Updated on March 22nd, 2026 by Nathan Parsh

The Dividend Aristocrats are a group of 69 companies in the S&P 500 Index that have increased their dividends for 25+ consecutive years.

Within the Dividend Aristocrats are various types of stocks with differing yields. Some of the Dividend Aristocrats have higher yields, but these high-yielders tend to grow their dividends at a lower rate each year.

At the same time, there are Dividend Aristocrats with low yields. While these may look unappealing on the surface, they often provide higher dividend growth levels from year to year. An example is Brown-Forman (BF.B), a Dividend Aristocrat that has increased its dividend for 42 consecutive years.

There are currently 69 Dividend Aristocrats, including Brown-Forman. You can download an Excel spreadsheet of all 69 Dividend Aristocrats (with metrics like dividend yields and price-to-earnings ratios) by clicking the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Brown-Forman has paid a dividend for 82 years. Thanks to its defensive business model, the company typically provides high dividend increases each year, even during recessions. Growth has slowed in recent years, but the dividend growth streak is very impressive.

This article will discuss Brown-Forman’s growth prospects, valuation, and outlook.

Business Overview

Jack Daniel’s Tennessee Whiskey got its start all the way back in 1865 when Jack Daniel purchased Cave Spring Hollow. The following year, he registered the Jack Daniel Distillery, which is today America’s oldest registered distillery.

Brown-Forman has a large product portfolio focused on whiskey, vodka, and tequila. Its most famous brand is its flagship, Jack Daniel’s whiskey. Other popular brands include Herradura and El Jimador tequila.

On March 4th, 2026, Brown-Forman released results for the third quarter of 2026.

Source: Investor Presentation

Revenue for the quarter declined 1.9% to $1.04 billion, but did beat analysts’ estimates by $40 million. Organic sales grew 1% for the period. GAAP earnings-per-share of $0.58 compared to $0.57 in the prior year and topped expectations by $0.11.

For the first nine month of fiscal 2026, revenue declined 2% to $3 billion, though organic growth was flat. GAAP earnings-per-share of $1.41 was down from $1.53 in the comparable period of the prior fiscal year.

The sales decline for the first nine month of the year was driven by the end of the Korbel Champagne Cellars relationship and the absence of the Sonoma-Curter prior-year transition services agreement. Whiskey sales remained stable due to 10% growth for Woodford Reserve and a 12% increase for Old Forester, but Tequila fell 15% and ready-to-drink products was lower by 31%.

U.S. net sales fell 5% due to weaker Jack Daniel’s demand and the end of the Korbel agreement. Developed international markets were down 2%, but Emerging markets improved 16%.

Gross profit declined 1%, but gross margins expanded 50 basis points to 59.9% due to acquisitions and divestitures and favorable currency translation. These gains were offset by higher costs and unfavorable price and mix.

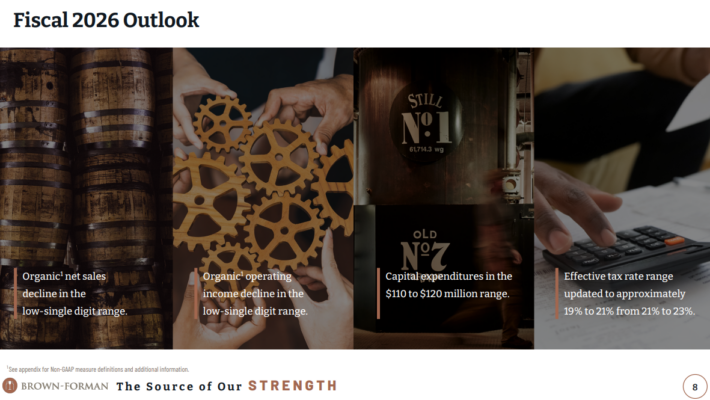

Brown-Forman increased its quarterly dividend 2% to $0.231, marking the company’s 42nd consecutive year of raising its distribution. The company expects organic growth to decline in the low single-digit range and earnings-per-share are projected to decrease as well.

Growth Prospects

Brown-Forman has a strong growth track record; the company even increased its earnings-per-share during the last financial crisis, as demand for alcohol is not especially cyclical. Historical earnings-per-share were driven by a combination of several factors, including revenue growth, rising margins, and the impact of a declining share count.

Because Brown-Forman owns strong brands and is active in the super and ultra-premium alcoholic beverages markets, which see consistent market growth, Brown-Forman should be able to keep its revenue growth going forward.

This has been an important growth factor for Brown-Forman in the past. Brown-Forman’s Jack Daniels brand and its American super-premium whiskeys continue to grow around the globe.

Higher overall sales allow for margin increases due to better economies of scale, which makes the company more efficient overall, and positively impacts its net earnings growth rate.

In addition, Brown-Forman has aggressively repurchased shares in the past decade, which adds some additional growth to its bottom line. Going forward, there is plenty of growth potential left as the company further expands its product line inside and outside its flagship Jack Daniels brand.

Furthermore, the company will purchase growth through acquisitions, for example, its recent purchase of the Diplomático Rum brand. This purchase launched Brown-Forman into the growing super-premium+ rum category. Diplomático Rum is a super-premium rum from Venezuela and is distributed in over 100 countries.

Source: Investor Presentation

We are forecasting 5% annual earnings-per-share growth off expected earnings-per-share of $1.65 for fiscal year 2026 over the next five years.

Competitive Advantages & Recession Performance

Brown-Forman has many competitive advantages. Its famous brands yield significant pricing power. Because of its global scale, it has a highly profitable business with low manufacturing and distribution costs. These qualities help Brown-Forman generate consistently high returns on invested capital.

Brown-Forman is also very resistant to recessions. This is typical among alcohol stocks, as their products tend to be consumed in greater volume when economic times are tough. One could argue that alcohol manufacturers perform well during recessions.

Brown-Forman’s earnings-per-share through the Great Recession are shown below:

- 2007 earnings-per-share of $0.76

- 2008 earnings-per-share of $0.77 (1.3% increase)

- 2009 earnings-per-share of $0.82 (6.5% increase)

- 2010 earnings-per-share of $0.95 (15.9% increase)

As you can see, the company grew its earnings per share every year through the Great Recession. This rare accomplishment demonstrates the company’s defensive business model.

Spirits manufacturers such as Brown-Forman are among the most recession-resistant businesses.

Valuation & Expected Returns

Based on our estimate for 2026 earnings-per-share of $1.65 and a current share price near $23, Brown-Forman shares are currently trading at a P/E ratio 13.9.

Considering the strength of Brown-Forman’s business, we have a target P/E of 20. Shares of the company are well below our target, making the stock undervalued today.

If shares were to increase to 20 times earnings by fiscal year 2031, this implies the potential for a 7.5% valuation tailwind over the next five years.

Brown-Forman offers an unusually high dividend yield of 4.0% today, which appears to be safe as the expected payout ratio for fiscal year 2026 is 56%.

Add in our forecasted earnings growth rate of 5%, and total returns could be 15.5% annually over the next five years.

Final Thoughts

Brown-Forman has a dominant position in its core product categories. Its flagship Jack Daniel’s brand should continue to lead the whiskey industry, with high growth from its smaller whiskey brands and tequilas. Emerging markets are also an appealing growth catalyst, and of course, the dividend growth streak is enviable.

Brown-Forman is a good example of a great business trading at an exceptionally fair valuation. The company has a solid dividend and very strong business, the shares look particularly compelling for purchase right now. We now rate shares of Brown-Forman as a buy due to projected returns.

Related: My Top 10 Buy & Hold Forever Stocks.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: