Updated on February 24th, 2026 by Felix Martinez

The Dividend Aristocrats are 69 S&P 500 stocks that have achieved at least 25 consecutive years of dividend increases.

The Dividend Aristocrats are among the highest-quality dividend growth stocks in the entire stock market. For this reason, we individually review every Dividend Aristocrat each year.

You can download your full list of all 69 Dividend Aristocrats (along with important financial metrics like price-to-earnings ratios and dividend yields) by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

The next installment of the 2025 series takes a closer look at Linde plc (LIN), which qualifies on the list as a result of its acquisition of Praxair, a former Dividend Aristocrat.

The Praxair acquisition should be a meaningful growth catalyst for many years to come. As a result, we view Linde favorably as a dividend growth stock, albeit one with an elevated valuation.

Business Overview

Linde plc – which was created through the merger of Linde AG and Praxair – is the world’s largest industrial gas corporation. Linde AG is headquartered in the U.K. following the merger. The company produces, sells, and distributes atmospheric, process, and specialty gases, as well as high-performance surface coatings.

Linde products and services can be found in nearly every industry in more than 100 countries worldwide. The combined company now generates over $34 billion of annual revenue.

Source: Investor Presentation

The company operates in five segments: Americas, EMEA, APAC, Engineering, and Global Other. Linde gases are used in a variety of industries, including energy, steel production, chemical processing, environmental protection, food processing, electronics, and more. The company also has a healthcare business consisting of medical gases and services.

Linde’s exposure to any particular geographical area has been improved thanks to the merger, as it now has a strong, global customer base across various industries. Indeed, Linde now serves customers in more than 100 countries worldwide.

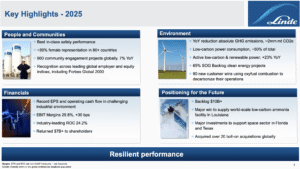

Linde plc released its Q4 and full-year results for 2025. The company delivered strong full-year 2025 results, highlighting the resilience of its industrial gas business model. Revenue increased 3% year over year to $34.0 billion, while adjusted operating profit rose 4% to $10.1 billion, with margins expanding to an industry-leading 29.8%. Adjusted EPS grew 6% to $16.46, supported by pricing gains, productivity initiatives, and stable volumes.

The company generated $10.4 billion in operating cash flow and returned $7.4 billion to shareholders through dividends and share repurchases, while maintaining a $10.0 billion project backlog that provides visibility into future growth.

Fourth-quarter performance remained solid, with revenue rising 6% to $8.8 billion and adjusted EPS increasing 6% to $4.20, exceeding expectations. Adjusted operating profit reached $2.6 billion, driven by higher pricing and continued efficiency improvements across regions.

Free cash flow totaled $1.6 billion after capital expenditures, allowing Linde to return over $2.0 billion to shareholders during the quarter. Growth was led by project start-ups and strength in electronics, chemicals, and energy end markets, particularly in the Americas and Asia-Pacific segments.

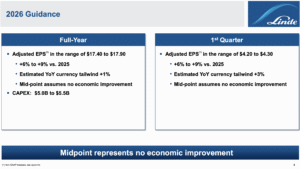

Looking ahead, Linde expects continued earnings expansion, guiding 2026 adjusted EPS of $17.40–$17.90, representing 6%–9% year-over-year growth. Management plans $5.0–$5.5 billion in capital expenditures to support its contractual gas project pipeline, while disciplined capital allocation and high-margin long-term contracts position the company to generate consistent cash flow and shareholder returns despite macroeconomic uncertainty.

Growth Prospects

The merger between Praxair and Linde AG, which led to the creation of Linde plc, has impacted the combined company’s results and outlook.

Linde ended 2025 with a sizable backlog of potential future projects.

The merger has opened new avenues for growth, including clean energy and decarbonization projects.

Source: Investor Presentation

Linde plc can generate substantial cost savings through synergies between the two companies. Executives have touted synergies and potential annual cost savings of more than $1 billion.

It seems likely that Linde plc will grow its earnings-per-share at a mid-single-digit rate over the long term, slightly faster than Praxair’s earnings-per-share growth rate over the last decade, driven by synergies.

Linde plc recently upped its stock buyback program to $10 billion, which should drive further share count declines.

We expect Linde’s earnings per share to grow by 6% per year over the next five years. We see revenue growth as modest, with a small tailwind from margin growth and a lower share count.

Competitive Advantages & Recession Performance

Linde enjoys multiple competitive advantages. As a leader in industrial gases, the company enjoys economic scale and greater operational efficiency than its smaller competitors.

In addition, Linde’s financial resources enable it to invest heavily in research and development. Linde spent about $143 million on R&D in 2022 to build and maintain its competitive advantages.

Another competitive advantage is Linde’s strong financial position. The company has a healthy balance sheet, with high credit ratings of ‘A2’ from Moody’s and ‘A’ from Standard & Poor’s. Given that total liabilities have fallen since the merger was completed, we expect these credit ratings to be stable.

Maintaining investment-grade credit ratings helps the company access capital markets at an attractive cost, allowing Linde to allocate its cash to dividends and buybacks.

On the other hand, Linde is not a recession-resistant business. As a global industrial manufacturer, its business model is sensitive to fluctuations in the global economy. An economic downturn typically sees lower demand from industrial customers.

Linde’s earnings-per-share during the Great Recession are as follows:

• 2008 earnings-per-share of $4.19

• 2009 earnings-per-share of $4.01 (4.3% decline)

• 2010 earnings-per-share of $3.84 (4.2% decline)

• 2011 earnings-per-share of $5.45 (42% increase)

The company saw a modest decline in earnings per share during the recession, but its earnings improved alongside the broader global economic recovery.

By 2011, Linde’s earnings had surpassed 2008 levels. We expect Linde’s revenue and margins to suffer during the next recession, but note that its current growth outlook is robust.

Valuation & Expected Returns

Linde is expected to generate earnings per share of $17.65 in 2026. Based on this, shares currently trade for a price-to-earnings ratio of 28.2x. This is a high valuation for the stock, even though the company is highly profitable and growing earnings at a satisfactory rate.

In addition, we see Linde as receiving a premium valuation due to its unmatched competitive position in its industry.

Our fair value estimate for the stock is a price-to-earnings ratio of 21. As a result, Linde appears to be overvalued.

If shares were to fall in valuation to our fair value estimate, it would reduce annual returns by ~5.6%. This represents a significant headwind for investors buying at the current price.

Future returns will be boosted by earnings growth and dividends. In addition to Linde’s expected earnings growth of 6% per year over the next five years, the stock has a current annualized dividend yield of 1.2%.

The combination of valuation changes, earnings growth, and dividends results in total expected returns of ~1.6% per year over the next five years. The valuation headwind will virtually offset earnings-per-share growth and the dividend yield, and we see the stock as unattractive.

Linde is a very profitable company with positive earnings and dividend growth, but the impact of its overvaluation is enough to warrant a sell recommendation at the current price.

Final Thoughts

Linde stock has performed well since the merger with Praxair. Expectations are high for the combined company’s potential, but at this time, we feel Linde’s stock is significantly overvalued.

Linde will be an industry leader with clear and durable competitive advantages. The company should grow revenue and earnings at a steady rate going forward, assuming the global economy stays out of recession.

However, while Linde is a strong business, the stock is too richly valued to buy today. While Linde should continue to raise its dividend each year, investors should wait for a significant decline in the share price before buying Linde stock.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The 20 Highest Yielding Dividend Aristocrats

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 54 stocks with 50+ years of consecutive dividend increases.

- The 20 Highest Yielding Dividend Kings

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: