Updated on March 5th, 2026 by Nathan Parsh

Chevron Corporation (CVX) is one of the world’s largest and most well-known energy stocks. It is also one of the energy sector’s most stable dividend growth companies, having grown its dividend for 39 consecutive years.

As a result, Chevron is a member of the exclusive Dividend Aristocrats – a group of 69 elite dividend stocks with 25+ years of consecutive dividend increases.

We believe the Dividend Aristocrats are some of the highest-quality dividend stocks in the entire stock market. With this in mind, we created a full list of all 69 Dividend Aristocrats, along with important financial metrics such as dividend yields and P/E ratios.

You can download a copy of our full Dividend Aristocrats list by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Due to the industry’s reliance on high commodity prices for profitability, only two oil stocks are on the list of Dividend Aristocrats: Chevron and Exxon Mobil (XOM).

Chevron’s dividend consistency and stability help it stand out in the otherwise volatile energy industry. This article will analyze Chevron’s intermediate-term investment prospects.

Business Overview

Chevron is one of 6 integrated oil and gas super-majors, along with:

- BP (BP)

- Eni SpA (E)

- TotalEnergies (TTE)

- Exxon Mobil (XOM)

- Shell (SHEL)

Like the other integrated supermajors, Chevron engages in upstream oil and gas production and downstream refining businesses. In 2025, Chevron generated $12.8 billion of its earnings from its upstream segment compared to $3 billion from its downstream segment. Therefore, it is highly sensitive to the underlying commodity price.

Global oil demand has continued to increase in the years since the coronavirus pandemic steadily. Separately, oil and gas prices have been elevated due to the war in Ukraine and resulting sanctions on Russia. Before the sanctions, Russia was producing about 10% of global oil output and one-third of natural gas consumed in Europe. In addition, the recent rise in conflict in Iran has also impacted the price of oil.

The benefit from these exceptionally favorable conditions was evident in Chevron’s performance in 2022, although conditions softened in 2023 and 2024 as oil and gas prices moderated off their peaks.

Chevron posted mixed financial results to end 2025.

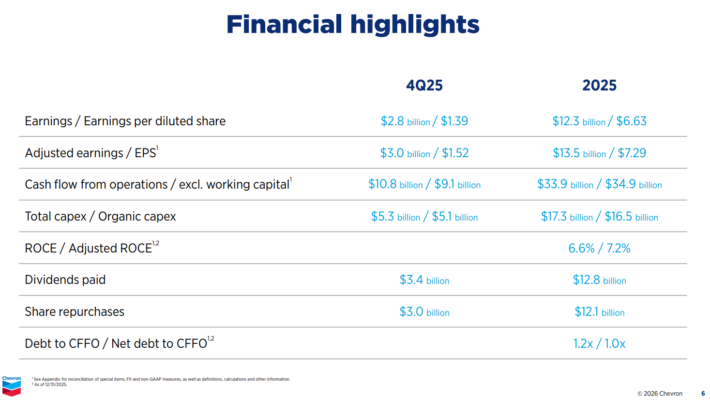

Source: Investor Presentation

At the end of January, Chevron reported (1/30/25) earnings for the fourth quarter and full year. The company’s fourth-quarter 2025 adjusted earnings of $3.0 billion ($1.52 per share), was down from $3.6 billion ($1.85) in fourth-quarter 2024. Revenue declined 10.3% to $46.9 billion. The company did best estimates for both revenue and adjusted earnings-per-share.

Production surged 21% in Q4. The price of oil had fallen to four-year lows in recent months, as OPEC had begun to restore its output aggressively. The strategy of OPEC is likely to cause a huge global oil surplus of about 2.0 million barrels per day this year. That said, WTI Crude and Brent Crude were both higher by a mid-double-digit percentage following the escalating conflict in the Middle East.

For the year, adjusted earnings-per-share of $7.29 was down from $10.05 in 2024. Earnings declined primarily due to lower crude oil prices, lower affiliate earnings, and unfavorable currency exchange. These were offset by higher margins on refined product sales, an increase in sales volumes, and lower severance charges. Revenue fell 4.6% to $184.4 billion.

The company returned a record $27.1 billion to shareholders, including $12.1 billion in buybacks, $12.8 billion in dividends, and $2.2 billion of Hess share purchases in early 2025. The board approved a 4% dividend increase to $1.78 per share.

Growth Prospects

Chevron is one of the largest publicly traded energy corporations in the world and stands to benefit tremendously from elevated prices of oil and gas.

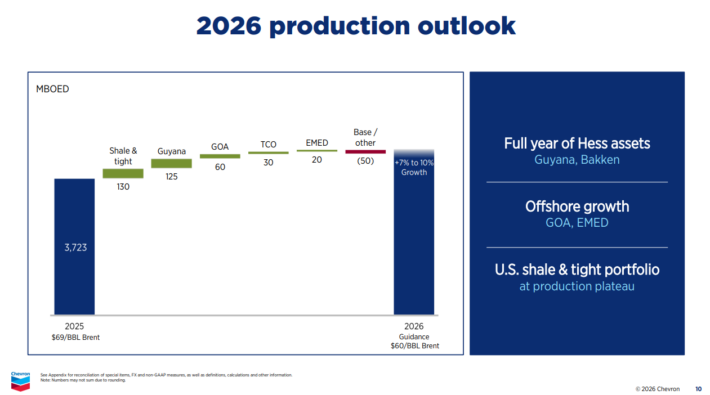

Chevron invested heavily in growth projects for years but failed to grow its output for an entire decade, as oil projects take several years to start bearing fruit. However, Chevron is now in the positive phase of its investing cycle.

Source: Investor Presentation

In addition, thanks to the high-grading of its asset portfolio, Chevron can fund its dividend even at an oil price of $40.

Another long-term growth catalyst is Chevron’s ability to make major acquisitions. On October 23rd, 2023, Chevron agreed to Acquire Hess (HES) for $53 billion in an all-stock deal. Thanks to this deal, Chevron will purchase the highly profitable Stabroek block in Guyana and Bakken assets, greatly enhancing its production and free cash flow.

Given the nearly all-time high earnings-per-share expected this year, we expect an 3% average annual increase over the next five years.

Competitive Advantages & Recession Performance

Chevron’s competitive advantage in the highly cyclical energy sector comes primarily from its size and financial strength. The company’s operational expertise allowed it to navigate the 2020 coronavirus pandemic successfully.

As a commodity producer, Chevron is vulnerable to any oil price downturn, particularly given that it is the most leveraged oil major to the oil price. However, thanks to its strong balance sheet, the company is likely to endure the next downturn, just like it has done in all the previous downturns.

Chevron’s aggressive cost-cutting efforts have helped the company become more efficient. Chevron has continued to reduce drilling costs, significantly reducing its break-even expense.

Chevron stacks up well among its peers in the energy sector. However, the company is certainly not the most recession-resistant Dividend Aristocrat, as evidenced by its performance during the 2007-2009 financial crisis:

- 2007 adjusted earnings-per-share: $8.77

- 2008 adjusted earnings-per-share: $11.67 (33% increase)

- 2009 adjusted earnings-per-share: $5.24 (-55% decline)

- 2010 adjusted earnings-per-share: $9.48 (81% increase)

Chevron’s adjusted earnings per share declined by more than 50% during the 2007-2009 financial crisis, but the company managed to remain profitable during a bear market that drove many of its competitors out of business.

This allowed Chevron to continue raising its dividend payment throughout the Great Recession. Chevron’s dividend safety is far above the average company in the energy sector.

Valuation & Expected Total Returns

Chevron’s expected total returns are more difficult to assess than those of many other companies. This is primarily due to the company’s highly volatile results, which result from the dramatic swings in oil and gas prices.

With a share price near $189, the price-to-earnings ratio presently sits 25.5 times based on 2026 expected earnings of $7.40 per share.

If the stock reverted to our fair value estimate of 14 times earnings, this would imply a sizeable valuation headwind over the next five years 11.3% annually.

In addition, the stock offers a 3.8% dividend yield. However, projected earnings growth of 3% and the dividend yield are likely to be offset by the expected headwind from multiple reversion.

Overall, the stock could generate a -3.7% average annual return over the next five years off its nearly all-time high current stock price.

Final Thoughts

Chevron is one of the rare oil and gas companies that was able to navigate through the Great Recession of 2007-2009, the oil downturn of 2014-2016, and the COVID-19 pandemic without cutting its dividend.

Chevron’s lower cost structure allows it to handle a much lower average oil price. Furthermore, new projects in the U.S. and international markets will help the company continue to grow.

Nevertheless, as we are nearing the peak of the oil industry’s cycle, which is infamous for its dramatic swings, Chevron is rated as a hold at current prices.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: