Updated on April 30th, 2026 by Josh Arnold

International REITs could be valuable for investors interested in diversifying their portfolios. Many international Real Estate Investment Trusts (REITs) are based outside the U.S. and have quality business models and high dividend yields.

One example is Granite Real Estate Investment Trust (GRTUF), a Canadian REIT. Granite has a proven business model and pays a 5.6% dividend yield, which is about four times the level of the S&P 500.

Granite also pays its dividends monthly, which is a more attractive dividend schedule than REITs, which pay quarterly dividends.

Granite is one of 119 stocks that pay monthly dividends. You can access the full database of monthly dividend stocks (along with important financial metrics such as price-to-earnings ratios and dividend yields) by clicking on the link below:

Granite is listed in Toronto and New York, but for this article, we’ll use the New York listing under ticker GRTUF, and US dollars.

This article will outline Granite’s business model and discuss its merits as a dividend stock.

Business Overview

Granite owns and manages predominantly industrial real estate properties in North America and Europe. It converted to a REIT on January 3, 2013, and has transformed into a leaner, more efficient trust, with higher-quality assets.

Source: Investor presentation

Over time, Granite has grown from a smaller, less valuable portfolio that was almost entirely dependent upon one tenant (Magna), to a diversified, much larger portfolio with significantly higher average property values. The trust has undergone a transformation in recent years to reach these goals, and it is clear that the effort has paid off.

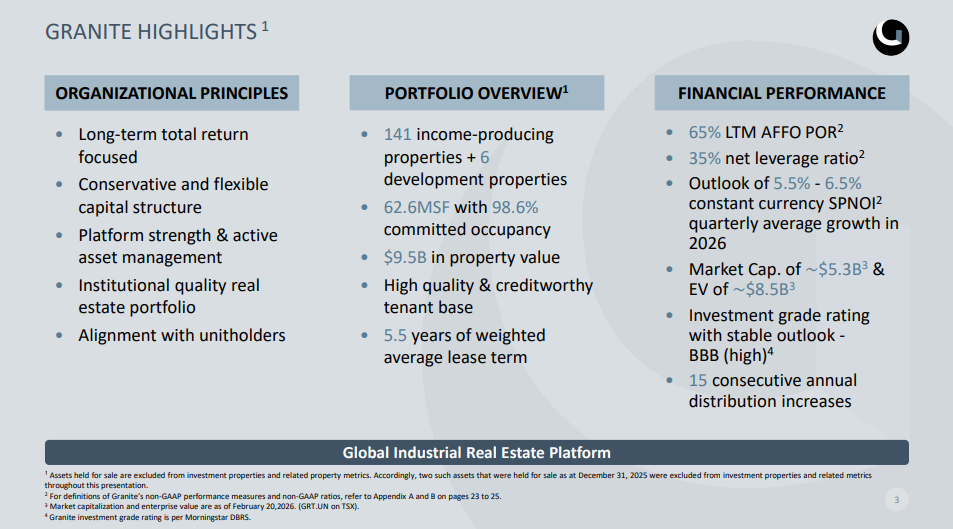

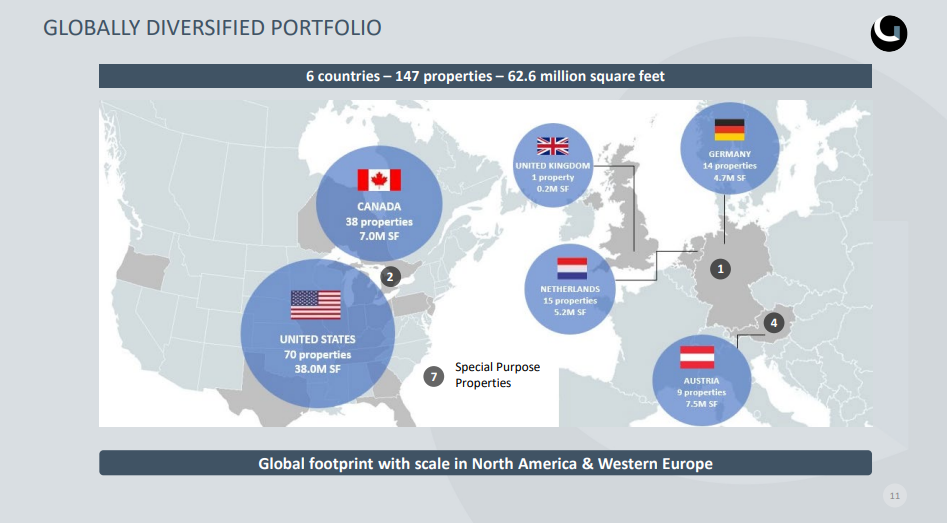

The trust’s income-producing portfolio consists of Multi-Purpose, Logistics and Distribution Warehouses, and Special-Purpose facilities. It owns a total of 62.6 million square feet spread across 147 properties in Europe, Canada, and the U.S. Combined, these properties have a carrying value of about $9.5 billion.

Source: Investor presentation

Granite is present only in countries with little or no geopolitical risk and in properties and industries with strong long-term fundamentals. It is still heavily concentrated in the US and Canada, with a little more than two-thirds of its property’s square footage in North America.

Still, its international exposure provides a diversifying component to the trust’s results. Granite focuses on properties that support e-commerce development and are located strategically to support such businesses in the best markets.

![]()

Source: Investor presentation

Granite seeks out areas that have proximity to major cities and have favorable demographics, including significant infrastructure and available labor pools. In addition, it already owns modern properties, meaning capital expenditure needs are low, with tenants with high switching costs.

These characteristics mean that Granite chooses only the most favorable properties to own, with long-term tenants who have the best chance of thriving in various economic climates. Finally, it focuses on the enormous shift to e-commerce, particularly on food and pharmaceuticals.

Granite reported fourth quarter and full-year earnings on February 25th, 2026, and results were pretty good. Revenue for the year was $452 million, up from $415 million in 2024. The rise in revenue was driven primarily by contractual rent adjustments, new leases and renewals, and contributions from acquisitions.

Overall occupancy was 98%, up from 94.9% a year earlier, which was due to strong demand for the trust’s logistics markets. FFO-per-unit came to $4.31 for the year, up strongly from $3.78 in 2024. This was driven by the gain from higher rental income, same-property net operating income margin growth, and favorable forex translation. These were partially offset by higher operating costs and capex. We expect $4.58 per share in FFO for 2026.

Growth Prospects

Granite’s outlook is positive from a fundamental perspective, with the trust in the midst of a transformation. Granite is in the final stages of its years-long transformation in which it is optimizing its cost of capital, leverage on the balance sheet, and reaching what it considers a saturation point in critical target markets.

In recent years, the trust has experienced significant transition, switching out its CEO, board, and leadership team. Today, the trust is focused on transforming its portfolio through the sale of non-core assets, enhancing its presence in the U.S., and making purchases in select European markets. The trust is not expanding its portfolio today, as it is actually slightly smaller than it was a year ago. However, the value of the portfolio has grown significantly, and the mix is more favorable for longer-term growth.

Granite appears to have achieved its growth goals earlier than expected, and as a result, we expect incremental investment to slow somewhat in the coming years. A development pipeline is still in progress, with some properties in Europe and North America. However, Granite’s transformative moves have largely been completed.

Granite’s growth outlook is favorable, given that it should continue to see higher rent prices and a larger investment book through acquisitions and development. We’re looking for 3% annual growth going forward.

Dividend Analysis

Granite currently pays a monthly dividend of $0.2958 per share in Canadian dollars, which equates to ~$0.22 monthly in US dollars.

On an annualized basis, the current regular dividend payment is $3.55 per share in Canadian currency. In U.S. dollars, this works out to roughly $2.64 per share. This equates to a 3.9% yield.

If U.S. investors own the stock, returns will be subject to currency risk as it is translated from Canadian dollars to U.S. dollars. The dividend to U.S. investors will depend in part upon prevailing exchange rates, which currently stand at $1 CAD = $0.73 USD. Another important consideration for investing in international stocks is withholding taxes.

Note: As a Canadian stock, a 15% dividend tax will be imposed on US investors investing in the company outside of a retirement account. See our guide on Canadian taxes for US investors here.

Granite’s 3.9% dividend yield is supported by underlying cash flow. Based on the adjusted FFO for 2026, Granite’s payout ratio is 56%. That is meaningfully below previous years and considered very safe in the REIT universe where payout ratios tend to be quite high.

We believe Granite will grow FFO in the coming years, so in conjunction with the current fair payout ratio, we see the distribution as safe.

Final Thoughts

Investors can receive high levels of income and diversification benefits by considering REITs based outside the United States. Granite REIT is a good example of an international REIT with a high-quality business model, and a fair dividend yield of 3.9%.

The trust has largely completed its transformation effort, which diversified its portfolio, reduced risk, and enhanced its earnings growth prospects. As the payout ratio has been reduced significantly, we see this as supportive of future dividend increases. As a result, Granite remains an attractive option for investors looking for monthly dividends and a ~4% dividend yield.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more