Updated on April 20th, 2026 by Nathan Parsh

Real Estate Investment Trusts have much to offer investors who desire higher investment income, including retirees. For instance, Gladstone Commercial Corporation (GOOD) is a REIT with a high dividend yield of 9.4%.

You can see the full list of 5%+ yielding stocks by clicking here.

Gladstone Commercial appears to be an attractive dividend stock, especially considering the available alternatives. The S&P 500 Index, on average, has about a ~1.2% dividend yield. Plus, Gladstone Commercial pays its dividends each month.

You can download our full Excel spreadsheet of all 119 monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

However, Gladstone Commercial’s dividend is far from guaranteed. Its expected payout ratio for this year is 84%, leaving little room for error in maintaining the dividend.

This article will discuss the trust’s business model and financial performance and explain why its dividend may be riskier than it first appears.

Business Overview

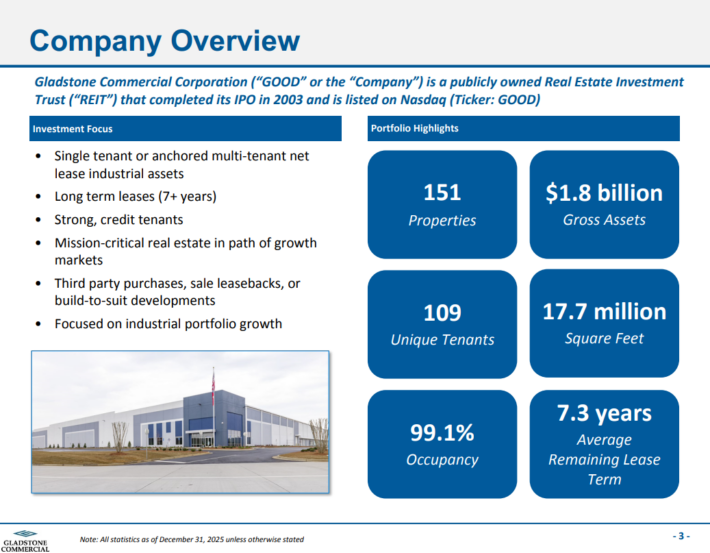

Gladstone Commercial is a Real Estate Investment Trust, or REIT, that invests primarily in single-tenant and anchored multi-tenant net leased assets. It owns nearly 18 million square feet of office and industrial real estate in the U.S.

Gladstone Commercial has a very diversified portfolio. As of the end of March 2026, the trust’s portfolio consisted of 151 properties leased to more than 109 unique tenants in 27 states.

Source: Investor presentation

The trust’s portfolio is typically geared toward long-term agreements. In addition, Gladstone Commercial enjoys high occupancy rates, including a current rate of 99.1%. Impressively, occupancy has never fallen below 95% since the trust’s IPO in 2003.

Approximately 53% of Gladstone Commercial’s tenants are rated investment grade or are the non-rated investment grade equivalent. This contributes to a high-quality portfolio of tenants that should weather minor economic downturns and preserve Gladstone Commercial’s rent streams.

Gladstone reported fourth-quarter and full-year earnings results on February 18th, 2026. Results were better than expected on both the top and bottom lines. Funds-from-operations per-share came to $0.37 Q4, which was $0.01 better than expected. Revenue was $43.46 million, which was $2.23 million ahead of estimates. Same-store lease revenue grew 4% in the 12 months ending in December compared to the same period a year earlier. Operating revenue for the quarter was $43.5 million, while operating expenses were $26.4 million.

Net assets increased during the year from $1.1 billion to $1.2 billion. Management reported that during 2025 Gladstone acquired $206 million of industrial assets across 10 facilities totaling 1.6 million square feet. These deals carried a weighted average cap rate of 8.88% and an average lease term of 15.9 years. The trust saw 100% collection of cash based rents, and occupancy was more than 99% across its portfolio. The average remaining lease being 7.3 years.

We project that Gladstone will generate FFO-per-share of $1.43 for the year, which would be just a 2.1% improvement from 2025.

Growth Prospects

The trust has generated impressive revenue growth in the past, but bottom-line growth has leveled off lately. This creates some uncertainty regarding the distribution’s safety. FY2026 core FFO expectations are essentially flat.

Gladstone’s FFO-per-share has been between $1.40 and $1.60 for most of the past decade as the trust continues to issue new shares and debt to fund acquisitions. Still, those acquisitions have failed to provide an economic gain for shareholders after accounting for share issuance and cost of debt. In other words, while the trust’s new properties provide growth on a dollar basis, when the cost of those acquisitions is factored in, it is essentially no gain on a per-share basis. Therefore, we expect that the trust will produce no annual growth in FFO-per-share over the next five years.

Given where the distribution is today, that could present a problem as the trust’s payout ratio is approaching 100%. However, despite the favorable fundamentals of the trust’s portfolio, its headwinds to earnings growth (dilution and operating expenses) are still very much present.

Still, the trust has successfully grown its asset base at a double-digit annual compound growth rate in the last decade. And since 2003, the portfolio has maintained high occupancy exceeding 95%.

With limited lease expirations in 2026, the trust is focused on growth. They are interested in increasing the portfolio’s industrial allocation. Currently, industrial properties account for roughly two-thirds of the portfolio. Office properties make up most of the remainder, with retail and medical offices rounding it out.

Dividend & Valuation Analysis

Gladstone Commercial’s current monthly dividend payment is $0.10 per share. On an annualized basis, the dividend payment is $1.20 per share, which is good for a high 9.4% dividend yield.

The distribution has been stagnant at $0.125 per share monthly since January 2008, reflecting the trust’s struggles with growth. However, recently, the trust decided to cut the dividend, reducing the monthly payment to $0.10 per share in January 2023.

To its credit, Gladstone Commercial has paid monthly dividends for more than 20 consecutive years, an impressive track record of consistent payouts.

Since Gladstone Commercial’s 2003 initial public offering, the trust has not missed a distribution or reduced it until recently, which is still pretty impressive for a REIT given the wide array of economic conditions that have existed in this time frame.

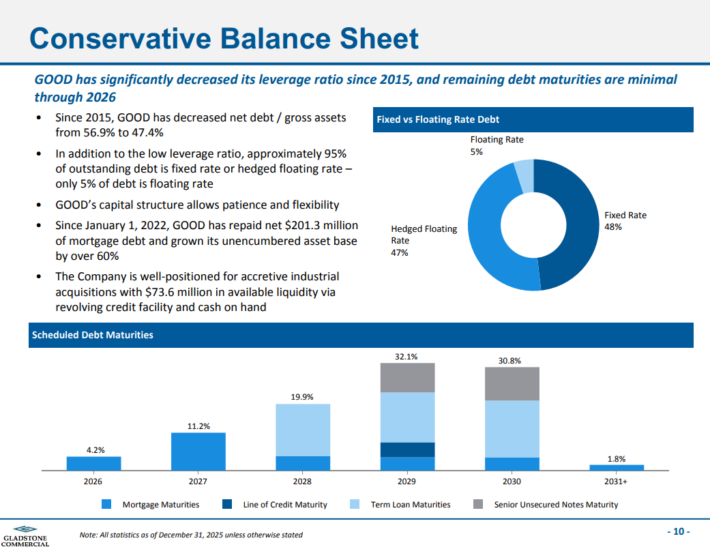

Another important consideration when buying dividend stocks is balance sheet strength.

Too much debt can jeopardize a trust’s dividends. On a positive note, Gladstone Commercial has worked to reduce its leverage significantly over the past several years and now has a balanced maturity schedule. Furthermore, its reduced dividend payout level will further ease the burden on its balance sheet.

Source: Investor Presentation

Approximately 95% of Gladstone Commercial’s debt is either fixed-rate or hedged, which could help mitigate the impact of volatile interest rates.

In addition, significant maturities are several years away, meaning the trust has time to generate cash to pay them off or find better ways to refinance them.

If the trust’s fundamentals deteriorate over the next few years, there is a chance it may not be able to sustain its dividend, even at the reduced current level. We see this as the principal risk of owning Gladstone Commercial today.

Shares of Gladstone Commercial are trading at 8.9 times our expected FFO-per-share for the year, which is below our target of 11 times FFO-per-share. Reverting to our target valuation by 2031 would result in an annual tailwind of 4.3% from multiple expansion over this period.

Combined with the 9.4% dividend yield, we project total returns of 11.2% per year through 2031.

Final Thoughts

Gladstone Commercial’s very high dividend yield is attractive and appears to be sustainable, at least in the near term, given the trust’s current level of FFO. The trust also enjoys high occupancy and strong rental rates.

As a result, investors will need to monitor the trust’s results closely to ensure FFO does not decline much from present levels. Indeed, even a modest decline could jeopardize the dividend.

Gladstone’s yield is attractive to income investors, but there appears to be little in the way of earnings growth. The monthly payment schedule is a bonus with the high yield, but investors must pay attention to results and monitor the payout ratio.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more