Updated on May 2nd, 2026 by Josh Arnold

Primaris Real Estate Investment Trust (PMREF) is a Canada-based trust that focuses on enclosed shopping malls. It trades for a $1.6 billion market cap currently. While the trust reports in Canadian dollars and is listed in Toronto, we’ll focus here on its New York listing and US dollars.

Primaris has three appealing investment characteristics:

#1: It is a REIT so it has a favorable tax structure and pays out the majority of its earnings as dividends.

Related: List of publicly traded REITs

#2: It is a high-yield stock based on its 4.6% dividend yield.

Related: List of high-yield stocks

#3: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full list of monthly dividend stocks (along with relevant financial metrics like dividend yields and payout ratios), which you can access below:

Primaris Real Estate Investment Trust’s trifecta of favorable tax status as a REIT, a strong dividend yield, and a monthly dividend make it appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Primaris Real Estate Investment Trust.

Business Overview

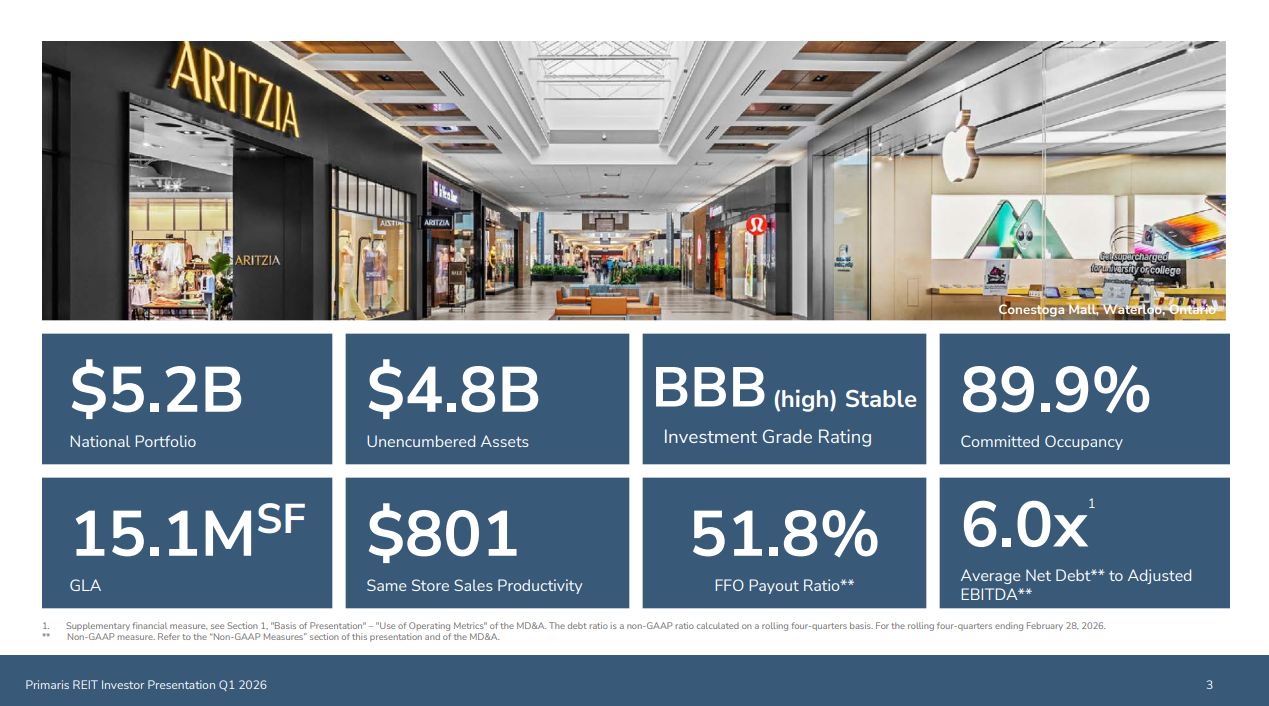

Primaris Real Estate Investment Trust is the only enclosed shopping center-focused REIT in Canada. Its ownership interests are primarily in dominant enclosed shopping centers in growing markets. Its asset portfolio totals 15.1 million square feet and has a value of approximately $3.8 billion.

Source: Investor Presentation

Like most mall REITs, Primaris REIT is facing a strong secular headwind, namely the shift of consumers from traditional shopping to online purchases. This trend has driven numerous brick-and-mortar stores out of business in recent years and has markedly accelerated since the onset of the coronavirus crisis.

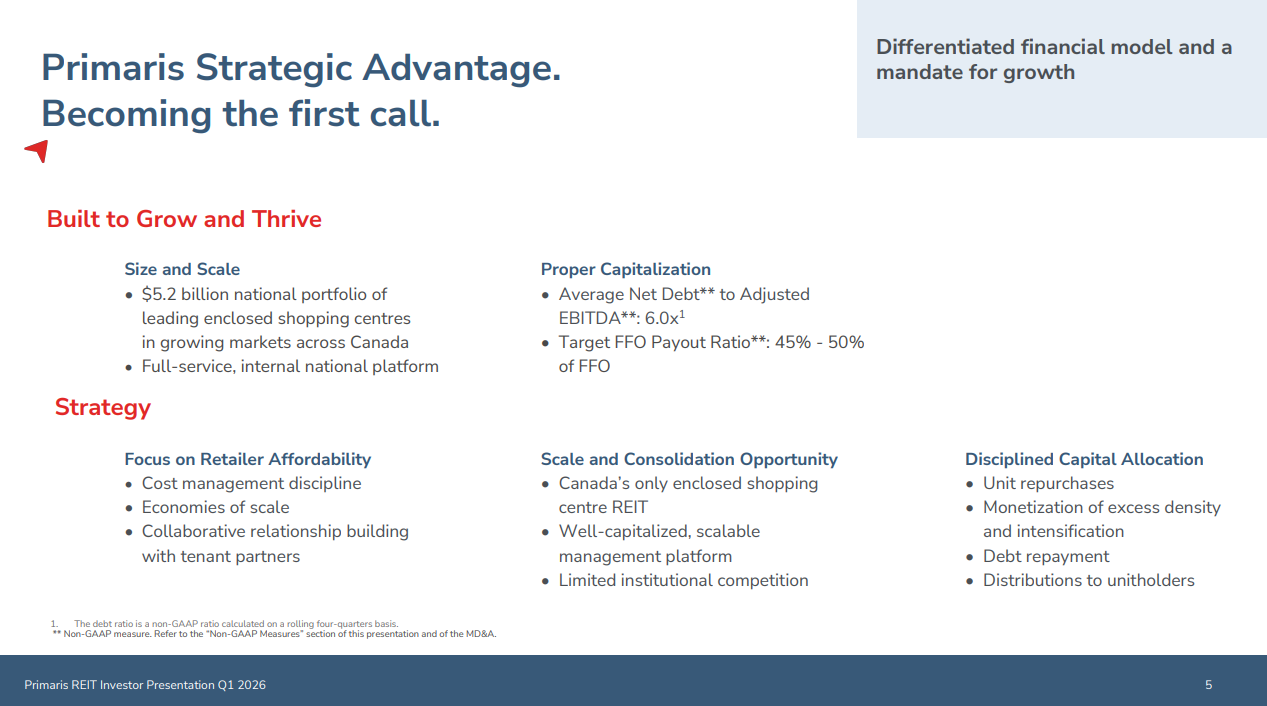

Primaris REIT is doing its best to adjust to the changing business landscape. To this end, the company tries to achieve economies of scale while also enabling and supporting omnichannel integration. We note that the company’s flagship malls are generating several hundred million dollars in annual retail sales each.

Moreover, Primaris REIT owns and operates shopping centers that constitute the primary retail mode in its markets. The REIT also targets shopping centers with annual sales of at least C$80 million to achieve the critical mass needed to achieve significant economies of scale.

Source: Investor Presentation

Furthermore, Primaris REIT tries to build multi-location tenant relationships to create deeper relationships with its tenants and benefit from such relationships in the long run.

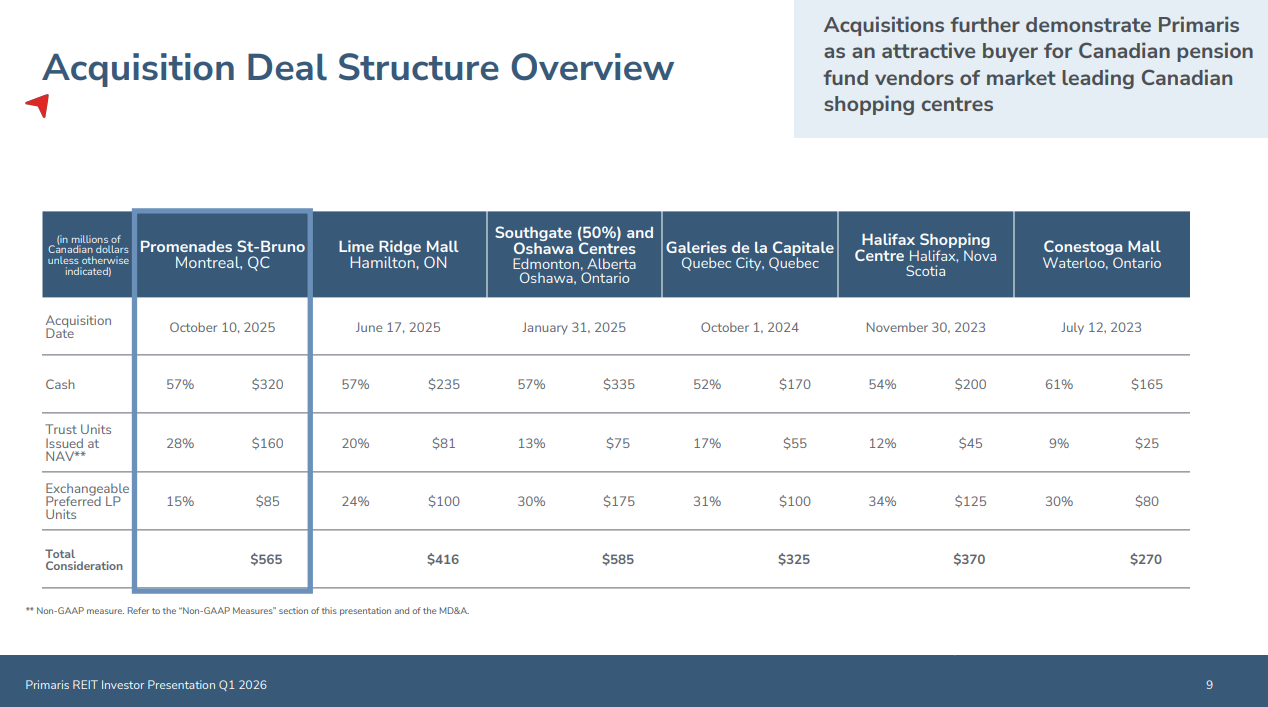

Primaris posted first quarter earnings on April 29th, 2026, and results showed revenue of $129 million, which was largely attributable to the change from the contribution of recent acquisitions. In addition, the trust enjoyed stable tenant sales productivity and rental revenue strength.

Cash net operating income was $67.5 million and funds-from-operations came to $43.1 million, or 31 cents per unit. These were down modestly year-over-year due to prior-year property tax recoveries and remaining drag from disclaimed HBC locations. Excluding this, FFO-per-share would have risen slightly.

The quarter ended with in-place occupancy of 86.4% and 89.9% committed occupancy, with leasing spreads of 5.5% across 372k square feet of renewals. We see $1.37 per share in FFO for this year as the management team focuses on executing its capital recycling strategy.

Growth Prospects

Thanks to the characteristics of its core markets, Primaris REIT has some significant growth drivers. In its markets, the population and average household income are expected to grow by a low to mid-single-digit growth rate going forward. This means higher revenues for the shopping centers and, hence, higher revenues for Primaris REIT.

Moreover, as occupancy is currently standing below historical average levels, there is ample room for future growth for this REIT. Management is confident in sustained growth in the upcoming years. We note there hasn’t been noticeable improvement in occupancy as of the end of the first quarter 2026.

On the other hand, investors should never forget the strong secular headwind from the shift of consumers toward online shopping. While Primaris REIT is doing its best to adjust to the new business environment, the secular shift of consumers will almost certainly continue exerting a substantial drag on the business of the REIT. Overall, we find it prudent to assume just a 1.0% average annual growth of FFO per unit over the next five years to be safe. That is in line with estimated growth of just three cents per share in FFO for this year.

Dividend & Valuation Analysis

Primaris REIT is currently offering a 4.6% dividend yield. It is thus an interesting candidate for income-oriented investors but the latter should be aware that the dividend may fluctuate significantly over time due to the gyrations of the exchange rate between the Canadian dollar and the USD. Thanks to its decent business model, solid payout ratio of 47%, the trust is not likely to cut its dividend in the absence of a severe recession.

Notably, Primaris REIT has maintained a stronger balance sheet than most REITs to have sufficient financial strength to endure the secular decline of malls and the effect of a potential recession on its business. The company has a decent balance sheet, with a leverage ratio (Net Debt to EBITDA) of ~6x.

On the other hand, market interest rates are higher than they’ve been for many years. This is a headwind for the vast majority of REITs, including Primaris REIT. If high inflation persists for much longer than currently anticipated, high interest rates will probably take their toll on Primaris REIT’s bottom line.

Regarding valuation, Primaris REIT is currently trading for 10.2 times its expected FFO for this year.

Given the headwind from online shopping, we assume a fair price-to-FFO ratio of 9.0 for the stock. Therefore, the current FFO multiple is slightly lower than our assumed fair price-to-FFO ratio. If the stock trades at its fair valuation level in five years, then valuation would add a small amount to total returns.

Considering the 1% annual FFO-per-share growth, the 4.6% dividend, and a slight headwind from multiple contraction, Primaris REIT could offer a low single-digit average annual total return over the next five years. While not enough to warrant a buy recommendation at this time, investors who prioritize safe income might find Primaris REIT to be an attractive investment option.

Final Thoughts

Primaris REIT is the only REIT in Canada focused on enclosed shopping centers. With a ~5% dividend yield and a solid payout ratio of 47%, it is an attractive candidate for income-oriented investors’ portfolios, given the S&P 500 is yielding just 1%.

On the other hand, investors should be aware of the risks of this REIT. Due to its focus on malls, Primaris REIT is vulnerable to recessions, while it also faces a strong headwind due to the shift of consumers from brick-and-mortar shops to online purchases. Only investors who are comfortable with these risks should consider purchasing this stock.

Moreover, Primaris REIT is characterized by exceptionally low trading volume. It is hard to establish or sell a prominent position in this stock.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more