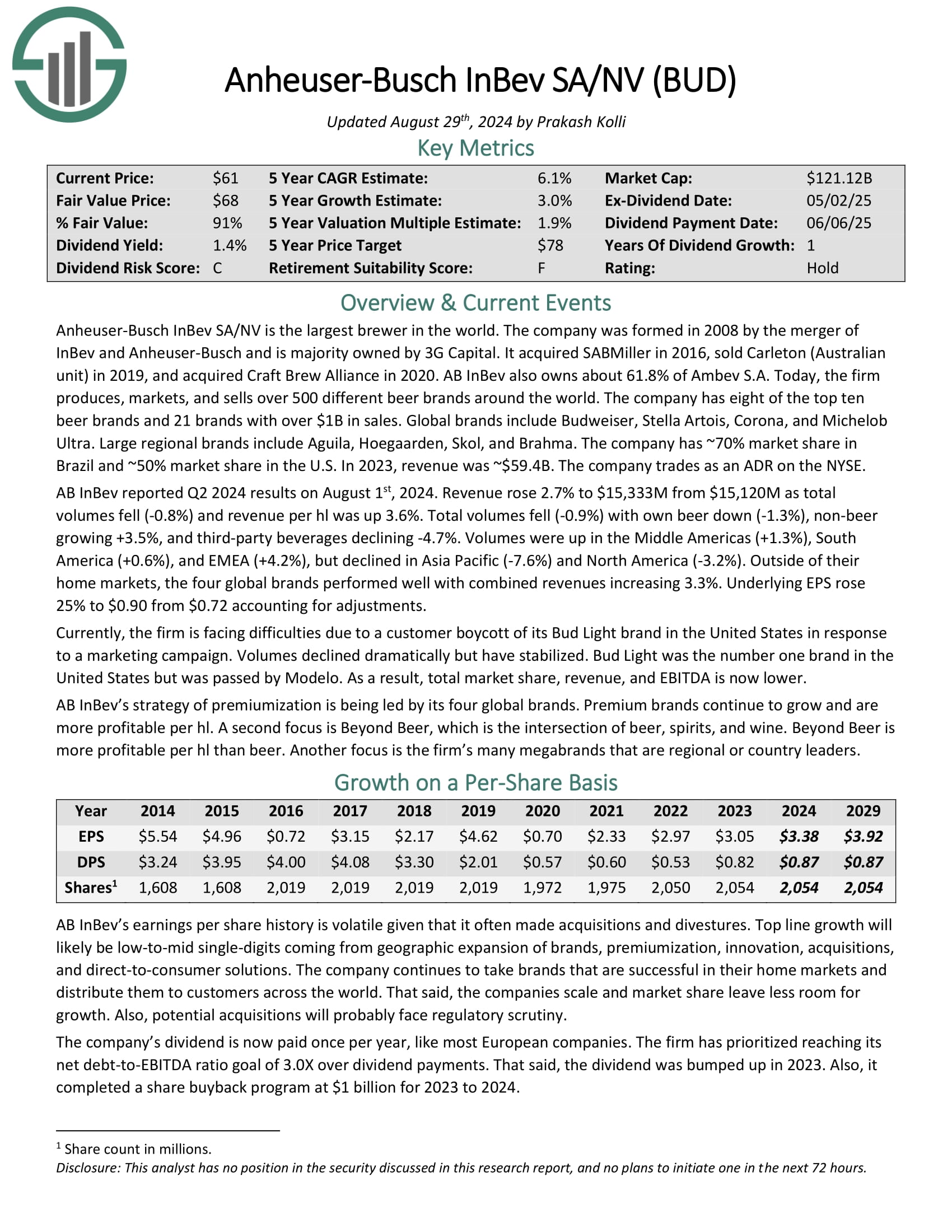

Alcohol Stock #5: Anheuser-Busch InBev (BUD)

- 5-year expected annual returns: 5.1%

AB-InBev is the largest beer company in the world. In its current form, it is the result of the 2008 merger between InBev and Anheuser-Busch. Today, it sells more than 500 beer brands, in more than 150 countries around the world. Some of its most popular brands include Budweiser, Bud Light, Corona, Stella Artois, Beck’s, Castle, and Skol.

AB InBev reported Q2 2024 results on August 1st, 2024. Revenue rose 2.7% to $15,333M from $15,120M as total volumes fell (-0.8%) and revenue per hl was up 3.6%. Total volumes fell (-0.9%) with own beer down (-1.3%), non-beer growing +3.5%, and third-party beverages declining -4.7%.

Volumes were up in the Middle Americas (+1.3%), South America (+0.6%), and EMEA (+4.2%), but declined in Asia Pacific (-7.6%) and North America (-3.2%). Outside of their home markets, the four global brands performed well with combined revenues increasing 3.3%. Underlying EPS rose 25% to $0.90 from $0.72 accounting for adjustments.

Click here to download our most recent Sure Analysis report on BUD (preview of page 1 of 3 shown below):

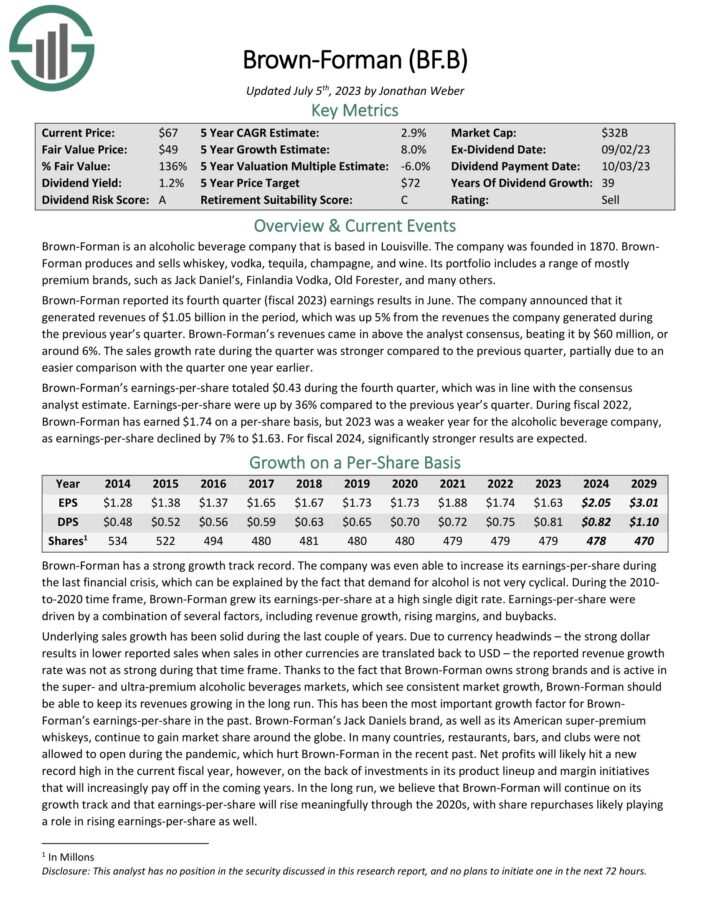

Alcohol Stock #4: Brown-Forman (BF.B)

- 5-year expected annual returns: 7.8%

Brown-Forman has an impressive history of dividend growth. The company has increased its dividend for over 30 years in a row, making it a Dividend Aristocrat.

Brown-Forman’s long dividend growth history is due to its strong brands and recession resiliency. It has a large product portfolio, which is focused on whiskey, vodka, and tequila. Its most famous brand is its flagship Jack Daniel’s. Other popular brands include Herradura, Woodford Reserve, El Jimador, and Finlandia.

Click here to download our most recent Sure Analysis report on Brown-Forman (preview of page 1 of 3 shown below):

Alcohol Stock #3: Molson Coors (TAP)

- 5-year expected annual returns: 10.6%

Molson Coors Brewing Company was founded in 1873. Since then, it has grown into one of the largest U.S. brewers. It has a variety of brands including Coors Light, Coors Banquet, Molson Canadian, Carling, Blue Moon, Hop Valley, Crispin Cider, and the Miller beer brands.

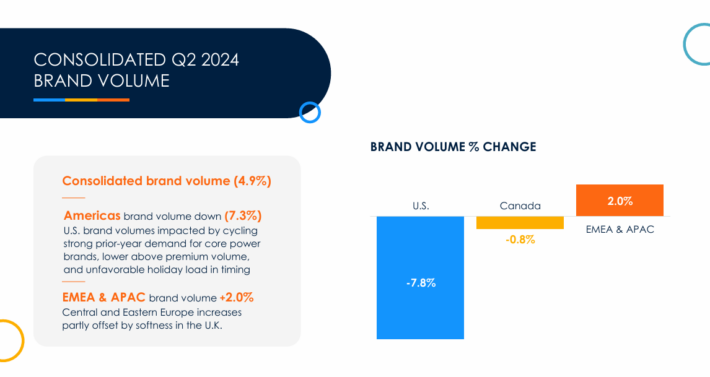

On August 6th, 2024, Molson Coors reported second quarter 2024 results for the period ending June 30th, 2024. For the quarter, the company generated net sales of $3.25 billion, a 0.4% decrease compared to Q2 2023.

Source: Investor Presentation

Net sales declined 1.7% in Americas, but improved 5.3% in Europe, the Middle East and Africa, and Asia-Pacific.

Reported net income equaled $560 million or $2.03 per share compared to $441 million or $1.57 per share in Q2 2023. On an adjusted basis, earnings-per-share equaled $1.92 versus $1.78 prior. The company repurchased $375 million of its shares in H1 2024.

Click here to download our most recent Sure Analysis report on Molson Coors (preview of page 1 of 3 shown below):

Alcohol Stock #2: Diageo PLC (DEO)

- 5-year expected annual returns: 10.8%

Diageo traces its roots all the way back to the 17th century and the Haig family, the oldest family of Scotch whiskey distillers.

Today, Diageo manufacturers some of the most popular spirits and beer brands in the world, such as Johnnie Walker, Smirnoff, Captain Morgan, Baileys, Tanqueray, Guinness, Crown Royal, Ketel One, and many more.

In all, Diageo has 20 of the world’s top 100 spirits brands.

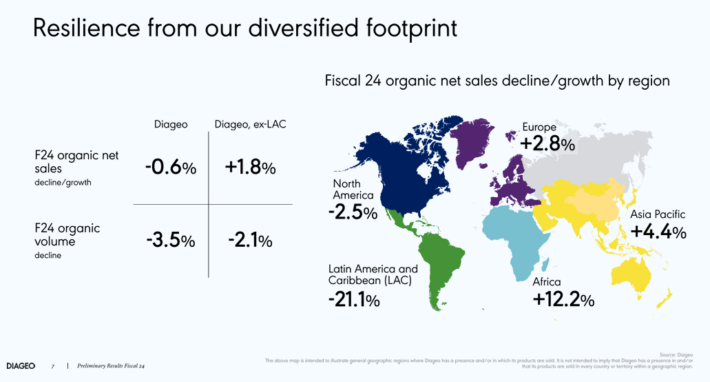

On July 30th, 2024, Diageo released earnings results for fiscal year 2024 for the period ending June 30th, 2023. For the year, the company earned $6.91 per share, which was 5% above the prior year’s result, but well below estimates. Net sales decreased 1.4% while organic growth was lower by 0.6%.

Source: Investor Presentation

A small benefit from pricing and mix was more than offset by a 3.5% decrease in volume. Most regions performed well. Organic revenue growth for Africa, Asia Pacific, and Europe totaled 12%, 4%, and 3%. North America was down 3% while Latin American and Caribbean was down 21%.

The decrease in North America was due to a cautious consumer market and tough comparable periods. Total market share grew or held steady in 75% of the portfolio, which compared to 70% in fiscal year 2023. Premium-plus brands accounted for the majority of net sales.

Click here to download our most recent Sure Analysis report on Diageo (preview of page 1 of 3 shown below):

Alcohol Stock #1: Constellation Brands (STZ)

- 5-year expected annual returns: 11.2%

Constellation Brands was founded in 1945, and today, it produces and distributes beer, wine, and spirits. It has over 100 brands in its portfolio, including beer brands such as Corona.

In addition, Constellation’s wine brands include Robert Mondavi and Clos du Bois. Its liquor brands include SVEDKA Vodka, Casa Noble Tequila, and High West Whiskey.

One of the biggest reasons for Constellation Brands’ impressive growth in recent years, is its focus on the premium segment, which continues to grow.

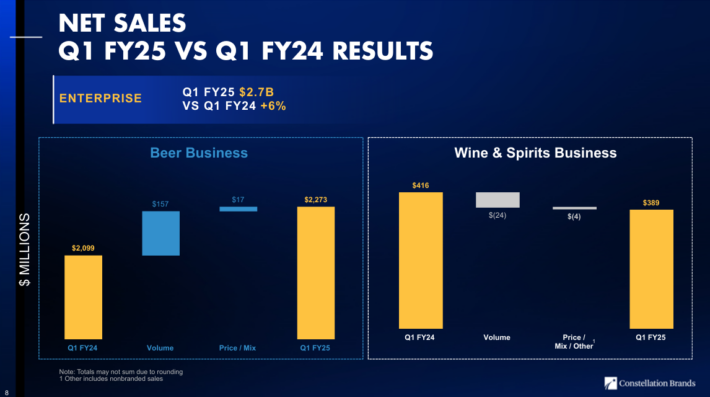

On July 3rd, 2024, Constellation Brands reported first quarter fiscal 2025 results for the period ending May 31st, 2024.

Source: Investor Presentation

For the first quarter, the company recorded $2.66 billion in net sales, a 6% increase compared to the same prior year period. Beer sales improved by 8% year-over-year, while wine and spirits sales declined by 7%.

Comparable earnings-per-share equaled $3.57 for the quarter, which was a 17% increase compared to Q1 2024, and 12 cents ahead of analyst estimates.

Click here to download our most recent Sure Analysis report on STZ (preview of page 1 of 3 shown below):

Final Thoughts

Many alcohol stocks were hit hard as the coronavirus crisis unfolded, but some have come back significantly in recent months. For value and income investors, the recovery in alcohol stocks has reduced the number of buying opportunities due to rising valuations and declining dividend yields.

Still, the world’s best alcohol manufacturers have strong brands, and generate high cash flow that is used for growth investment as well as cash returns to shareholders.

It is also valuable for investors that alcohol stocks are likely to be among the best-performers if a recession does occur. Consumption of alcoholic beverages will stay steady–and could even increase–in a recession. A sustained recovery from the coronavirus would be a major benefit for the biggest alcohol manufacturers.

If you are interested in finding high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The Dividend Champions List: a broader group of stocks with 25+ years of consecutive dividend increases, without the S&P 500 Index inclusion requirement.

- The Dividend Challengers List: stocks with 5-9 years of consecutive dividend increases.

- The Dividend Achievers List: a group of stocks with 10-24 years of consecutive dividend increases.

- The Dividend Kings List: considered to be the best-of-the-best among dividend growth stocks, the Dividend Kings are a group of exceptional dividend stocks with 50+ years of consecutive dividend increases.

- The Blue Chip Stocks List: contains stocks on either the Dividend Achievers, Dividend Aristocrats, or Dividend Kings list.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.