Updated on April 24th, 2026 by Josh Arnold

Real estate and dividend stocks are two of the most popular vehicles for creating passive retirement income.

The downside to owning rental properties is that it is not really passive. Any landlord who has had to call a plumber or an electrician during the middle of the night can attest to this.

Real estate investment trusts—or REITs—are very attractive investment vehicles for investors looking to capture the returns of the real estate sector while benefiting from the hands-off approach of dividend stocks.

EPR Properties (EPR) is one of the most well-known REITs. In the second half of 2021, EPR reinstated its monthly dividend after suspending it for over a year due to the coronavirus pandemic.

That means EPR rejoined the list of monthly dividend stocks. We’ve compiled a list of 119 monthly dividend stocks, along with important financial metrics like dividend yields and payout ratios, which you can view by clicking on the link below:

This article will analyze the investment prospects of EPR Properties in detail.

Business Overview

EPR Properties is a triple net lease real estate investment trust focusing on entertainment, recreation, and education properties.

A triple net lease means that the tenant is responsible for paying the three main costs associated with real estate: taxes, insurance, and maintenance. Operating as a triple net lease REIT reduces EPR Properties’ operating expenses, and increases the predictability of earnings.

EPR has identified entertainment, recreation, and education as the three large buckets it invests in. It has then identified attractive sub-segments of those larger segments, including movie theaters, ski resorts, and charter schools.

Source: Investor Presentation

EPR is focused in various metropolitan areas throughout the US and parts of Canada, so it is highly diversified geographically as well as with its tenants. It also practices constant capital recycling, divesting less attractive assets in favor of more attractive ones. This active approach is something that sets EPR apart from some other REITs.

EPR posted fourth quarter and full-year earnings on February 26th, 2026, and results were slightly better than expected. Funds-from-operations per-share came to $1.30, which met expectations. Revenue was up just over 3% year-over-year to $183 million, beating estimates by $1 million. Rental revenue rose $8 million year-over-year.

For the full year, FFO-per-share was $5.12, which was up nicely from $4.87 the year before. Disposition proceeds came to $35 million for Q4 and $168 million for the year. The company also announced that it was acquiring seven regional amusement parks from Six Flags for $342 million. This is the trust’s largest acquisition since 2017, but shares sold off heavily on the news.

Separately, the dividend was boosted by 5% to $3.72 per share annually, its fifth consecutive increase. We’re expecting $5.35 in adjusted FFO-per-share for 2026, but note the Six Flags parks acquisition is a significant wildcard for the coming quarters.

Growth Prospects

Prior to 2020, EPR had maintained a track record of steady growth. From 2010 to 2019, EPR compounded its adjusted FFO-per-share by almost 8% per year. The coronavirus pandemic upended virtually all REITs and caused EPR’s FFO-per-share to decline from $5.44 in 2019 to $1.43 in 2020.

Although the trust faced major challenges during the pandemic, which showed in its financial results, EPR continues to recover strongly. EPR still has many opportunities to drive its growth. The company’s focus on experiential properties protects it against e-commerce threats. EPR believes that consumers will still want these experiences, and thus, its properties will generate strong traffic.

The trust believes there’s strong future growth potential in location-based entertainment and several underpenetrated experiential segments in experiential real estate. Management believes there is a $100 billion+ addressable market opportunity there.

EPR has significantly reduced its education portfolio while growing most of its property types in its experiential portfolio. EPR will focus on growing all property types in its experiential portfolio, except for theatres. The trust wants to reduce its dependence on theatres given the significant volatility in results from that segment.

Source: Investor Presentation

We expect 5% annual FFO-per-share growth over the next five years. EPR’s growth will be fueled by its competitive advantages, primarily its portfolio of specialized properties. Through years of experience, EPR has methodically identified the most profitable properties and focused its investments in these areas. We do question the amusement park acquisition, but note that EPR’s management has proven to be strong operators over the years.

Competitive Advantage & Recession Performance

The company’s focus on experiential properties gives it a competitive advantage by protecting it against e-commerce threats. EPR believes that its properties will generate strong traffic, as consumers will still want those experiences. We also believe the management team’s willingness to pivot when conditions require it is a highly attractive trait.

The company certainly isn’t immune to recessions, but due to its business model and advantages, we see EPR as one of the better-run REITs in our coverage universe. A return to growth should allow the company to raise the dividend gradually over time.

Dividend Analysis

EPR’s dividend history was impressive heading into 2020. The company increased its annual per-share dividend by roughly 6% per year from 2010 to 2019. Of course, the pandemic forced the company to suspend its dividend for most of 2020.

Fortunately, EPR management expects its recovery to continue. This expectation gave management confidence to increase the monthly dividend for the fifth consecutive time, and it’s currently good for a 6.7% annual yield.

On an annualized basis, the $3.72 per share dividend is still below the pre-COVID payout of $4.59 per share. Still, at this level, EPR stock yields 6.7%. Therefore, EPR stock is still attractive for income investors as a high dividend stock.

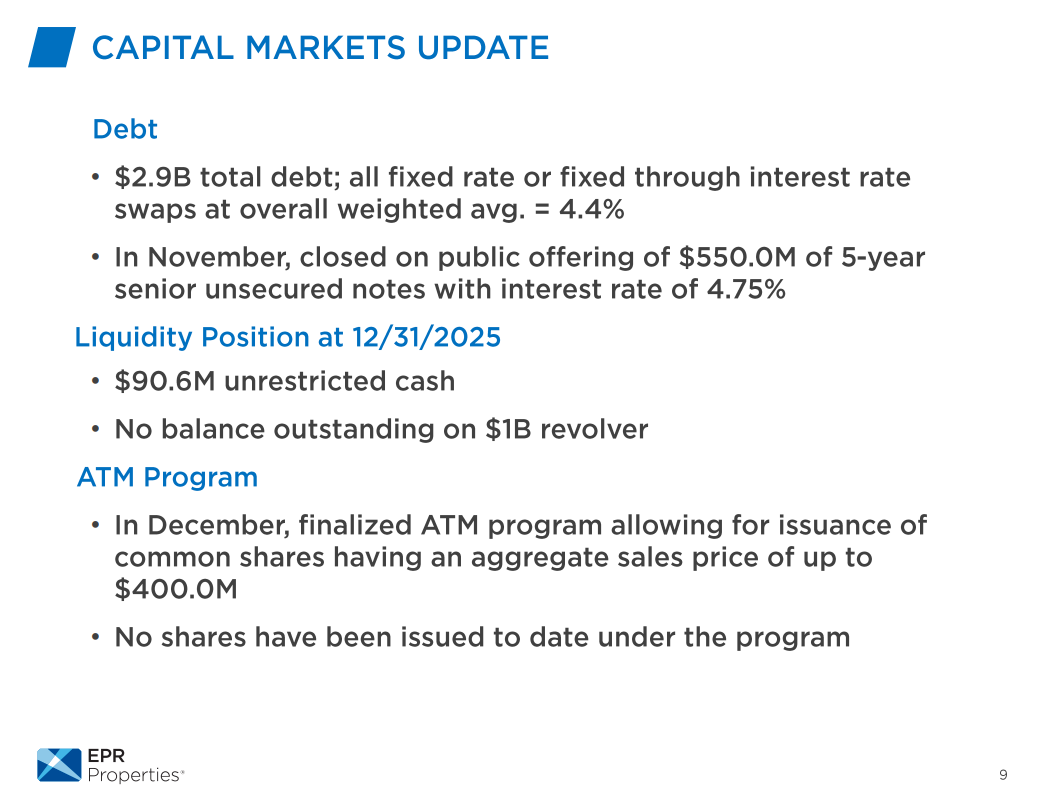

EPR has a reasonably leveraged capital structure that affords it some flexibility. It has worked to repair its balance sheet in the wake of the pandemic to improve its dividend safety and growth potential further.

Source: Investor Presentation

EPR’s debt totals about $2.9 billion, with a weighted average debt maturity of 3 years and a weighted average interest rate of 4.4%. It has a $1 billion credit revolver that has a zero balance, giving EPR plenty of liquidity.

All of this supports EPR’s growth plans and, by extension, its ability to not only pay its dividend but also, hopefully raise it over time.

EPR’s dividend appears to be secure, and the trust will likely continue to raise it at meaningful rates over time if its FFO continues to recover back to pre-COVID levels. This makes the stock attractive for those seeking current income and dividend growth.

Final Thoughts

EPR Properties looks to be performing very well following the pandemic and continues to recover strongly into 2026. The REIT has a dominant position in the ownership of movie theaters, recreational facilities, and educational properties, although as usual, its portfolio is under construction. These are relatively small subsegments of the real estate industry, which gives EPR the advantage of being a ‘big fish in a small pond.’

EPR Properties stock has a 6.7% dividend yield and has its monthly dividend payments for five years. As a result, it is once again an appealing stock for income investors looking for high yields and monthly payouts.

Of course, this depends on the continued recovery in EPR’s portfolio metrics and financial results. Based on all these factors, EPR Properties appears to be a good choice for income investors or investors looking for some exposure to high-yield REITs.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more