Updated on July 8th, 2025 by Nathan Parsh

The Dividend Kings comprise companies that have increased their dividends for at least 50 consecutive years. Due to their unparalleled streak of annual dividend increases, it is common to view the Dividend Kings as among the best dividend growth stocks in the market.

You can see the full list of all 55 Dividend Kings here.

We also compiled a comprehensive list of all Dividend Kings, along with relevant financial statistics such as dividend yields and price-to-earnings ratios. You can download the full list of Dividend Kings by clicking on the link below:

Consolidated Edison (ED) is one of the more recent additions to the Dividend Kings, having raised its dividend for 51 consecutive years.

Over the years, utilities have become relied upon for their steady dividend payouts, even during recessions. This article will analyze the company’s business overview, future growth prospects, competitive advantages, and other key aspects.

Business Overview

Consolidated Edison is a large-cap utility stock. The company generates more than $15 billion in annual revenue and has a market capitalization of approximately $36 billion.

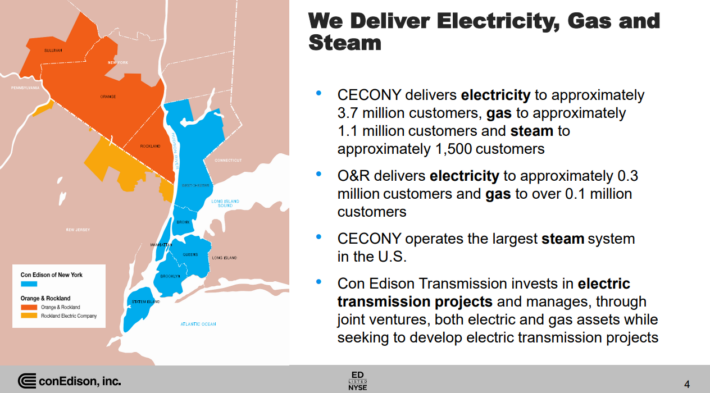

The company serves approximately 3.7 million electric customers and an additional 1.1 million gas customers in New York.

Source: Investor Presentation

It operates electric, gas, and steam transmission businesses, with a steam system that is the largest in the U.S.

On October 1st, 2022, Consolidated Edison announced that it was selling its interest in its renewable energy business to RWE Renewables Americas, LLC for $6.8 billion. The transaction closed in 2023. As a result of this transaction, Consolidated Edison has not issued common stock in each of the last two years. The company had typically issued shares for financing on a regular basis in the past.

On May 2nd, 2025, Consolidated Edison announced first-quarter results for the period ending March 31st, 2025. During the quarter, revenue increased 12.1% to $4.8 billion, representing $346 million more than expected.

Adjusted earnings of $792 million, or $2.26 per share, compared favorably to adjusted earnings of $742 million, or $2.15 per share, in the previous year. Adjusted earnings per share exceeded the analysts’ estimates by $0.07.

As with prior periods, higher rate bases for gas and electric customers were the primary contributors to results in the CECONY business, which accounts for the vast majority of the company’s assets.

Average rate base balances are expected to grow at an average annual rate of 8.2% between 2025 and 2029, up from 6.4% previously. Consolidated Edison expects capital investments of nearly $38 billion during the period 2025 to 2029.

On its latest conference call, Consolidated Edison reaffirmed its guidance for 2025. The company expects adjusted earnings per share in a range of $5.50 to $5.70 for the year. At the midpoint, the guidance implies 3.7% growth over 2024.

Growth Prospects

Earnings growth across the utility industry typically mimics GDP growth. Over the next five years, we expect Consolidated Edison to grow its earnings per share by 6.0% annually.

The company has guided for an average annual earnings per share growth of 5% to 7% from 2025 levels through 2029. We believe this growth is achievable, given that share issuances appear to have stopped, coupled with the company’s guidance towards higher-than-expected rate balances. We note that this expected earnings growth rate is above the long-term average rate of 3.2%.

ConEd should generate solid earnings growth each year through a combination of new customer acquisitions and rate increases, helped by the gradual improvement of the U.S. economy.

The growth drivers for Consolidated Edison are new customers and rate increases. One benefit of operating in a regulated industry is that utilities are permitted to raise rates on a regular basis, which virtually assures a steady level of growth.

Source: Investor Presentation

Consolidated Edison anticipates growing its rate base by more than 8% annually on average through 2029. This is a natural way for a utility to generate steady revenue and earnings growth.

One potential threat to future growth is high interest rates, which could increase the cost of capital for companies that utilize debt, such as utilities.

The Fed has largely maintained interest rates where they are, following decreases, which means companies with heavy debt loads are paying less to finance their capital needs.

Lower interest rates help companies that rely heavily on debt financing, such as utilities, so investors do not need to be concerned about Consolidated Edison in a falling-rate cycle.

Even if rates remain elevated, Consolidated Edison is in strong financial condition. It has an investment-grade credit rating of A-, and a modest capital structure with balanced debt maturities over the next several years.

A healthy balance sheet and strong business model help provide security for Consolidated Edison’s dividends.

Investors can reasonably expect low single-digit dividend increases each year, at a rate similar to the company’s annual adjusted earnings-per-share growth.

Competitive Advantages & Recession Performance

Consolidated Edison’s main competitive advantage is the high regulatory hurdles of the utility industry. Electricity and gas services are necessary and vital to society.

As a result, the industry is highly regulated, making it virtually impossible for a new competitor to enter the market. This provides a great deal of certainty to Consolidated Edison.

In addition, the utility business model is highly recession-resistant. While many companies experienced significant earnings declines in 2008 and 2009, Consolidated Edison performed relatively well. Earnings per share during the Great Recession are shown below:

- 2007 earnings-per-share of $3.48

- 2008 earnings-per-share of $3.36 (3% decline)

- 2009 earnings-per-share of $3.14 (7% decline)

- 2010 earnings-per-share of $3.47 (11% increase)

Consolidated Edison’s earnings fell in 2008 and 2009 but recovered in 2010. The company still generated healthy profits, even during the worst of the economic downturn.

This resilience allowed Consolidated Edison to continue raising its dividend each year.

The same pattern held up in 2020 when the U.S. economy entered a recession due to the coronavirus pandemic. ConEd has remained highly profitable, with record earnings per share in each of the last three years, which has enabled the company to raise its dividend annually.

Valuation & Expected Returns

Using the current share price of approximately $100 and the midpoint of 2025 guidance, the stock trades at a price-to-earnings ratio of 17.9. This is nearly in line with our fair value estimate of 18.0, which is below the long-term average P/E of 18.5.

As a result, Consolidated Edison shares appear to be fairly valued. If the stock valuation reaches our fair value estimate, the corresponding multiple expansion would add 0.2 percentage points to annual returns over the next five years.

Fortunately, the stock can still provide positive returns to shareholders through earnings growth and dividend payments. We expect the company to grow its earnings per share by 6.0% annually over the next five years.

Additionally, the stock boasts a current dividend yield of 3.4%. Utilities like ConEd are prized for their stable dividends and safe payouts.

Putting it all together, Consolidated Edison’s total expected returns could reach 8.9% through 2029. This is a solid rate of return, but not high enough to warrant a buy recommendation at the moment.

Income investors may find the yield attractive, as the current yield is meaningfully higher than the 1.25% yield of the S&P 500 Index and grows very consistently. The company has a projected payout ratio of 61%, which is one of the lowest payout ratios for ConEd in the last decade, indicating a sustainable dividend. However, dividend growth has been on the low side, averaging just above 2% over both the long and medium terms.

Nevertheless, we rate the stock a hold at the current projected rate of return.

Final Thoughts

Consolidated Edison can be a valuable holding for income investors, such as retirees, thanks to its 3.4% dividend yield. The stock offers secure dividend income and is also a Dividend King, meaning it is expected to raise its dividend each year.

Therefore, risk-averse investors looking primarily for income right now–such as retirees–could see greater value in buying utility stocks like Consolidated Edison. However, we rate the stock as a hold due to projected returns.

Additional Reading

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

- The Dividend Achievers List is comprised of ~400 stocks with 10+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Best DRIP Stocks: The top 15 Dividend Champions with no-fee dividend reinvestment plans.

- The Complete List of Russell 2000 Stocks

- The Complete List of NASDAQ-100 Stocks