Updated on May 8th, 2026 by Felix Martinez

Investors seeking high yields may consider purchasing shares of Business Development Companies (BDCs). These stocks frequently have a higher dividend yield than the broader stock market average.

Some BDCs even pay monthly dividends.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

Oxford Square Capital Corporation (OXSQ) is a Business Development Company (BDC) that pays a monthly dividend. Oxford Square is also a highly yielding stock, with a yield of nearly 17% based on expected dividends for fiscal 2025. This is 12 times the average yield of the S&P 500.

However, investors should always keep in mind that the sustainability of a dividend is just as important, if not more so, than the yield itself.

BDCs often deliver high yields, but many (including Oxford Square) struggle to maintain their dividends, particularly during recessions. This article will examine the company’s business and growth prospects and evaluate the safety of its dividend.

Business Overview

Oxford Square Capital Corp. is a Business Development Company (BDC) specializing in financing early- and middle-stage businesses through loans and Collateralized Loan Obligations (CLOs). You can see our full BDC list here.

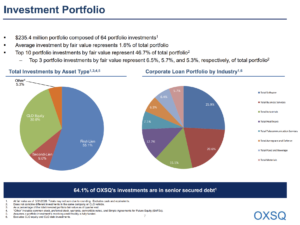

The company holds a well-diversified portfolio of First–Lien, Second–Lien, and CLO equity assets across seven industries, with the highest exposures in business services and software at 20.6% and 25.9%, respectively.

Source: Investor presentation

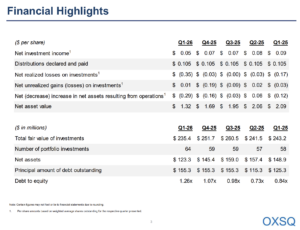

On April 22, 2026, Oxford Square announced its Q1 and 2026 results.

Source: Investor presentation

The company reported weaker first-quarter 2026 results, driven by lower investment income and significant realized investment losses.

Net investment income declined to $4.1 million, or $0.05 per share, compared to $6.1 million, or $0.09 per share, in the prior-year quarter. Total investment income also fell to $8.9 million from $10.2 million. The company recorded $30.7 million in realized investment losses, resulting in a $25.5 million decrease in net assets for the quarter.

Net asset value per share declined to $1.32 from $1.69 at the end of 2025. Despite weaker performance, Oxford Square continued to invest in its portfolio, deploying approximately $15.8 million during the quarter.

The company also raised approximately $12.3 million through its at-the-market stock offering program and declared monthly distributions of $0.035 per share for July, August, and September 2026.

Growth Prospects

The company’s investment income per share had been declining at an alarming rate, as financing became cheaper, preventing Oxford Square from refinancing at its previously higher rates. Additionally, the company has historically distributed dividends above its earnings, thereby eroding its NAV and future income generation by reducing its asset holdings.

Given that the Fed has not cut interest rates amid current economic uncertainty, we expect Oxford Square to generate stable per-share investment income in the near term.

The 2020 dividend cut should enable Oxford Square to retain some cash, hopefully allowing it to start regrowing its NAV. With rates unlikely to continue falling for the moment, income generation should stabilize.

With investments across a broad range of industries, Oxford Square has a reasonably balanced portfolio. The company’s top three industries do make up most of the portfolio, but they are in different areas of the economy. This provides some protection in the event of a downturn in one industry.

However, if rates decline over time, the company’s receivables could be further pressured, worsening its annual financial performance. Overall, we believe that the company’s future investment income generation carries substantial risks, while a potential recession and an adverse economic environment could severely damage its interest income.

Dividend Analysis

Oxford Square only recently began paying a monthly dividend, with the first being distributed in April 2019. Total dividends paid over the past few years are listed below:

- 2015 dividends: $1.14

- 2016 dividends: $1.16 (1.8% increase)

- 2017 dividends: $0.80 (31% decline)

- 2018 dividends: $0.80 (no increase)

- 2019 dividends: $0.80 (no increase)

- 2020 dividends: $0.6120 (23.5% decline)

- 2021 dividends: $0.42 (31.4% decline)

- 2022 dividends: $0.42 (Flat)

- 2023 dividends: $0.54(28.5% increase)

- 2024 dividends: $0.42 (22% decline)

- 2025 dividends: $0.42 (Flat)

Shareholders received a small increase in 2016, followed by three large dividend reductions since 2017. This inconsistency in dividend payout is due to the company’s volatile financial performance. Last year’s dividend total was negatively affected by the absence of the $ 0.12-per-share special dividend paid in 2023. The monthly payment has remained the same since the 2020 cut.

Oxford Square currently pays a monthly dividend of $0.035 per share, equaling an annualized payout of $0.42 per share.

Based on a full-year payout of $0.42 per share, Oxford Square stock yields 22.6%. Although the dividend cuts in recent years have been substantial, the dividend yield remains remarkably high. That said, investors should not focus solely on yield; dividend safety is a crucial consideration for income investors, and in this regard, Oxford Square leaves a lot to be desired.

Based on our expectation of full-year 2026 investment income per share of $0.30, the company is projected to maintain a 140% dividend payout ratio. Thus, the dividend looks to be unsafe.

Final Thoughts

Oxford Square boasts a robust business model, characterized by diversification across various investment assets and industries. The company has also taken steps to build up its less-risky asset position while reducing its reliance on riskier CLOs.

That said, Sure Dividend recommends that risk-averse investors avoid Oxford Square. We believe the dividend does not provide sufficient safety. The company distributes all of its investment income, essentially leaving little room for maneuver. Any decline in investment income could lead to further dividend cuts, making Oxford Square less attractive to investors seeking stable, secure income.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more