Updated on November 24th, 2025 by Bob Ciura

Grocery stocks are in an uncertain position. Industry trends are changing as more consumers gravitate toward online shopping and grocery delivery, which accelerated during the coronavirus pandemic.

Meanwhile, competition among grocery stocks is heating up. E-commerce giant Amazon.com (AMZN) made a huge entry into grocery with its ~$14 billion acquisition of Whole Foods.

Many of these grocery stocks remain attractive for dividend growth investors. For example, Walmart and Target are both members of the Dividend Aristocrats.

The Dividend Aristocrats are a group of 69 stocks in the S&P 500 Index with 25+ years of consecutive dividend increases.

The requirements to be a Dividend Aristocrat are:

- Be in the S&P 500

- Have 25+ consecutive years of dividend increases

- Meet certain minimum size & liquidity requirements

You can download an Excel spreadsheet of all 66 Dividend Aristocrats (with important financial metrics such as dividend yields and payout ratios) by clicking the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Meanwhile, Costco and Kroger are members of the Dividend Achievers list, a group of stocks with 10+ years of consecutive dividend growth.

You can see the entire list of all ~400 Dividend Achievers by clicking here.

These retailers are all making progress to better compete with Amazon, adapt to the changing consumer demands, and continue generating growth.

This article will discuss the top 7 grocery stocks ranked in order of expected total returns.

Table of Contents

We have ranked the top 7 grocery stocks according to expected returns. The grocery stocks are listed from lowest to highest five-year expected total returns.

You can use the following links to instantly jump to any specific stock:

- Best Grocery Stock #7: SpartanNash Co. (SPTN)

- Best Grocery Stock #6: Walmart Inc. (WMT)

- Best Grocery Stock #5: Kroger Co. (KR)

- Best Grocery Stock #4: Dollar General Corp. (DG)

- Best Grocery Stock #3: Costco Wholesale Corp. (COST)

- Best Grocery Stock #2: Target Corporation (TGT)

- Best Grocery Stock #1: Albertsons Corporation (ACI)

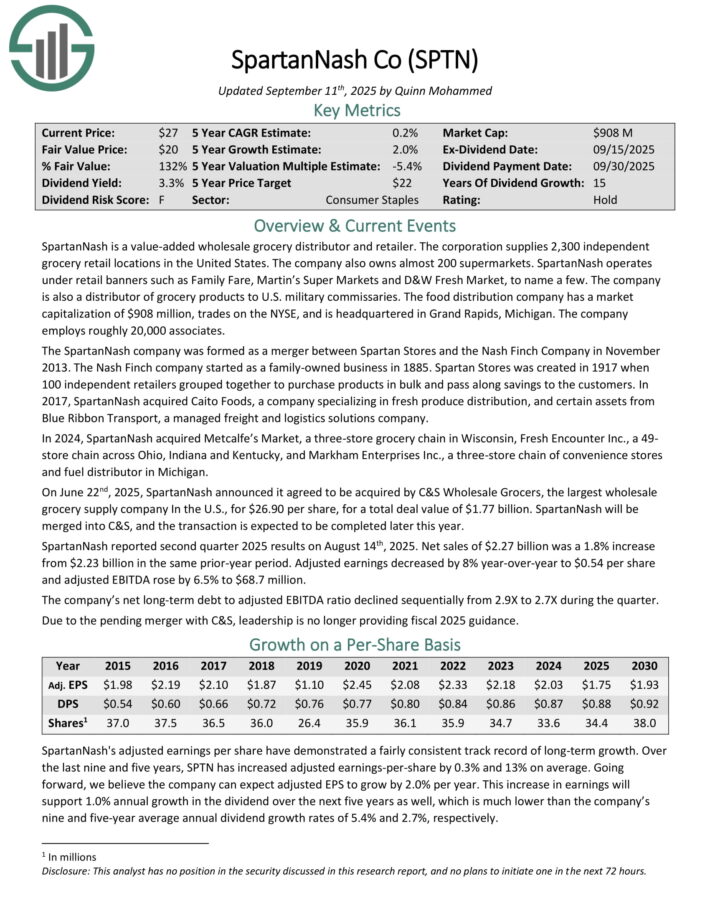

Best Grocery Stock #7: SpartanNash Co. (SPTN)

- 5-year expected annual returns: -0.2%

SpartanNash is a value-added wholesale grocery distributor and retailer. The corporation supplies 2,300 independent grocery retail locations in the United States. The company also owns almost 200 supermarkets.

SpartanNash operates under retail banners such as Family Fare, Martin’s Super Markets and D&W Fresh Market, to name a few. The company is also a distributor of grocery products to U.S. military commissaries.

On June 22nd, 2025, SpartanNash announced it agreed to be acquired by C&S Wholesale Grocers, the largest wholesale grocery supply company In the U.S., for $26.90 per share, for a total deal value of $1.77 billion. SpartanNash will be merged into C&S, and the transaction is expected to be completed later this year.

SpartanNash reported second quarter 2025 results on August 14th, 2025. Net sales of $2.27 billion was a 1.8% increase from $2.23 billion in the same prior-year period. Adjusted earnings decreased by 8% year-over-year to $0.54 per share and adjusted EBITDA rose by 6.5% to $68.7 million.

Click here to download our most recent Sure Analysis report on SpartanNash (preview of page 1 of 3 shown below):

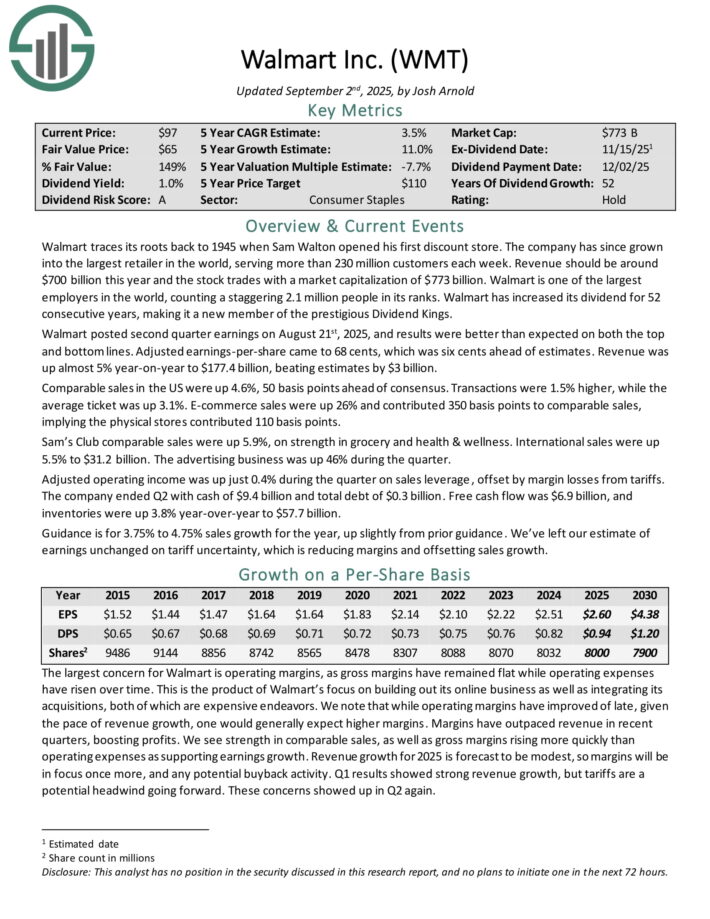

Best Grocery Stock #6: Walmart Inc. (WMT)

- 5-year expected annual returns: 1.8%

Walmart traces its roots back to 1945 when Sam Walton opened his first discount store. The company has since grown into the largest retailer in the world, serving more than 230 million customers each week. Revenue should be around $700 billion this year.

Walmart posted second quarter earnings on August 21st, 2025, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to 68 cents, which was six cents ahead of estimates. Revenue was up almost 5% year-on-year to $177.4 billion, beating estimates by $3 billion.

Comparable sales in the US were up 4.6%, 50 basis points ahead of consensus. Transactions were 1.5% higher, while the average ticket was up 3.1%.

E-commerce sales were up 26% and contributed 350 basis points to comparable sales, implying the physical stores contributed 110 basis points.

Sam’s Club comparable sales were up 5.9%, on strength in grocery and health & wellness. International sales were up 5.5% to $31.2 billion. The advertising business was up 46% during the quarter.

Adjusted operating income was up just 0.4% during the quarter on sales leverage, offset by margin losses from tariffs. The company ended Q2 with cash of $9.4 billion and total debt of $0.3 billion.

Guidance is for 3.75% to 4.75% sales growth for the year, up slightly from prior guidance.

Click here to download our most recent Sure Analysis report on WMT (preview of page 1 of 3 shown below):

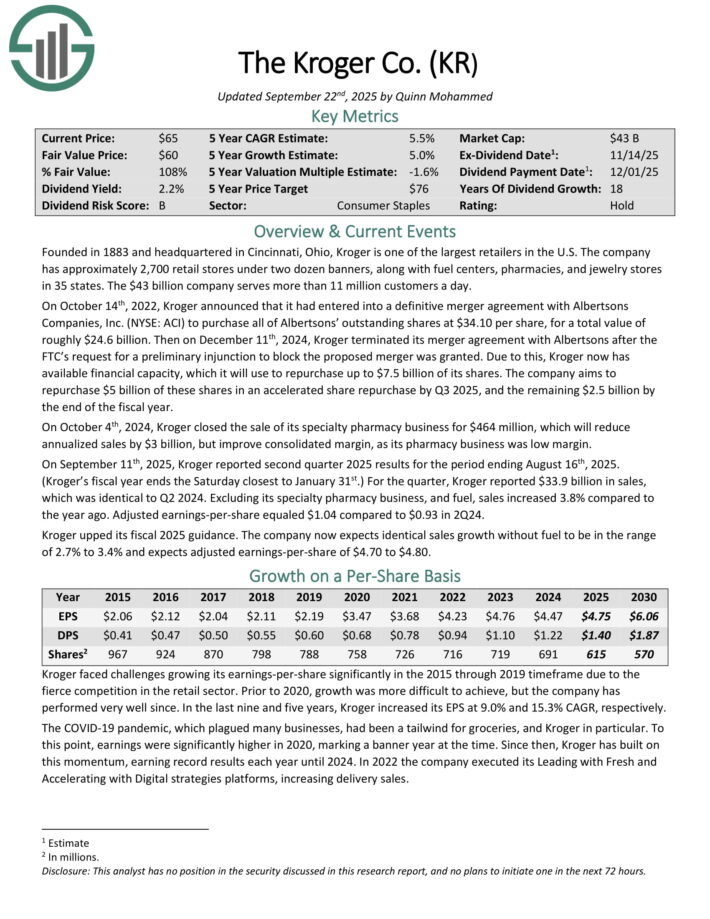

Best Grocery Stock #5: Kroger Co. (KR)

- 5-year expected annual returns: 5.1%

Kroger is one of the largest retailers in the U.S. The company has approximately 2,700 retail stores under two dozen banners, along with fuel centers, pharmacies, and jewelry stores in 35 states. The company serves more than 11 million customers a day.

On September 11th, 2025, Kroger reported second quarter 2025 results for the period ending August 16th, 2025 (Kroger’s fiscal year ends the Saturday closest to January 31st.)

For the quarter, Kroger reported $33.9 billion in sales, which was identical to Q2 2024. Excluding its specialty pharmacy business, and fuel, sales increased 3.8% compared to the year ago. Adjusted earnings-per-share equaled $1.04 compared to $0.93 in 2Q24.

Kroger has reduced its share count by 3.7% over the last decade. And now that the Albertson’s merger has been terminated, Kroger intends to repurchase $7.5 billion of its common stock, which will meaningfully reduce its share count and lead to higher EPS .

Click here to download our most recent Sure Analysis report on Kroger (preview of page 1 of 3 shown below):

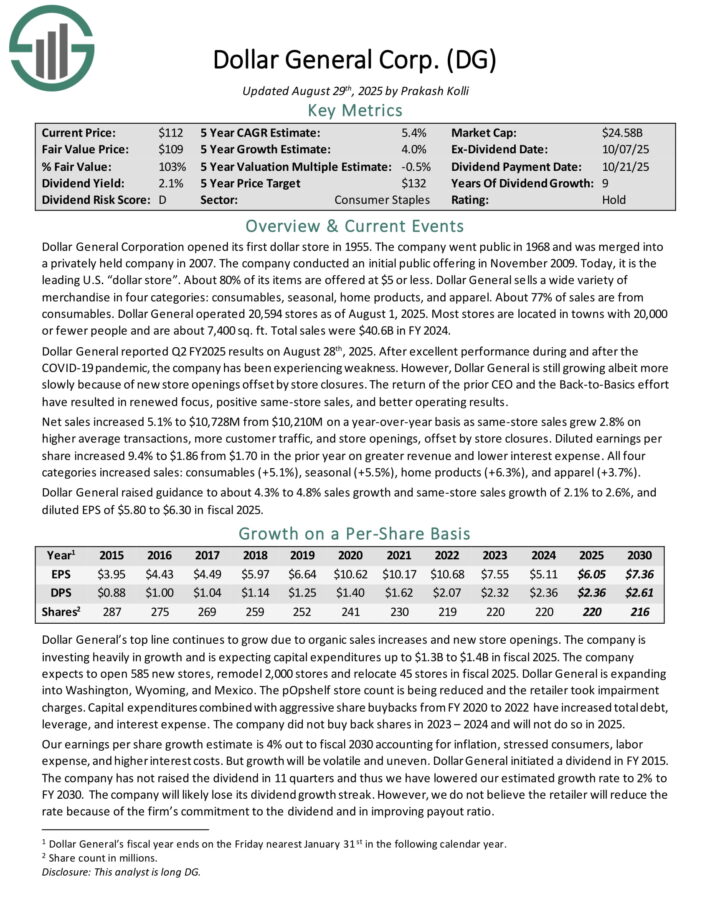

Best Grocery Stock #4: Dollar General Corp. (DG)

- 5-year expected annual returns: 7.3%

Dollar General Corporation opened its first dollar store in 1955. Today, it is the leading U.S. “dollar store”. About 80% of its items are offered at $5 or less.

Dollar General sells a wide variety of merchandise in four categories: consumables, seasonal, home products, and apparel. About 77% of sales are from consumables. Dollar General operated 20,594 stores as of August 1, 2025.

Most stores are located in towns with 20,000 or fewer people and are about 7,400 sq. ft. Total sales were $40.6B in FY 2024.

Dollar General reported Q2 FY2025 results on August 28th, 2025. Net sales increased 5.1% to $10,728M from $10,210M on a year-over-year basis as same-store sales grew 2.8% on higher average transactions, more customer traffic, and store openings, offset by store closures.

Diluted earnings per share increased 9.4% to $1.86 from $1.70 in the prior year on greater revenue and lower interest expense. All four categories increased sales: consumables (+5.1%), seasonal (+5.5%), home products (+6.3%), and apparel (+3.7%).

Dollar General raised guidance to about 4.3% to 4.8% sales growth and same-store sales growth of 2.1% to 2.6%, and diluted EPS of $5.80 to $6.30 in fiscal 2025.

Click here to download our most recent Sure Analysis report on DG (preview of page 1 of 3 shown below):

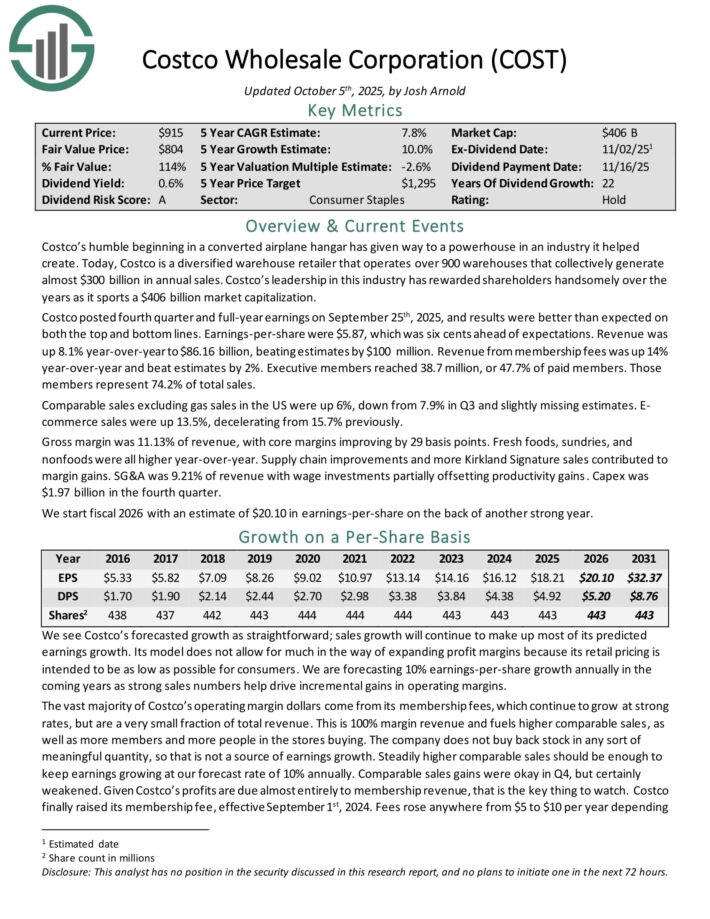

Best Grocery Stock #3: Costco Wholesale (COST)

- 5-year expected annual returns: 8.2%

Costco is a diversified warehouse retailer that operates over 900 warehouses that collectively generate almost $300 billion in annual sales.

Costco posted fourth quarter and full-year earnings on September 25th, 2025, and results were better than expected on both the top and bottom lines. Earnings-per-share were $5.87, which was six cents ahead of expectations.

Revenue was up 8.1% year-over-year to $86.16 billion, beating estimates by $100 million. Revenue from membership fees was up 14% year-over-year and beat estimates by 2%.

Executive members reached 38.7 million, or 47.7% of paid members. Those members represent 74.2% of total sales.

Comparable sales excluding gas sales in the US were up 6%, down from 7.9% in Q3 and slightly missing estimates. E-commerce sales were up 13.5%, decelerating from 15.7% previously.

The vast majority of Costco’s operating margin dollars come from its membership fees, which continue to grow at strong rates, but are a very small fraction of total revenue. This is 100% margin revenue and fuels higher comparable sales, as well as more members and more people in the stores buying.

The company does not buy back stock in any sort of meaningful quantity, so that is not a source of earnings growth. Steadily higher comparable sales should be enough to keep earnings growing at our forecast rate of 10% annually.

Click here to download our most recent Sure Analysis report on Costco (preview of page 1 of 3 shown below):

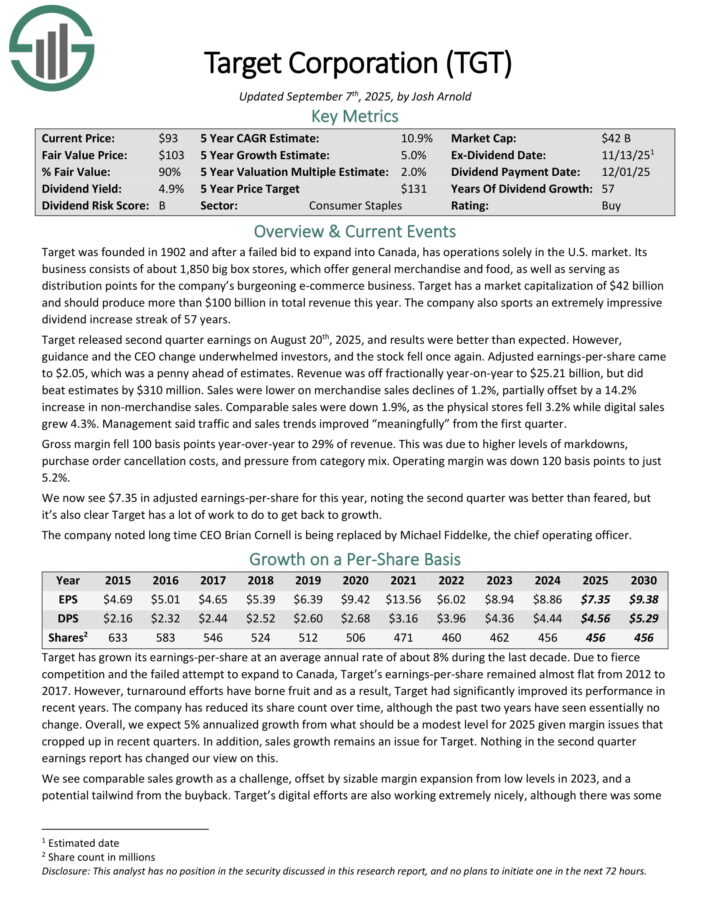

Best Grocery Stock #2: Target (TGT)

- 5-year expected annual returns: 12.3%

Target was founded in 1902 and now operates about 1,850 big box stores, which offer general merchandise and food, as well as serving as distribution points for the company’s e-commerce business.

Target released second quarter earnings on August 20th, 2025, and results were better than expected. However, guidance and the CEO change underwhelmed investors, and the stock fell once again.

Adjusted earnings-per-share came to $2.05, which was a penny ahead of estimates. Revenue was off fractionally year-on-year to $25.21 billion, but did beat estimates by $310 million. Sales were lower on merchandise sales declines of 1.2%, partially offset by a 14.2% increase in non-merchandise sales.

Comparable sales were down 1.9%, as the physical stores fell 3.2% while digital sales grew 4.3%. Management said traffic and sales trends improved “meaningfully” from the first quarter.

The company is investing heavily in its business in order to navigate through the changing landscape in the retail sector. The payout is now 62% of earnings for this year, which is elevated from historical levels, but the dividend remains well-covered.

Click here to download our most recent Sure Analysis report on TGT (preview of page 1 of 3 shown below):

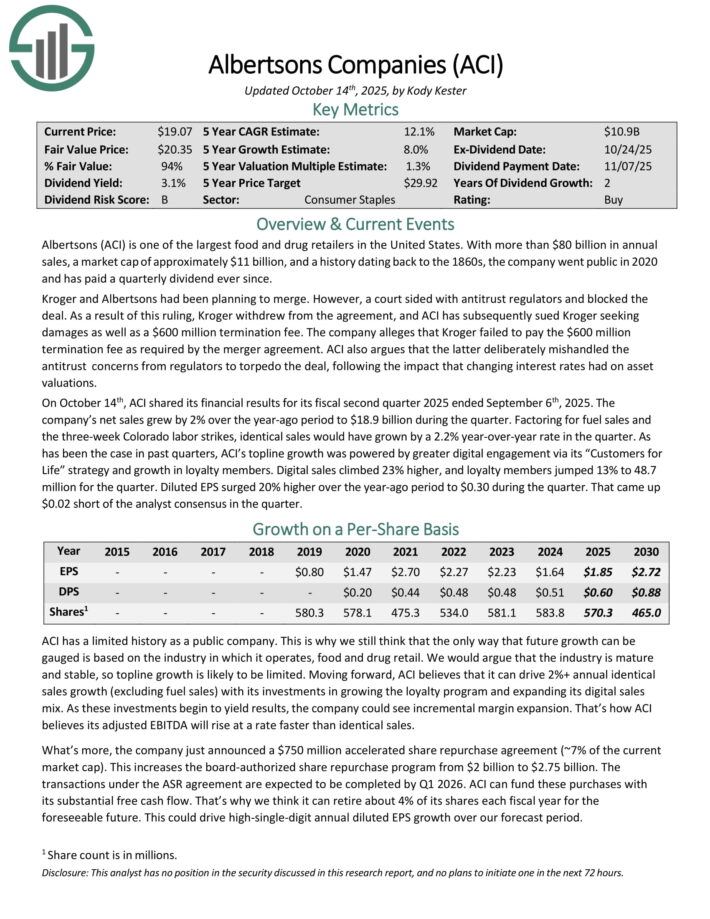

Best Grocery Stock #1: Albertsons Corporation (ACI)

- 5-year expected annual returns: 13.8%

Albertsons is one of the largest food and drug retailers in the United States. With more than $80 billion in annual

sales, and a history dating back to the 1860s, the company went public in 2020 and has paid a quarterly dividend ever since.

On October 14th, ACI shared its financial results for its fiscal second quarter 2025 ended September 6th, 2025. The company’s net sales grew by 2% over the year-ago period to $18.9 billion during the quarter.

Factoring for fuel sales and the three-week Colorado labor strikes, identical sales would have grown by a 2.2% year-over-year rate in the quarter.

As has been the case in past quarters, ACI’s topline growth was powered by greater digital engagement via its “Customers for Life” strategy and growth in loyalty members.

Digital sales climbed 23% higher, and loyalty members jumped 13% to 48.7 million for the quarter. Diluted EPS surged 20% higher over the year-ago period to $0.30 during the quarter.

Click here to download our most recent Sure Analysis report on Albertsons (preview of page 1 of 3 shown below):

Final Thoughts

The grocery industry is changing like never before. Now that Amazon has acquired Whole Foods, the company will likely accelerate its push into the grocery industry even further, especially with new technologies on the way.

That said, the top grocery stocks have decades of experience in the retail industry. They have proven the ability to navigate difficult conditions before and adapt when necessary.

Broadly speaking, the grocery industry is attractive for investors right now. Investors looking to buy grocery stocks should focus on those with durable competitive advantages and the financial strength to continue investing in growth.

Target and Walmart have the longest histories of annual dividend increases, while several others also have meaningful dividend growth histories.

Additional Resources

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

If that strategy appeals to you, it may be useful to browse through the following databases of dividend growth stocks:

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 56 stocks with 50+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: