Updated on May 8th, 2026 by Felix Martinez

H&R Real Estate Investment Trust (HRUFF) has three appealing investment characteristics:

#1: It is a REIT, so it has a favorable tax structure and pays out the majority of its earnings as dividends.

Related: List of publicly traded REITs

#2: It offers an above-average dividend yield of 6.2%, nearly eight times the 1.5% yield of the S&P 500.

#3: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

H&R Real Estate Investment Trust’s trifecta of favorable tax status as a REIT, an above-average dividend yield, and a monthly dividend makes it appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about H&R Real Estate Investment Trust.

Business Overview

H&R REIT is one of the largest real estate investment trusts in Canada, with total assets of approximately $6.6 billion. It owns a portfolio of high-quality office, retail, industrial, and residential properties in North America, with a total leasable area of more than 26 million square feet.

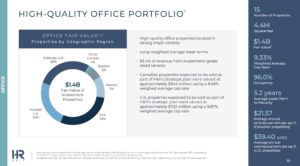

H&R REIT is undergoing a major transformation. It is divesting its grocery-anchored and essential service retail properties and office properties to focus exclusively on residential and industrial properties.

Source: Investor Presentation

The REIT aims to become a high-growth platform for residential and industrial properties. Management expects the asset portfolio to consist of approximately 80% residential and 20% industrial properties by the end of 2026.

H&R REIT has some attractive characteristics for prospective investors. Its management owns a significant stake in the company, and hence, its interests are aligned with those of the unitholders.

Source: Investor Presentation

The company reported mixed 2025 results as it continued repositioning its portfolio toward residential and industrial properties. Since 2021, the company has sold or agreed to sell roughly $7.0 billion in assets, significantly reducing its exposure to office and retail real estate. Residential and industrial assets now represent 84% of the portfolio.

For 2025, H&R reported a net loss of $791.6 million, largely due to declines in property valuations, particularly in office and New York residential assets. Net asset value per unit fell to $16.09 from $20.92 in 2024.

Despite these losses, operating fundamentals remained stable. Rental revenue totaled $815.1 million, while same-property NOI increased 1.6% year over year. Funds from operations (FFO) rose to $1.21 per unit, and adjusted funds from operations (AFFO) increased to $1.00 per unit.

The REIT also improved its financial position by reducing debt to approximately $3.5 billion and strengthening liquidity through major asset sales completed in early 2026. H&R maintained its annualized distribution rate of $0.60 per unit, with the AFFO payout ratio improving to 60.3% from 75.5% in 2024.

Growth Prospects

H&R REIT has exhibited a volatile performance record, partly due to fluctuations in the exchange rate between the Canadian dollar and the USD. In USD, FFO had declined 5.3% annually over the last decade.

That said, the REIT has a promising pipeline of growth projects in Austin, Dallas, Miami, and Tampa. These areas are characterized by superior population and economic growth when compared to the rest of the country. Given ample room for new properties in these markets, H&R REIT is likely to continue to grow its FFO per unit significantly for many years to come.

On the other hand, like most REITs, H&R REIT is currently facing headwinds from the adverse environment of high interest rates, which are likely to increase the trust’s interest expense burden.

Nevertheless, it is difficult to estimate the impact of high interest rates on H&R REIT, as the trust’s interest expense has decreased sharply in recent quarters due to extensive property divestments. In addition, investors should exercise caution in their growth expectations, given the extensive divestment of properties during the REIT’s ongoing transformation. Overall, we expect the FFO growth to remain flat over the next five years.

Dividend & Valuation Analysis

H&R REIT is currently offering a 5.6% dividend yield. It is thus an interesting candidate for income-oriented investors. Still, the latter should be aware that the dividend may fluctuate significantly over time due to exchange rate movements between the Canadian dollar and the USD.

Notably, the REIT has a payout ratio of only 63% for the current year, one of the lowest in the REIT universe. Given its solid business model and healthy interest coverage of approximately 4, the REIT can easily cover its dividend. To cut a long story short, investors can secure a dividend yield of 5.6% or more and rest assured that the dividend has a wide margin of safety.

Taking into account the stable FFO-per-unit growth, the 5.6% dividend, and a 8.7% annualized compression in the valuation level, H&R REIT could offer just -1.7% average annual total return over the next five years. This is not an attractive expected return, especially for investors who prioritize total returns. We note that the stock is suitable only for patient investors comfortable with the risks associated with the trust’s ongoing transformation.

Final Thoughts

H&R REIT has a solid business model, primarily driven by strong demand for its properties in the markets it serves. The stock offers an attractive dividend yield accompanied by a very low payout ratio, making it a suitable candidate for the portfolios of income-oriented investors.

On the other hand, investors should be aware of the risk associated with the REIT’s somewhat weak balance sheet and its ongoing transformation, which may lead to some volatility in the REIT’s results going forward. Moreover, H&R REIT is characterized by exceptionally low trading volume. Therefore, we rate H&R REIT shares a sell.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

-

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more