Updated on May 20th, 2026 by Nathan Parsh

AGNC Investment Corp (AGNC) has an extremely high dividend yield of above 14%. In terms of current dividend yield, AGNC is near the very top of our list of high-yield dividend stocks.

In addition, AGNC pays its dividend each month rather than quarterly or semi-annually. Monthly dividends allow investors to compound dividends even faster.

There are 120 monthly dividend stocks in our database.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yields and payout ratios) by clicking on the link below:

That said, investors should also assess the sustainability of such a high dividend yield, as yields in excess of 10% are often a sign of fundamental business challenges.

Double-digit dividend yields often signal that investors do not believe the dividend is sustainable and are pricing the stock in anticipation of a cut to the dividend.

This article will discuss AGNC’s business model and whether the stock appeals to income-oriented investors.

Business Overview

AGNC was founded in 2008 and is an internally managed REIT. Unlike most REITs, which own physical properties that are leased to tenants, AGNC has a different business model. It operates in a niche of the REIT market: mortgage securities.

AGNC invests in agency mortgage-backed securities. It generates income by collecting interest on its invested assets, minus borrowing costs. It also records gains or losses from its investments and hedging practices.

Agency securities have principal and interest payments guaranteed by either a government-sponsored entity or the government itself. They theoretically carry less risk than private mortgages.

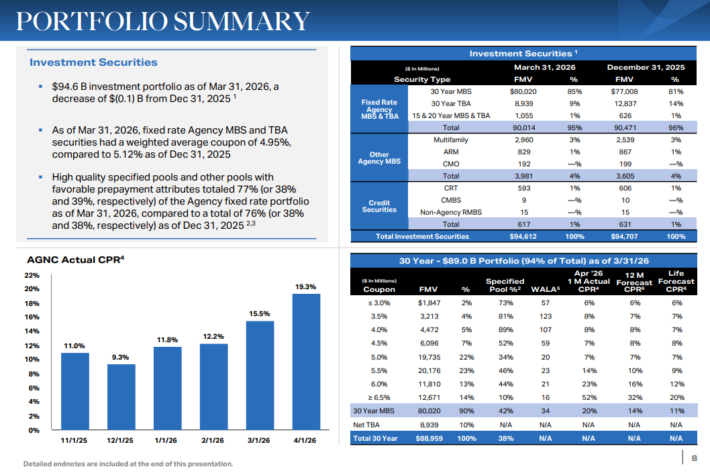

Source: Investor Presentation

The trust employs significant amounts of leverage to invest in these securities, boosting its ability to generate interest income. AGNC borrows primarily on a collateralized basis through securities structured as repurchase agreements.

The trust’s goal is to build value via monthly dividends and net asset value accretion. AGNC has done well with its dividends over time, but net asset value creation has sometimes proven elusive.

Indeed, the trust has paid nearly $50 of total dividends per share since its IPO; the share price today is just $10.15. In other words, the trust has distributed cash per-share to shareholders of nearly five times the stock’s current value.

That sort of track record is extraordinary and is why some investors are drawn to the stock.

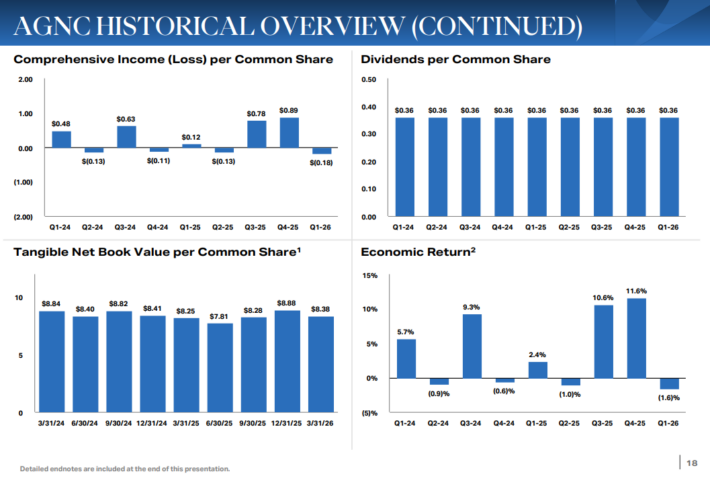

On April 20th, 2026, AGNC Investment Corp. reported its financial results for the first quarter of 2026. The company announced a comprehensive loss of $(0.18) per common share, which included a net loss of $(0.17) and $(0.01) in other comprehensive loss.

The tangible net book value per common share decreased by $0.50, or 5.6%, from the previous quarter, ending at $8.38 as of March 31, 2026. AGNC’s economic return was down 1.6% on tangible common equity for the quarter, comprising $0.36 in dividends declared and a $0.50 decline in tangible book value.

The company’s net spread and dollar roll income was $0.42 per share, which was a 4.5% decrease from $0.45 in Q1 2025, but was $0.05 better than expected. This decline reflected constant prepayment rate for the quarter, which nearly doubled to 13.2% from 7% a year ago.

The average asset yield stood at 4.95%, while the net interest spread was 2.06%. AGNC maintained a leverage ratio of 7.4x tangible net book value and held $7.0 billion in unencumbered cash and Agency MBS.

Growth Prospects

The major drawback to mortgage REITs is that rising interest rates negatively impact the business model. AGNC makes money by borrowing at short-term rates, lending at long-term rates, and pocketing the difference. Mortgage REITs are also highly leveraged to amplify returns.

It is common for mortgage REITs to have leverage rates of 5x or more because spreads on these securities tend to be quite tight. AGNC currently has a leverage ratio of 7.4x.

In a rising interest-rate environment, mortgage REITs typically see the value of their investments reduced. Higher rates usually cause their interest margins to contract, as the payment received is fixed in most cases, whereas borrowing costs are variable.

In previous years, interest rates surged to 23-year highs as central banks around the world hiked rates aggressively to reduce inflation. The trust’s book value contracted in those quarters as a result of these moves.

Overall, the high payout ratio and the volatile nature of the business model will harm earnings-per-share growth. In fact, we believe that EPS will have a -1.0% growth rate annually through 2031. We also believe that dividend growth will be anemic for the foreseeable future.

While rates have been cut recently, we do not believe that they will drastically cut absent a global recession.

Additionally, inflation has ticked up in the U.S. Previously, the Fed had expected to reduce further to as low as 2.75%-3.0% by 2026. But inflation starting to rebound, the Fed may not be able to execute as per its guidance.

In that case, AGNC could see a headwind to its business, as its borrowing costs will increase and its interest margins will contract if rates remain the same or are moved higher.

Dividend & Valuation Analysis

AGNC has declared monthly dividends of $0.12 per share since April 2020. This means that AGNC has an annualized payout of $1.44 per share, which equals an extremely high current yield of 14.2% based on the current share price.

Source: Investor Presentation

High yields can be a sign of elevated risk. AGNC’s dividend does carry significant risk. AGNC has reduced its dividend several times over the past decade.

We do not see a dividend cut as an imminent risk at this point, given that the payout was cut fairly recently to account for unfavorable interest rate movements and that AGNC’s net asset value has stabilized somewhat.

Management has taken the necessary steps to protect its interest income, so we don’t see another dividend cut in the near term, particularly if the Fed doesn’t raise rates or is able to cut as it had previously planned to do.

The payout ratio is expected to be ~91% of earnings for 2026, which would be down from 96% last year. If this proves correct, there will be no reason to cut the payout. It should be noted that the REITs payout ratio has been in the mid-40% to mid-70% range for the 2021-2024 period, so it is possible for AGNC to have a very healthy payout ratio.

However, with any mortgage REIT, there is always a significant risk to the payout, and investors should keep that in mind, particularly given the volatile behavior of interest rates in recent years.

Shares of AGNC are trading at 6.4x our expected EPS for the year, which is above our target price-to-earnings ratio of 5.0. Reverting to our target P/E by 2031 would reduce annual returns by 4.9% over this period.

Combined with the 14.2% starting yield and our expectation for -1.0% earnings growth, we forecast that AGNC could have annual return potential of 7.7% through 2031.

Final Thoughts

High-yield monthly dividend-paying stocks are extremely attractive for income investors, at least on the surface. This is particularly true in an environment of low interest rates, as alternative sources of income generally have much lower yields.

AGNC pays a hefty yield of 14.2% right now, which is very high by any standard.

We believe the REIT’s high yield is safe for the foreseeable future, but given the company’s business model and interest-rate sensitivity, this is hardly a low-risk situation.

While AGNC should continue to pay a dividend yield many times higher than the S&P 500 Index average, it is not an attractive option for risk-averse income investors.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 5%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more