Updated on April 8th, 2026 by Nathan Parsh

Business Development Companies – or BDCs, for short – can be a great source of current yield for income investors.

Main Street Capital Corporation (MAIN) is a great example of this. MAIN stock has a current dividend yield of 5.8%, but the yield grows to 8% when factoring in the company’s special dividends.

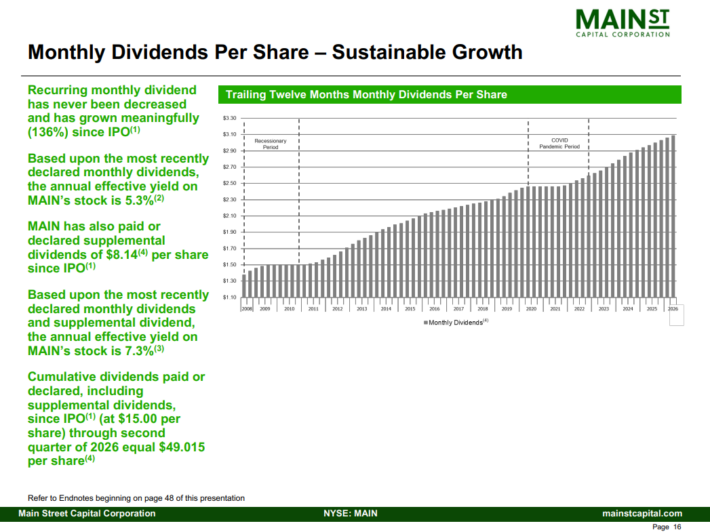

Better yet, Main Street Capital stock pays monthly dividends.

You can download our full Excel spreadsheet of all 119 monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

The stock’s high dividend yield and monthly payments make it a solid choice for income investors.

Main Street Capital’s business appears to be on solid footing. This article will discuss the investment prospects of Main Street Capital Corporation in detail.

Business Overview

Main Street Capital Corporation is a Business Development Company (BDC). Our full list is here.

The company operates as a debt and equity investor for lower middle market companies (those with $10-$150 million of annual revenues) seeking to transform their capital structures.

BDCs can invest in both debt and equity, which gives them an advantage over companies that invest in private debt or private equity alone.

Main Street Capital Corporation also invests in the private debt of middle-market companies (not lower middle-market companies) and has a budding asset management advisory business.

Source: Investor Presentation

Both transaction type and geography highly diversify holdings. By transaction type, the BDC acquires most of its deals via recapitalization and leveraged buyouts.

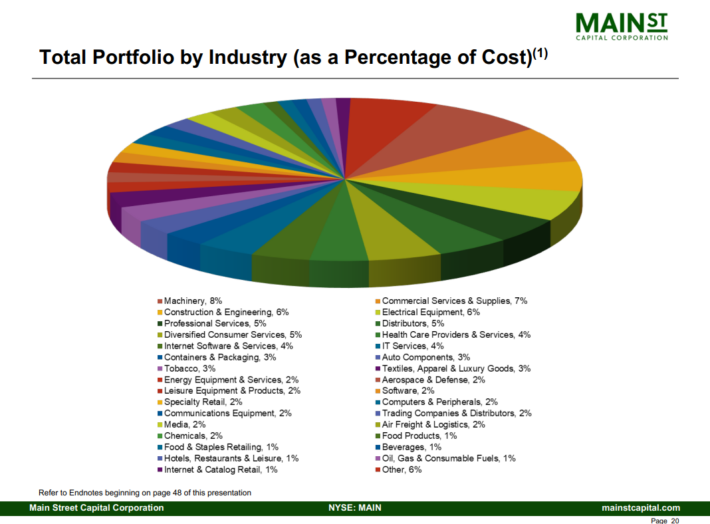

Main Street Capital Corporation also has a very high degree of industry diversification.

At the end of Q4 2025, Main Street had interests in 92 lower-middle-market companies (valued at $3.1 billion), 11 middle-market companies ($83 million), and 86 private loan investments ($2.0 billion).

Growth Prospects

Main Street Capital Corporation’s growth prospects come from its unique strategy of driving investment returns. In turn, the BDC sustains its high monthly dividend payout, and grows it over time.

On November 3rd, 2025, Main Street Capital announced a 2.0% dividend increase to $0.26 per share paid monthly. The current annualized dividend payout is $3.12 per share.

On February 26th, 2026, Main Street Capital reported fourth-quarter and full-year results. The quarter’s net investment income increased 6.0% to $92.1 million. Net investment income per share of $1.03 was up 5% year-over-year versus $0.98 per share in Q4 2024.

Distributable net investment income per share totaled $1.09, which was up 5% from the prior year. Main Street’s net asset value ended the quarter at $31.65, a 5.3% increase from the end of the previous year.

Main Street has established a solid record in the past decade, with a 10-year and five-year net investment income per share CAGR of 6.6% and 13.5%, respectively.

We expect MAIN to grow its net investment income per share by 1% per year over the next five years.

Dividend & Valuation Analysis

MAIN pays a monthly dividend. The company has also paid substantial supplemental dividends on various occasions. The most recent example was a supplemental payout of $0.30 per share that was declared on February 26th, 2026.

These are one-time special dividends, but we expect the company to continue this tradition of special dividends when distributable NII per share significantly exceeds its monthly dividend payouts.

The supplemental dividends have been a result of generating realized gains from Main Street’s equity investments.

Source: Investor Presentation

The dividend appears secure. For example, based on NII-per-share the company easily covered its dividend every year since 2021.

We expect MAIN to generate net investment income per share of $4.06 in 2026. With a forward annualized dividend payout of $3.12 per share, MAIN has an expected dividend payout ratio of approximately 77% for this year.

Its regular dividend growth and occasional special dividends imply that its dividend is in good shape.

To avoid corporate income tax as a BDC, Main Street must distribute at least 90% of its taxable income, leaving little wiggle room to fund growth.

While this strategy has worked extremely well since the last recession, we do caution that this method of funding becomes substantially less attractive (and more expensive) in weaker economic periods.

The main threat to the dividend is a recession, which would force many borrowers to default and cause interest rates on floating-rate loans to plummet.

As a result, earnings per share would likely decline rapidly, forcing the company to right-size its dividend. For now, however, the dividend appears to be safe.

In addition to the yield, net investment income per share growth and changes in valuation will also contribute to over all returns.

Shares of Main Street Capital are trading at 13.3 times expected NII at the moment, which is slightly below our target of 13.5. Multiple expansion could add 0.3% to annual returns over the next five years.

Along with our expectation for NII growth of 1% and the 5.8% dividend yield, we project total annual returns of 6.4% through 2031. The addition of special dividends could make for a higher total return as well.

Final Thoughts

Although Main Street Capital Corporation is off the radar for most dividend growth investors, this BDC has a strong history of delivering substantial shareholder returns.

The firm’s strong track record of superior investment management and expertise in the lower middle market segment gives it a strong competitive advantage in the private equity and debt industry.

Further, Main Street Capital Corporation is a shareholder-friendly BDC with a high yield and monthly payouts. Given total return projections, we rate the stock as a hold.

Further Reading: 20 Highest-Yielding BDCs

Don’t miss the resources below for more monthly dividend stock investing research.

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more