Updated on Febuaury 4th, 2026 by Felix Martinez

At Sure Dividend, we believe the best stocks to buy and hold for long-term wealth share several qualities. First, they are strong businesses that lead their respective industries and generate consistent profits year after year—even during recessions.

Not only that, but they also have shareholder-friendly management teams that are dedicated to raising their dividends each year. We advocate investing in the Dividend Aristocrats, a group of 69 S&P 500 companies that have at least 25 consecutive years of dividend increases.

You can download the full list of all 69 Dividend Aristocrats, along with several important financial metrics such as price-to-earnings ratios and dividend yields, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Each year, we review all the Dividend Aristocrats. Next up is Archer Daniels Midland (ADM).

Archer Daniels Midland has increased its dividend every year for 51 consecutive years and has paid uninterrupted quarterly dividends to shareholders for 90 years. The company’s dividend is also relatively safe thanks to sound business fundamentals.

Business Overview

Archer Daniels Midland was founded in 1902 when George A. Archer and John W. Daniels began a linseed-crushing business. In 1923, Archer-Daniels Linseed Company acquired Midland Linseed Products Company, which created Archer Daniels Midland.

Today, it is an agricultural-industry giant with annual revenue exceeding $86 billion. The company produces a wide range of products and services to meet growing demand for food as populations rise.

Archer-Daniels-Midland’s businesses include processing cereal grains and oilseeds, as well as agricultural storage and transportation. The Ag Services and Oilseeds segment is Archer Daniels Midland’s largest.

Source: Investor Presentation

Archer-Daniels-Midland reported its fourth-quarter Fiscal Year (FY) 2025 results on February 4rd, 2026. The company reported a mixed fourth quarter and full-year 2025, reflecting a challenging operating environment marked by weaker global trade flows and ongoing uncertainty around U.S. biofuel policy. Fourth-quarter adjusted EPS came in at $0.87, down 24% year over year, as segment operating profit fell 22% to $821 million. Results were pressured primarily by significantly lower crush margins and reduced soybean export activity in Ag Services & Oilseeds, partially offset by resilience in Carbohydrate Solutions and continued improvement in Nutrition.

For full-year 2025, ADM reported adjusted EPS of $3.43, down 28% from the prior year, with total segment operating profit declining 23% to $3.2 billion. Despite weaker earnings, the company generated a strong operating cash flow of $5.5 billion, advanced cost-reduction and portfolio optimization initiatives, and improved plant efficiency. Nutrition was a relative bright spot, delivering 8% operating profit growth for the year, supported by strength in flavors and improved margins in animal nutrition.

Looking ahead, ADM provided constructive guidance for 2026, forecasting adjusted EPS in a range of $3.60 to $4.25. Management expects improving global trade dynamics and greater clarity on U.S. biofuel policy to support earnings recovery, with upside driven by crush margin expansion, operational efficiencies, and stronger customer demand. Backed by solid cash generation, ADM also increased its quarterly dividend for the 53rd consecutive year, reinforcing its commitment to shareholder returns despite near-term volatility.

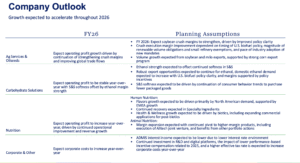

Growth Prospects

ADM’s growth prospects hinge on improving global trade conditions, recovery in ag margins, and tighter cost control. A rebound in exports and more stable biofuel policies should support earnings in its core Ag Services & Oilseeds business.

Over the long term, growth will be driven by higher-margin Nutrition products, rising global protein demand, and strong cash flow that enables continued investment and shareholder returns.

Source: Investor Presentation

Competitive Advantages & Recession Performance

Archer Daniels Midland has built significant competitive advantages over the years. It is the world’s largest corn processor, which drives economies of scale and production and distribution efficiencies.

It is an industry giant with ~440 crop procurement locations, ~300 food and feed processing facilities, and 64 innovation centers.

At its innovation centers, the company conducts research and development to respond more effectively to changes in customer demand and improve processing efficiency. Archer Daniels Midland’s unparalleled global transportation network is a significant competitive advantage.

The company’s global distribution system provides high margins and barriers to entry, allowing Archer Daniels Midland to remain highly profitable even during industry downturns.

Profits held up, even during the Great Recession. Earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $2.38

- 2008 earnings-per-share of $2.84 (19% increase)

- 2009 earnings-per-share of $3.06 (7.7% increase)

- 2010 earnings-per-share of $3.06

Archer Daniels Midland’s earnings per share increased in 2008 and 2009, during the Great Recession. Very few companies can boast such a performance in one of the worst economic downturns in U.S. history.

Archer Daniels Midland’s remarkable durability in recessions may stem from the fact that grains still need to be processed and transported, regardless of the economic climate.

There will always be a certain level of demand for Archer Daniels Midland’s products. From a dividend perspective, the payout looks quite safe.

Valuation & Expected Returns

Based on the expected 2026 EPS of $4.20, ADM shares trade for a price-to-earnings ratio of 16. Archer–Daniels–Midland has been valued at a price-to-earnings multiple of ~15 over the last decade.

Our fair value P/E is 14, meaning the stock is overvalued.

An increasing valuation multiple could compress returns by -2% annual returns for shareholders over the next five years. Future returns will also be derived from earnings growth and dividends.

We expect Archer Daniels Midland to grow its earnings by ~4% per year through 2031, and the stock currently offers a 3.1% dividend yield.

In this case, total expected returns are 5.1% per year over the next five years, a poor risk-adjusted rate of return for Archer Daniels Midland stock.

Final Thoughts

Archer Daniels Midland is coming off a few years of strong earnings growth. While earnings are expected to decline in 2024, we see the potential for a return to long-term growth.

The company has a long history of navigating challenging periods. It has continued to generate profits and reward shareholders with rising dividends.

The stock appears overvalued, with a 3.1% dividend yield and annual dividend increases. As a result, Archer Daniels Midland seems to be a hold for dividend growth investors.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 54 stocks with 50+ years of consecutive dividend increases.

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: