Updated on April 23rd, 2026 by Felix Martinez

SmartCentres Real Estate Investment Trust (CWYUF) has three appealing investment characteristics:

#1: It is a REIT, so it has a favorable tax structure and pays out the majority of its earnings as dividends.

Related: List of publicly traded REITs

#2: It is a high-yield stock based on its 7.3% dividend yield.

Related: List of 5%+ yielding stocks

#3: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

There are currently just 119 monthly dividend stocks. You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

SmartCentres Real Estate Investment Trust’s trifecta of favorable tax status as a REIT, a high dividend yield, and a monthly dividend makes it appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about SmartCentres Real Estate Investment Trust.

Business Overview

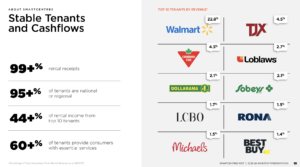

SmartCentres Real Estate Investment Trust is one of the largest fully integrated REITs in Canada. Its best-in-class portfolio consists of 195 strategically located properties in every province across the country. SmartCentres REIT has $12.1 billion in assets and owns 35.6 million square feet of income-producing, value-oriented retail space with 98.6% occupancy on owned land across Canada.

Source: Investor Presentation

SmartCentres REIT faces a secular headwind, namely, consumers’ shift from traditional shopping to online purchases. This trend has remarkably accelerated since the onset of the coronavirus crisis, hurting many retail REITs.

However, SmartCentres REIT enjoys a key competitive advantage, namely the strong financial position of its tenants. The REIT generates more than 25% of its revenue from Walmart and more than 60% from financially strong tenants that offer essential services. This is a major competitive advantage, as it makes the REIT’s cash flows reliable and resilient to economic downturns.

The company reported fourth-quarter 2025 net rental income of $143.6 million, representing a 1.4% increase year over year. Funds from operations (FFO) per unit rose slightly to $0.54 from $0.53 in the prior year, reflecting improved leasing activity and higher net operating income, although net income declined due to unfavorable fair value adjustments. Same-property NOI grew 2.9% in the quarter, supported by strong occupancy of 98.6% and continued rent growth on lease renewals.

Growth Prospects

SmartCentres REIT can boast a defensive business model, thanks to its tenants’ high credit profiles. On the other hand, REITs have failed to grow their FFO per unit over the last decade, as their bottom line has remained essentially flat.

It is important to note that the lackluster performance record has resulted primarily from strengthening the USD vs. CAD. As the Canadian dollar has depreciated by about 30% over the last decade, it is clear that SmartCentres REIT has grown its average FFO per unit by about 2.7% per year in local currency.

Source: Investor Presentation

Given SmartCentres REIT’s promising growth prospects, but also its lackluster performance record, currency risk, and interest-rate headwinds, we expect the REIT to grow its FFO per unit by about 0.5% per year on average over the next five years.

Source: Investor Presentation

Dividend & Valuation Analysis

SmartCentres REIT is currently offering an above-average dividend yield of 6.7%. It is thus an interesting candidate for income-oriented investors, but they should be aware that the dividend may fluctuate significantly over time due to exchange-rate gyrations between the Canadian dollar and the USD.

Moreover, the REIT has an elevated payout ratio of nearly 96%, significantly reducing the dividend’s safety margin. On the bright side, thanks to its defensive business model and strong interest coverage ratio, the trust is not likely to cut its dividend in the absence of a severe recession. Nevertheless, investors should not expect meaningful dividend growth going forward. They should know that the dividend may be cut during an unforeseen downturn, such as a deep recession. We also note that SmartCentres REIT has a material debt load on its balance sheet.

In reference to the valuation, SmartCentres REIT has traded for 14.3 times its FFO per unit in the last 12 months. Given the REIT’s material debt load, we assume a fair price-to-FFO ratio of 13.0 for the stock. Therefore, the current FFO multiple exceeds our assumed fair price-to-FFO ratio. If the stock trades at its fair value in five years, it will incur a -1.9% annualized drag on its returns.

Taking into account the 0.5% annual FFO-per-unit growth, the 6.7% dividend, and a -1.9% annualized contraction of valuation level, SmartCentres REIT could offer a 4.8% average annual total return over the next five years. This is a poor expected return, though we recommend waiting for a better entry point to enhance the margin of safety and the expected return. Moreover, the stock is suitable only for investors comfortable with the risks associated with the high payout ratio and the trust’s material debt load.

Final Thoughts

SmartCentres REIT can generate most of its revenues from companies with rock-solid balance sheets. It thus enjoys much more reliable revenues than most REITs. This is an important competitive advantage, especially during economic downturns.

Despite its high payout ratio, the stock offers an exceptionally high dividend yield of 6.7%, making it an attractive candidate for income-oriented investors’ portfolios.

On the other hand, investors should be aware of the risk that results from the REIT’s somewhat weak balance sheet. If high inflation persists for much longer than currently anticipated, high interest rates will place a heavy burden on the REIT. Therefore, only investors who are confident that inflation will soon revert to normal levels should consider purchasing this stock.

Moreover, SmartCentres REIT is characterized by extremely low trading volume. This means that it is hard to establish or sell a large position in this stock.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more