Updated on Febuaury 12th, 2026 by Felix Martinez

The Dividend Aristocrats are 69 S&P 500 companies with 25+ consecutive years of dividend increases. The Dividend Aristocrats each have strong business models and competitive advantages that enable them to raise their dividends each year.

There are currently 69 Dividend Aristocrats. You can download an Excel spreadsheet of all 69 Dividend Aristocrats (with important financial metrics such as price-to-earnings ratios and dividend yields) by clicking the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

In order to become a Dividend Aristocrat, a company must possess a profitable business model and durable competitive advantages, along with the ability to raise dividends even during recessions.

Consumer staples stocks such as Amcor plc (AMCR) have all the necessary qualities of a Dividend Aristocrat.

Amcor has increased its dividend for over 28 consecutive years. Thanks to a very strong product portfolio, it has maintained its dividend growth streak.

Business Overview

Amcor plc, which trades on the NYSE, was formed in June 2019 following the merger of two packaging companies: U.S.-based Bemis Co., Inc., and Australia-based Amcor Ltd.

Amcor develops and manufactures a wide range of packaging products for many consumer uses worldwide, including food and beverage, medical and medicinal, and home and personal care.

It consists of two main business segments: Flexible Packaging and Rigid Packaging.

Source: Investor Presentation

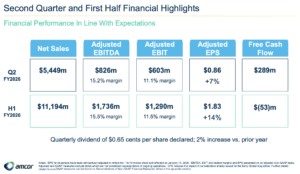

Amcor reported solid Q2 FY2026 results, driven largely by the Berry Global acquisition. Adjusted EPS rose 7% to $0.86, beating estimates by $0.02, while revenue jumped 68% year over year to $5.45 billion, though it modestly missed expectations. Adjusted EBITDA increased 83% to $826 million and adjusted EBIT rose 66% to $603 million, with margins improving to 15.2% and 11.1%, respectively.

Synergies from the Berry deal totaled $55 million in the quarter, landing at the high end of expectations, while free cash flow reached $289 million despite $69 million of integration and restructuring costs. Volumes declined modestly (~1.5%), reflecting a challenging demand environment.

For the first half of FY2026, Amcor delivered adjusted EPS of $1.83, up 14%, on 70% revenue growth to $11.2 billion. Adjusted EBITDA climbed 89% to $1.74 billion, and adjusted EBIT rose 77% to $1.29 billion, supported by $83 million of cumulative synergies.

Management reaffirmed full-year FY2026 guidance, calling for adjusted EPS of $4.00–$4.15 (12–17% constant-currency growth) and free cash flow of $1.8–$1.9 billion, underpinned by at least $260 million of pre-tax Berry synergies, ongoing cost discipline, and portfolio optimization initiatives.

Source: Investor Presentation

Growth Prospects

Amcor is counting on its Bemis acquisition to drive strong growth over the next half-decade. The main factors that will drive this growth acceleration are its global footprint, which will open up new attractive end markets and customers for the company’s products, and greater economies of scale, which will drive efficiencies and higher margins.

Another growth catalyst for Amcor is the emerging markets such as China and Latin America, where economic growth is high, and demand for packaging products is rising.

The company is also undertaking an aggressive share buyback program, which should boost per-share growth.

Furthermore, its balance sheet is strong, with a relatively low leverage ratio, giving it the flexibility to fund dividends and share repurchases while remaining opportunistic about future growth opportunities.

We believe these factors should combine to deliver solid 5% annualized earnings-per-share growth over the next half-decade.

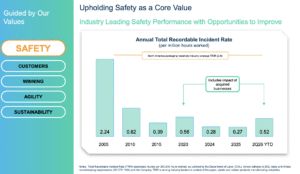

Competitive Advantages & Recession Performance

Its industry leadership positions Amcor for a competitive advantage. Although Amcor’s headquarters are in Europe, its largest markets are in the Americas. That means Amcor should be relatively safe from potential future declines to the pound (or to the Australian dollar, for that matter).

In addition, Amcor’s products are used every day around the world. People around the world will continue to need packaging. Amcor’s emphasis on recyclable and reusable products should appeal to more environmentally conscious end users, while the merger with Bemis offers significant prospects in developing markets.

Additionally, with the merger into a single, large manufacturing entity, Amcor has increased its ability to negotiate better supplier costs. This should make Amcor an unstoppable force in the packaging industry.

Amcor is also fairly resistant to recessions. As Amcor exists today (post-merger), it was not a publicly traded company during the Great Recession, so its earnings-per-share performance during the downturn is unavailable.

It is reasonable to assume Amcor’s earnings per share would decline somewhat during a recession, as the company’s global business model relies on economic growth. But it should continue paying (and raising) its dividend each year for the foreseeable future.

Valuation & Expected Returns

We expect Amcor to generate earnings per share of $4.00 in 2026. Based on this, Amcor’s shares are currently trading at a price-to-earnings ratio of 12.5x.

Even using a conservative multiple, we think that a recession-resistant Dividend Aristocrat with mid-single-digit growth prospects, such as Amcor, should trade for 15 times earnings. Therefore, we view the stock as undervalued.

A fair five-year expected earnings-per-share growth rate of 5.0% and the 5.2% dividend yield will help boost shareholder returns. We expect annualized total returns of approximately 13.2% through 2031.

Final Thoughts

Amcor is uniquely positioned for strong growth in the coming years, thanks to its recent acquisition, which has opened several new, attractive end markets and created opportunities to unlock valuable synergies. Furthermore, the company has a balance sheet with sufficient capacity to fund growth investments and share repurchases, which should boost EPS going forward.

As a result, we think that shares offer decent value here. With expectations of ~13.2% annualized total returns over the next half-decade, we view Amcor as an attractive buy right now.

That said, it could be an opportunity for dividend growth investors with a more conservative outlook, as its 5.2% yield is above average for the S&P 500, and its strong growth track record and recession-resistant business model make it an attractive long-term holding.

Finally, given its solid growth outlook, it will likely continue to increase its dividend for the foreseeable future.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 54 stocks with 50+ years of consecutive dividend increases.

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: