Updated on March 11th, 2026 by Felix Martinez

Every year, we publish a review of each Dividend Aristocrat, a group of 69 companies in the S&P 500 Index with 25+ consecutive years of dividend increases. Thanks to their long histories of annual dividend increases and strong business models, we believe the Dividend Aristocrats are among the best dividend stocks to buy.

With that in mind, we created a list of all 69 Dividend Aristocrats. You can download your copy of the Dividend Aristocrats list (along with important metrics like dividend yields and price-to-earnings ratios) by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Next on our list of Dividend Aristocrats is Target Corporation (TGT).

Target has a long history of dividend growth. The company has grown its dividend for 57 consecutive years. Target is a Dividend King, an even more exclusive list of companies that have increased dividends for at least 50 consecutive years.

Target has been one of the best-performing retail stocks over the last five years, thanks to its execution of numerous growth initiatives.

Business Overview

Target is a discount retail giant with a market capitalization of $55 billion. Today, it operates approximately 1,956 stores in the U.S. and an e-commerce business. It has a diverse product lineup and annual sales exceeding $105 billion.

The company has implemented many growth initiatives in recent years. As a result, Target has returned to its long-term growth trajectory in the last five years.

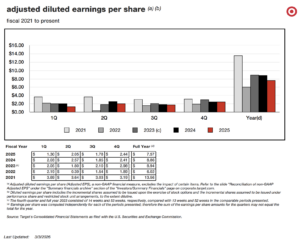

Target reported Q4 2025 net sales of $30.5 billion, a 1.5% year-over-year decline, while adjusted EPS came in at $2.44, beating expectations and slightly above last year’s $2.41. Comparable sales fell 2.5%, driven by a 3.9% decline in store traffic, partially offset by 1.9% growth in digital sales.

Despite weaker sales, the company benefited from stronger performance in food & beverage, beauty, and toys, as well as rapid growth in non-merchandise revenue streams, including advertising, membership services, and its marketplace platform.

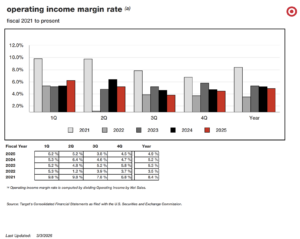

Profitability remained relatively stable despite the softer revenue environment. Fourth-quarter operating income declined 5.9% to $1.38 billion, while the operating margin fell to 4.5% from 4.7% in the prior year.

However, gross margin improved to 26.6% from 26.2%, reflecting lower inventory shrinkage, reduced supply chain costs, and higher advertising revenue, partially offset by higher product costs and merchandising activity.

For full-year 2025, Target generated $104.8 billion in revenue, down 1.7% year over year, while GAAP EPS declined to $8.13 from $8.86. Operating income fell 8.1% to $5.1 billion, and return on invested capital decreased to 13.8% from 15.4%.

Looking ahead, management expects 2026 net sales growth of about 2%, with EPS guidance of $7.50–$8.50 and modest margin expansion, supported by improved merchandising, technology investments, and continued growth in digital and membership services.

Source: Investor Presentation

Growth Prospects

Target has grown its earnings per share by an average of 8% per year over the last decade. The retailer stagnated during 2012-2017 due to its failed attempt to expand into Canada, but thanks to growth initiatives, it has returned to strong growth since 2017.

The biggest reason for this excellent growth is that Target has invested heavily in growing new sales channels, which have paid off. First, Target has invested heavily in e-commerce. The rise in e-commerce initially caught many retail companies, including Target, off guard. Target has revamped its online offerings and has seen rapid growth.

Target has also rolled out its same-day fulfillment service. Lastly, the company continues to redevelop stores and build smaller stores with much less square footage in places that cannot provide the necessary space for a large store. These stores are located in areas that see high traffic, such as densely populated large cities and college campuses.

Taken together, these measures have significantly affected Target’s growth. We expect Target to grow its earnings per share by 7% per year over the next five years.

Source: Investor Presentation

Competitive Advantages & Recession Performance

Target operates in a difficult industry. Retail is highly competitive and thus characterized by razor-thin profit margins. Retail brands often take a back seat to price and convenience for consumers.

This is why Target has invested so heavily in store redevelopment. That has enabled the company to retain its brand strength, even in a fiercely competitive industry. Most importantly, the retailer has massive distribution and scale capabilities that allow it to keep prices low.

In addition, Target operates in a defensive retail niche. Discount retail tends to hold up relatively well during economic downturns, when consumers typically shift from higher-priced retailers.

Target’s earnings-per-share during the Great Recession are as follows:

- 2007 earnings-per-share of $3.33

- 2008 earnings-per-share of $2.86 (14% decline)

- 2009 earnings-per-share of $3.30 (15% increase)

- 2010 earnings-per-share of $3.88 (17% increase)

- 2011 earnings-per-share of $4.28 (10% increase)

Target proved remarkably resilient during the Great Recession. It posted a 14% decline in 2008 but followed this with three consecutive years of double-digit earnings growth.

Target once again performed very well in 2020, a year when the U.S. economy experienced a severe recession due to the pandemic. And yet, Target continues to raise its dividend reliably each year.

Valuation & Expected Returns

Based on the current share price of $121, Target has a price-to-earnings ratio of 15.1x. Our fair value multiple is 17. If shares were to revert to their average price-to-earnings ratio, TGT stock would see annual returns increase by 2.4% over the next five years due to an increasing P/E multiple.

At the same time, Target is offering a 3.8% dividend yield. With an expected annual earnings-per-share growth rate of 7%, total returns are projected to be 12.3% per year over the next five years. This is a fairly attractive expected return for such a recession-resistant business model.

With annualized expected returns above 12.3%, we rate TGT stock a hold.

Final Thoughts

Target has faced some major downturns over the last decade. It failed to expand into Canada and struggled to adapt to the rise of e-commerce, as did the rest of retail, but the company appears to have returned to sustained growth.

Overall, we feel that Target’s current valuation is slightly elevated, but the company’s strong EPS growth justifies a higher valuation. We rate the stock as a hold.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It comprises 54 stocks with 50+ years of consecutive dividend increases.

- The 20 Highest Yielding Dividend Kings

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: