Updated on April 30th, 2026 by Josh Arnold

At first glance, PennantPark Floating Rate Capital (PFLT) is very appealing to income investors. That’s because PennantPark has a staggering 14%+ dividend yield. In addition, unlike many of its competitors, the company has managed to raise or maintain its dividend per-share payment for over a decade. This is unusual in a sector where dividend cuts are common.

PennantPark certainly qualifies as a high-dividend stock. Click here to see the entire list of 140 5%+ yielding stocks.

Not only that, but PennantPark also pays its dividends each month. This allows investors to compound their wealth even more quickly than a stock that pays a quarterly or semi-annual dividend, as well as providing more reliable income for those that use dividends for living expenses.

There are currently 119 monthly dividend stocks. You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

But, as is so often the case with sky-high dividend yields, PennantPark’s attractive dividend yield may be too good to be true.

This article will discuss the company’s business model and whether the payout is sustainable over the long term.

Business Overview

PennantPark is a Business Development Company, or BDC. It provides mostly debt financing, typically first-lien secured debt, senior notes, second-lien debt, mezzanine loans, or private high-yield debt. It specializes in making debt investments in middle-market companies. To a lesser extent, it also makes preferred and common equity investments. The most recent balance sheet showed that 90% of the company’s total investments were in first-lien senior secured debt.

Source: Investor Presentation

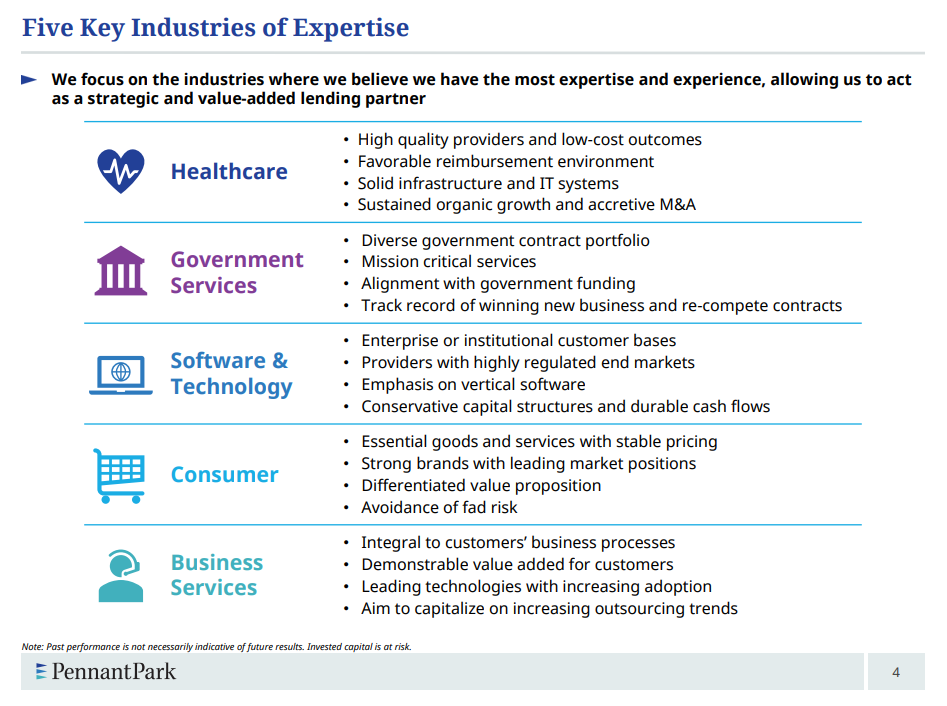

The company’s portfolio is highly diversified, with no particular industry making up more than 8% of the total mix, and the majority comprising less than 3% of the total.

In addition, the company’s portfolio has a floating rate, which opens up its yields to interest rate volatility. This can be good in times of rising rates but is unfavorable should rates decline.

An overview of the company’s investment philosophy reveals PennantPark prefers middle-market companies with $15 million to $50 million in annual EBITDA and has a high rate of underwriting success.

Credit quality has remained strong throughout the years, but there is inherent risk in the kinds of loans the company provides. PennantPark’s track record of outstanding underwriting is a key advantage, and this outstanding credit quality has helped the company maintain its dividend at the same rate for several years.

Source: Investor Presentation

Above is a sampling of the types of investments the company makes in target companies. Not only are the targets themselves from diverse industries and geographies, but PennantPark has a variety of instruments with which to make its investments.

First-lien secured debt is the preferred instrument given its favorable repayment position, but the company will do revolvers and equity injections as well. This is primarily a floating debt investment firm, however.

Growth Prospects

PennantPark has a track record of successful investments. However, its exposure to floating-rate instruments has caused its average portfolio yield to fall over the past several years. The yield on PennantPark’s portfolio peaked at just over 9% at the end of 2018, but the company faced declines in the subsequent years.

As PennantPark’s portfolio is comprised of floating rate instruments – mostly tied to LIBOR – it benefits when interest rates are increasing. Low rates over the past decade suppressed the company’s investment income, but the potential for higher rates is a future catalyst. To an extent, that has come true in 2022-2023 with rising rates.

The company posted first quarter earnings on February 10th, 2026 and results were decent. Core net investment income was 27 cents per share, meaning the company’s ability to pay the dividend remains quite stretched. Investing activity was $301 million at a weighted average interest rate of 10% across a mix of new and existing portfolio companies. The portfolio is 160 companies across 50 industries and a weighted average interest rate of 9.9%. About 99% of the portfolio was in floating-rate instruments and 89% was first lien senior secured debt. Leverage ended the quarter at 1.57X.

We see $1.13 in earnings-per-share for this year with one quarter out of the way. This doesn’t quite cover the dividend, as has been the case in recent years.

Dividend Analysis

PennantPark pays a monthly distribution of $0.1025 per share. The stock has a very attractive annualized dividend yield of 14%+. Even better, it makes monthly dividend payments, so investors receive their dividends more frequently than they would on a quarterly schedule.

Related: The 10 Highest Yielding Monthly Dividend Payers

However, it is also important to assess whether the dividend is sustainable. Abnormally high dividend yields could indicate that the dividend is in danger. We would expect a BDC to have a high yield, but the more than 14% yield is high even by BDC standards.

PennantPark Floating Rate also has a highly leveraged balance sheet and a payout ratio that often nears or exceeds 100% of earnings. While the company can probably sustain this model while the economy is running smoothly—as the stable dividend over the past decade has shown—it may collapse if the economy experiences a significant and prolonged downturn that causes its loans to underperform.

Despite an increase in 2023, shareholders should certainly not expect a distribution increase in the near term given how close the payout is to earnings today. PennantPark’s ability to grow its portfolio and average yields while controlling expenses will determine if the distribution is sustainable.

The company’s NII is not expected to cover the dividend this year with the payout ratio at 109%. We think the company can sustain this for a short while, but at some point will either need to grow earnings more quickly or cut the distribution. We note this hasn’t happened yet, but risks have risen for PennantPark given the way its portfolio is constructed with floating-rate instruments. Rates remain stable at the moment, but could be cut if growth slows. However, we don’t see the dividend as being at risk of being cut today. That said, it’s something investors should monitor continuously. If a cut were to come to fruition, it would like only need to be small.

Final Thoughts

The old saying “high-risk, high-reward” seems to apply to PennantPark. It certainly has an attractive dividend yield on paper, but if interest rates move lower, there could be dividend concerns down the road.

If everything goes according to plan, the stock’s yield alone could generate nearly double-digit total returns on an annual basis.

The company faces an elevated level of risk. If PennantPark does not grow investment income, it could be forced to reduce the dividend at some point in the future, but we do not currently forecast that.

Still, investors should tread carefully, and only those with a higher risk tolerance should consider buying PennantPark despite the very high yield.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more