Updated on August 1st, 2026 by Nikolaos Sismanis

With contributions from Ben Reynolds

Real estate investment trusts – or REITs, for short – are compelling investment vehicles.

That’s because:

- They provide diversified real estate exposure

- Without the high up-front cost of traditional real estate

- They often have high dividend yields well in excess of the S&P 500

- They are required by law to distribute 90% of earnings to investors

Bonus: You can download your free 200+ REIT list spreadsheet, complete with metrics that matter, by clicking on the link below:

In addition to the downloadable Excel sheet of all REITs, this article discusses why income investors should pay particularly close attention to this asset class.

And, we also include our top 7 REITs today based on expected total returns.

Table Of Contents

In addition to the full downloadable Excel spreadsheet, this article covers our top 7 REITs today, as ranked using expected total returns from The Sure Analysis Research Database.

The table of contents below allows for easy navigation.

- Why Invest In REITs?

- REIT Financial Metrics

- The Top 7 REITs Today

#7: Innovative Industrial Properties (IIPR)

#6: UMH Properties (UMH)

#5: American Tower (AMT)

#4: Rexford Industrial Realty (REXR)

#3: Community Healthcare Trust (CHCT)

#2: VICI Properties (VICI)

#1: NexPoint Residential Trust (NXRT)

Why Invest in REITs?

REITs are, by design, a fantastic asset class for investors looking to generate income.

Thus, one of the primary benefits of investing in these securities is their high dividend yields.

The currently high dividend yields of REITs is not an isolated occurrence. In fact, this asset class has traded at a higher dividend yield than the S&P 500 for decades.

The high dividend yields of REITs are due to the regulatory implications of doing business as a real estate investment trust.

In exchange for listing as a REIT, these trusts must pay out at least 90% of their net income as dividend payments to their unit holders (REITs trade as units, not shares).

Sometimes you will see a payout ratio of less than 90% for a REIT, and that is likely because they are using funds from operations, not net income, in the denominator for REIT payout ratios (more on that later).

REIT Financial Metrics

REITs run unique business models. More than the vast majority of other business types, they are primarily involved in the ownership of long-lived assets.

From an accounting perspective, this means that REITs incur significant non-cash depreciation and amortization expenses.

How does this affect the bottom line of REITs?

Depreciation and amortization expenses reduce a company’s net income, which means that sometimes a REIT’s dividend will be higher than its net income, even though its dividends are safe based on cash flow.

To give a better sense of financial performance and dividend safety, REITs developed the financial metric funds from operations, or FFO.

Just like earnings, FFO can be reported on a per-unit basis, giving FFO/unit – the rough equivalent of earnings-per-share for a REIT.

FFO is determined by taking net income and adding back various non-cash charges that are seen to artificially impair a REIT’s perceived ability to pay its dividend.

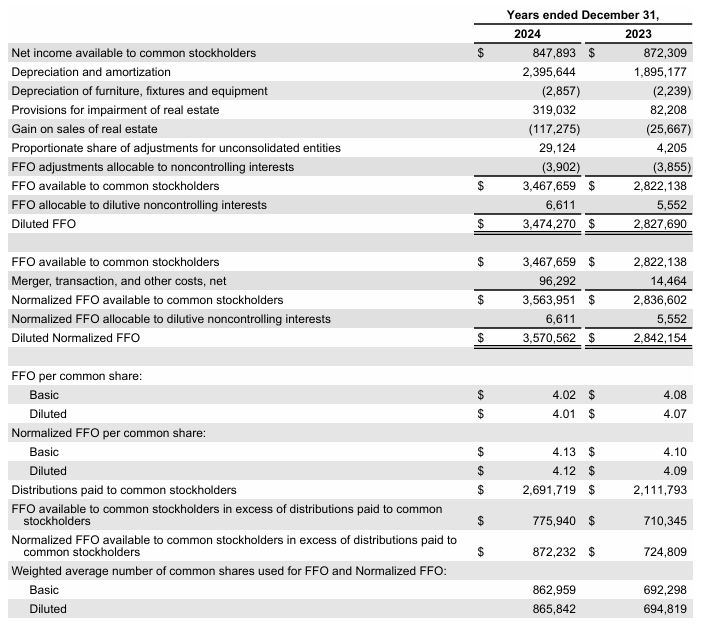

For an example of how FFO is calculated, consider the following net income-to-FFO reconciliation from Realty Income (O), one of the largest and most popular REIT securities.

Source: Realty Income Annual Report

In 2024, net income was $847 million while FFO available to stockholders was above $3.4 billion, a sizable difference between the two metrics.

This shows the profound effect that depreciation and amortization can have on the GAAP financial performance of real estate investment trusts.

The Top 7 REITs Today

Below we have ranked our top 7 REITs today based on expected total returns.

Expected total returns are in turn made up from dividend yield, expected growth on a per unit basis, and valuation multiple changes. Expected total return investing takes into account income (dividend yield), growth, and value.

Note: The REITs below have not been vetted for safety. These are high expected total return securities, but they may come with elevated risks.

We encourage investors to fully consider the risk/reward profile of these investments.

For the Top 10 REITs each month, based on expected total returns and safety, see our Top 10 REITs service.

Top REIT #7: Innovative Industrial Properties (IIPR)

- Expected Total Return: 12.5%

- Dividend Yield: 12.4%

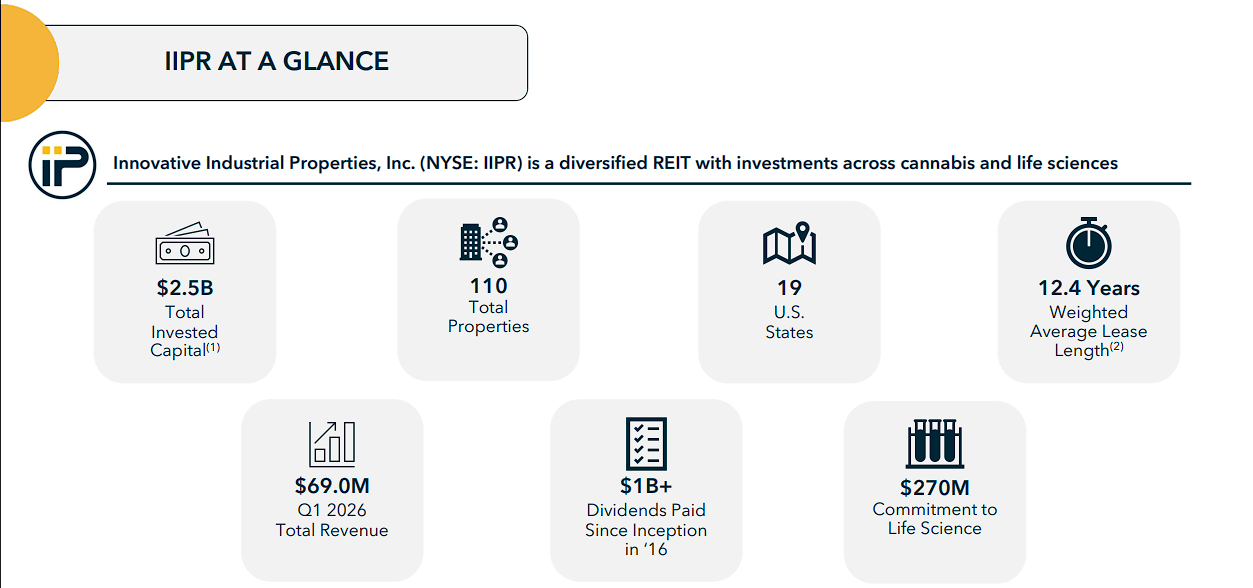

Innovative Industrial Properties (IIPR) is an internally managed specialty REIT that owns regulated-cannabis cultivation and processing facilities and also holds selected life-science investments.

At March 31st, 2026, it owned 110 properties across 19 states, totaling 8.9 million rentable square feet and $2.5 billion of invested capital.

First-quarter revenue declined 3.8% year-over-year to $69.0 million, primarily because tenant defaults reduced revenue by $6.9 million.

Net income attributable to common shareholders was nearly unchanged at $30.2 million, or $1.02 per diluted share.

Adjusted FFO was $53.4 million, or $1.88 per share, versus $1.94 one year earlier.

Management is working to stabilize the portfolio through new leasing and tenant resolutions.

IIPR executed leases covering 389,000 square feet year-to-date through the first-quarter report and raised $128 million of equity and debt capital.

Prospective replacement tenants have also been identified for four former 4Front properties, although licensing and receivership timelines remain important execution risks.

The quarterly dividend remains $1.90 per share, or $7.60 annualized.

Because first-quarter AFFO per share was slightly below the payout, the seemingly very high, and thus attractive, yield should be viewed alongside tenant-credit risk and the need for successful re-leasing.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on IIPR.

Top REIT #6: UMH Properties (UMH)

- Expected Total Return: 13.1%

- Dividend Yield: 5.7%

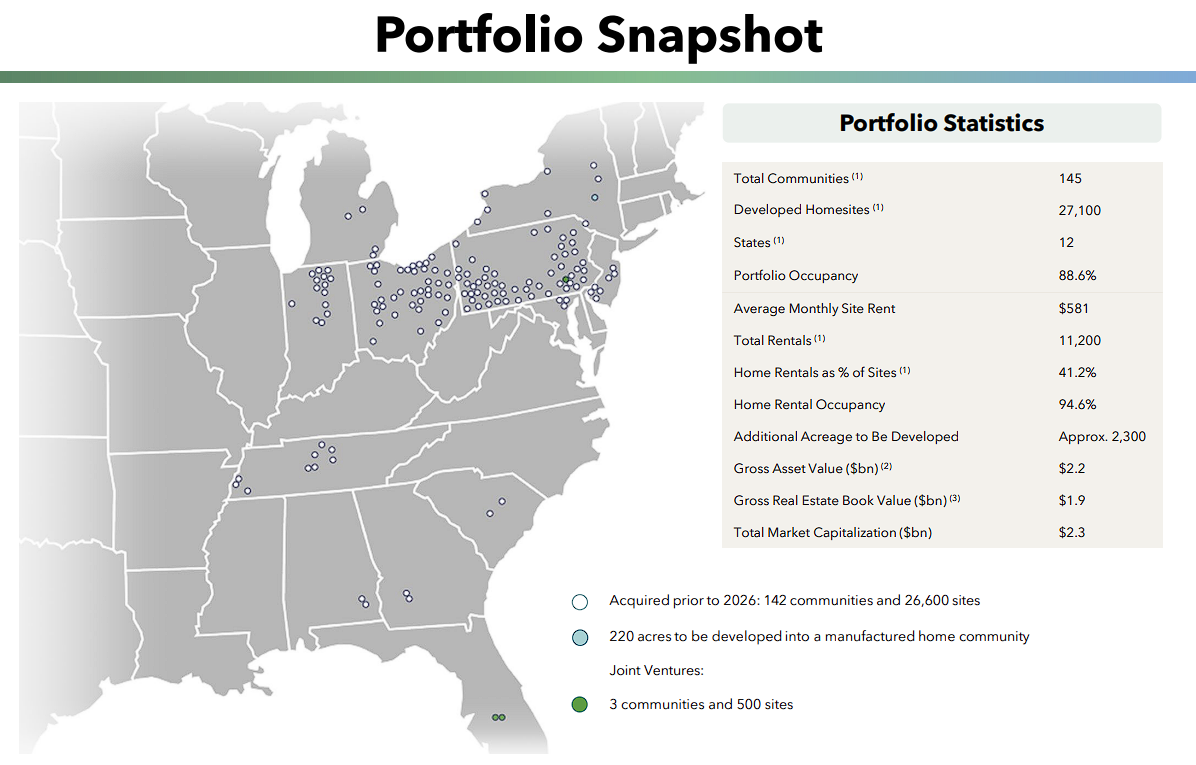

UMH Properties (UMH) owns and operates manufactured-home communities, primarily in the eastern United States. Its strategy combines recurring site rent, a large rental-home portfolio, home sales, and selective acquisitions. Manufactured housing benefits from a persistent shortage of affordable housing, while UMH can create value by filling vacant sites and converting inventory into revenue-producing rentals.

For the first quarter of 2026, total income increased 8% to $65.8 million. Net income attributable to common shareholders improved to $2.6 million, or $0.03 per share, from a small loss a year earlier.

Normalized FFO rose to $19.4 million, while normalized FFO per share held steady at $0.23 because of a higher share count.

Operating momentum has remained healthy. UMH converted 146 homes into rentals during the first quarter, and its approximately 11,200 rental homes were 94.6% occupied.

A July operating update showed total rental and related income up 10.3% year-over-year and home-sales income up 9.2%, reflecting further occupancy gains and rent increases.

The quarterly dividend is $0.225 per share, or $0.90 annualized.

That payout is about equal to four times first-quarter normalized FFO per share, so continued occupancy and per-share cash-flow growth will be important to support future dividend increases.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on UMH.

Top REIT #5: American Tower (AMT)

- Expected Total Return: 14.2%

- Dividend Yield: 4.0%

American Tower (AMT) is one of the world’s largest communications-infrastructure REITs. It leases space on towers and other sites to wireless carriers and also owns CoreSite, a portfolio of interconnected U.S. data centers.

The model benefits from recurring contractual revenue and rising demand for mobile data, cloud connectivity, and low-latency computing.

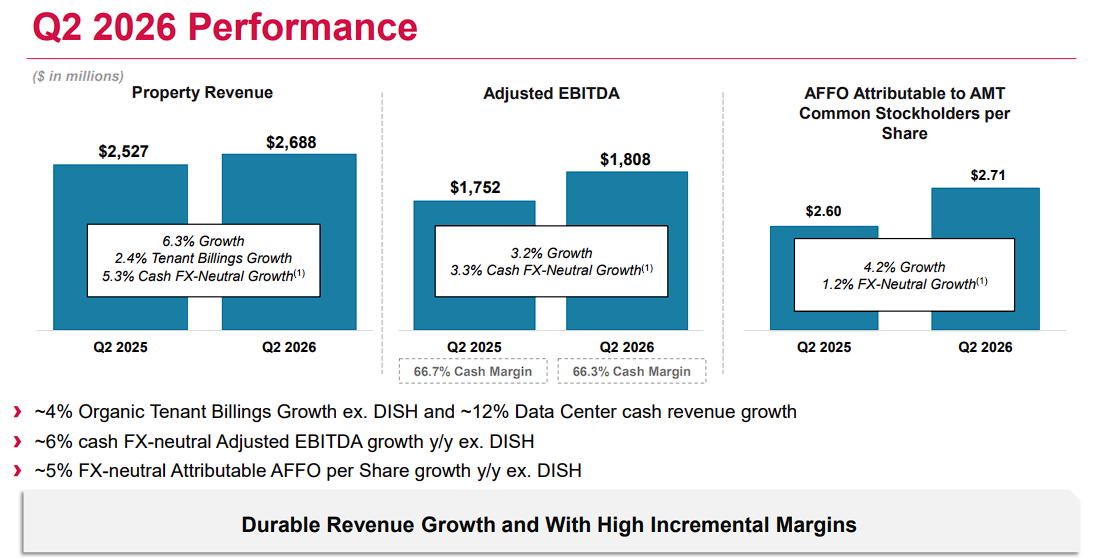

Second-quarter 2026 revenue increased 4.7% to $2.75 billion, while property revenue grew 6.3% to $2.69 billion.

Net income rose 133% to $888 million, partly reflecting favorable currency movements, and AFFO attributable to common shareholders increased 3.8% to $1.26 billion.

Net leverage ended the quarter at 4.9 times annualized adjusted EBITDA.

CoreSite remained a meaningful growth engine, with record leasing activity and strong demand connected to hybrid cloud and artificial-intelligence workloads.

American Tower raised its full-year outlook for the second time in 2026 and continues to direct most discretionary capital toward developed markets, including data-center development and new tower construction.

The REIT pays a quarterly dividend of $1.79 per share, or $7.16 annualized.

The payout is well covered by expected AFFO, while the 4.0% yield gives investors a combination of current income and exposure to long-term growth in digital infrastructure.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on AMT.

Top REIT #4: Rexford Industrial Realty (REXR)

- Expected Total Return: 14.8%

- Dividend Yield: 4.5%

Rexford Industrial Realty (REXR) owns, operates, and redevelops industrial properties exclusively in infill Southern California.

As of June 30th, 2026, the portfolio included 409 properties and approximately 50 million square feet.

The region’s limited land supply and large consumption base create attractive long-term fundamentals, although leasing conditions can still fluctuate with the economic cycle.

Second-quarter Core FFO increased 1.2% to $141.4 million, while Core FFO per share rose 6.8% to $0.63.

Same-property cash NOI increased 1.5%, average same-property occupancy was 95.7%, and the company completed 2.1 million square feet of leasing.

However, comparable rents declined 2.8% on a net-effective basis and 11.3% on a cash basis.

Rexford is undertaking a significant portfolio realignment, increasing 2026 disposition guidance to $1.5 billion to $2.0 billion.

Assets identified for sale produced a $624.8 million non-cash impairment in the quarter.

Proceeds are intended to strengthen the balance sheet and fund higher-return opportunities, including repurchases; the board authorized a new $1.0 billion buyback program.

The quarterly dividend remains $0.435 per share, or $1.74 annualized.

Updated 2026 Core FFO guidance of $2.38 to $2.43 per share indicates reasonable coverage, but you should monitor leasing spreads and the execution of the disposition plan.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on REXR.

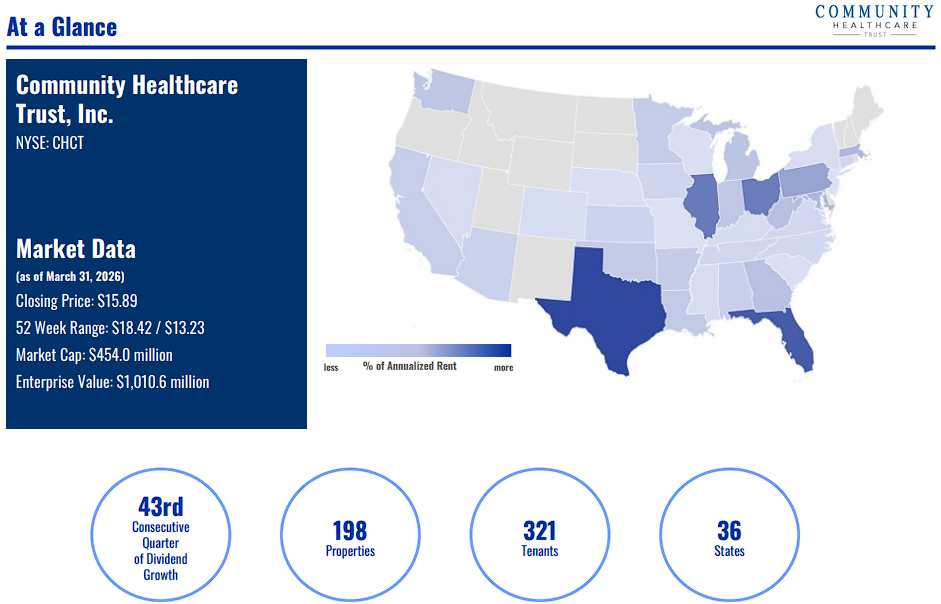

Top REIT #3: Community Healthcare Trust (CHCT)

- Expected Total Return: 15.3%

- Dividend Yield: 10.2%

Community Healthcare Trust (CHCT) owns outpatient-oriented healthcare properties in smaller U.S. markets, including medical offices, specialty centers, behavioral facilities, and inpatient rehabilitation facilities.

At March 31st, 2026, the portfolio comprised 198 properties across 36 states, with roughly 4.5 million square feet.

Its focus on smaller individual assets can produce attractive acquisition yields with less institutional competition.

First-quarter net income was approximately $2.5 million, or $0.07 per diluted share. FFO and AFFO were $0.49 and $0.56 per share, respectively.

Rental income rose to $31.3 million, while the portfolio was 89.8% leased with a weighted-average remaining lease term of approximately 7.2 years.

During the quarter, CHCT acquired a fully leased Florida inpatient-rehabilitation facility for $28.5 million, with a lease extending to 2044, and sold one property for approximately $5.2 million.

Four additional properties were under definitive purchase agreements for an aggregate expected price of about $99 million, providing a visible growth pipeline if the developments are completed and occupied as planned.

The board raised the quarterly dividend to $0.48 per share, continuing CHCT’s record of increasing the payout every quarter since its 2015 IPO.

The 10.2% yield is appealing, but the annualized $1.92 dividend consumes most expected AFFO, leaving limited room for tenant problems or financing pressure.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on CHCT.

Top REIT #2: VICI Properties (VICI)

- Expected Total Return: 16.3%

- Dividend Yield: 6.7%

VICI Properties (VICI) is an experiential net-lease REIT whose portfolio is anchored by major gaming properties operated by tenants such as Caesars Entertainment and MGM Resorts.

Its long-term triple-net leases shift property expenses to tenants and generally include contractual rent escalators, giving VICI a predictable base of rental income.

Second-quarter 2026 revenue increased 5.7% to $1.1 billion. AFFO attributable to common shareholders grew 7.8% to $679.6 million, while AFFO per share rose 4.6% to $0.62.

GAAP net income fell to $0.48 per share because of a $413.1 million year-over-year change in the non-cash credit-loss allowance, making AFFO more informative for recurring performance.

VICI continued to diversify its tenant roster. It closed a $1.16 billion acquisition of seven Nevada casino properties, added a lease tied to MGM Northfield Park, bought gaming assets in Alberta, and began a build-to-suit relationship with Club Med in St. Croix.

These transactions added several new operators and broadened the portfolio beyond its largest legacy tenants.

Management updated 2026 AFFO guidance to $2.45 to $2.47 per share.

Against the $1.80 annualized dividend, coverage remains comfortable, while the 6.7% yield and embedded lease escalators support the income case.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on VICI.

Top REIT #1: NexPoint Residential Trust (NXRT)

- Expected Total Return: 18.5%

- Dividend Yield: 7.8%

NexPoint Residential Trust (NXRT) owns middle-income apartment communities with value-add potential in large Sun Belt markets, primarily across the Southeastern and Southwestern United States.

The strategy centers on renovating units, improving amenities, and raising rents while maintaining affordable positioning relative to newly constructed apartments.

First-quarter 2026 revenue edged up to $63.5 million, but same-store revenue and NOI declined 2.2% and 2.7%, respectively.

The 36-property portfolio contained 13,304 units, with 93.5% physical occupancy and a $1,485 weighted-average monthly rent.

Core FFO fell to $17.3 million, or $0.68 per share, from $0.75 per share a year earlier; AFFO was $19.6 million, or $0.77 per share.

The value-add program remains productive despite softer same-store results. NXRT completed 300 full and partial upgrades during the quarter and achieved a 19% return on those investments.

It also used proceeds from a new property mortgage to reduce its credit-facility balance by $33 million, an important step while interest costs remain elevated.

The quarterly dividend is $0.53 per share, or $2.12 annualized, and was covered by first-quarter AFFO.

The 7.8% yield is meaningful, but the investment case depends on stabilizing same-store revenue and maintaining occupancy as the Sun Belt apartment market absorbs new supply.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on NXRT.

Final Thoughts

The REIT Spreadsheet list in this article contains a list of publicly-traded Real Estate Investment Trusts.

However, this database is certainly not the only place to find high-quality dividend stocks trading at fair or better prices.

In fact, one of the best methods to find high-quality dividend stocks is looking for stocks with long histories of steadily rising dividend payments.

Companies that have increased their payouts through many market cycles are likely to continue doing so for a long time to come.

You can see more high-quality dividend stocks in the following Sure Dividend databases, each based on long streaks of steadily rising dividend payments:

- Dividend Kings List: Dividend Stocks With 50+ Years of Rising Dividends

- Dividend Aristocrats List: 25+ Years of Rising Dividends

You might also be looking to create a highly customized dividend income stream to pay for life’s expenses.

The following lists provide useful information on high dividend stocks and stocks that pay monthly dividends: