Updated on June 26th, 2025 by Bob Ciura

Spreadsheet data updated daily

In the world of investing, volatility matters. Investors are reminded of this every time there is a downturn in the broader market and individual stocks that are more volatile than others experience enormous swings in price in both directions.

That volatility can increase the risk in an individual’s stock portfolio relative to the broader market.

The volatility of a security or portfolio against a benchmark – is called Beta. In short, Beta is measured via a formula that calculates the price risk of a security or portfolio against a benchmark, which is typically the broader market as measured by the S&P 500 Index.

When stock markets are rising, high-beta stocks could outperform. With that in mind, we created a list of S&P 500 stocks with the highest beta values.

You can download your free High Beta stocks list (along with relevant financial metrics such as dividend yields and price-to-earnings ratios) by clicking on the link below:

It is helpful in understanding the overall price risk level for investors during market downturns in particular.

High Beta stocks are not a sure bet during bull markets to outperform, so investors should be judicious when adding high Beta stocks to a portfolio, as the weight of the evidence suggests they are more likely to under-perform during periods of market weakness.

However, for those investors interested in adding a bit more risk to their portfolio, we’ve put together a list to help investors find the best high beta stocks.

This article will provide an overview of Beta. In addition, we will discuss how to calculate Beta, incorporating Beta into the Capital Asset Pricing Model, and provide analysis on the top 5 highest-Beta dividend stocks in our coverage database.

The table of contents below provides for easy navigation:

Table of Contents

- High Beta Stocks Versus Low Beta Stocks

- How To Calculate Beta

- Beta & The Capital Asset Pricing Model (CAPM)

- Analysis On The 5 Highest-Beta Dividend Stocks

- Final Thoughts

High Beta Stocks Versus Low Beta

Here’s how to read stock betas:

- A beta of 1.0 means the stock moves equally with the S&P 500

- A beta of 2.0 means the stock moves twice as much as the S&P 500

- A beta of 0.0 means the stocks moves don’t correlate with the S&P 500

- A beta of -1.0 means the stock moves precisely opposite the S&P 500

The higher the Beta value, the more volatility the stock or portfolio should exhibit against the benchmark. This can be beneficial for those investors that prefer to take a bit more risk in the market as stocks that are more volatile – that is, those with higher Beta values – should outperform the benchmark (in theory) during bull markets.

However, Beta works both ways and can certainly lead to larger draw-downs during periods of market weakness. Importantly, Beta simply measures the size of the moves a security makes.

Intuitively, it would make sense that high Beta stocks would outperform during bull markets. After all, these stocks should be achieving more than the benchmark’s returns given their high Beta values.

While this can be true over short periods of time – particularly the strongest parts of the bull market – the high Beta names are generally the first to be sold heavily by investors.

One potential theory for this, is that investors are able to use leverage to bid up momentum names with high Beta values and thus, on average, these stocks have lower prospective returns at any given time.

In addition, leveraged positions are among the first to be sold by investors during weak periods because of margin requirements or other financing concerns that come up during bear markets.

While high Beta names may outperform while the market is strong, as signs of weakness begin to show, high Beta names are the first to be sold and generally, much more strongly than the benchmark.

Indeed, evidence suggests that during good years for the market, high Beta names capture 138% of the market’s total returns.

In other words, if the market returned 10% in a year, high Beta names would, on average, produce 13.8% returns. However, during down years, high Beta names capture 243% of the market’s returns.

In a similar example, if the market lost 10% during a year, the group of high Beta names would have returned -24.3%. Given this relatively small outperformance during good times and vast underperformance during weak periods, it is easy to see why we prefer low Beta stocks.

Related: The S&P 500 Stocks With Negative Beta.

While low Beta stocks aren’t a vaccine against downturns in the market, it is much easier to make the case over the long run for low Beta stocks versus high Beta given how each group performs during bull and bear markets.

How To Calculate Beta

The formula to calculate a security’s Beta is fairly straightforward. The result, expressed as a number, shows the security’s tendency to move with the benchmark.

Therefore, a Beta value of 1.00 means that the security in question should move virtually in lockstep with the benchmark (as discussed briefly in the introduction of this article).

A Beta of 2.00 means moves should be twice as large in magnitude while a negative Beta means that returns in the security and benchmark are negatively correlated; these securities tend to move in the opposite direction from the benchmark.

This sort of security would be helpful to mitigate broad market weakness in one’s portfolio as negatively correlated returns would suggest the security in question would rise while the market falls.

For those investors seeking high Beta, stocks with values in excess of 1.3 would be the ones to seek out. These securities would offer investors at least 1.3X the market’s returns for any given period.

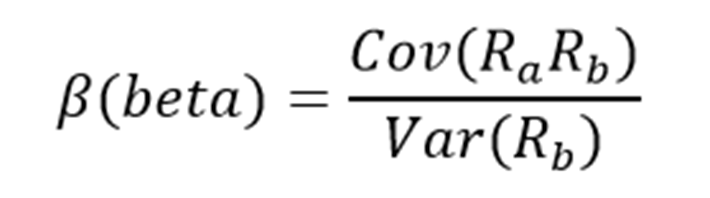

Here’s a look at the formula to compute Beta:

The numerator is the covariance of the asset in question while the denominator is the variance of the market. These complicated-sounding variables aren’t actually that difficult to compute.

Here’s an example of the data you’ll need to calculate Beta:

- Risk-free rate (typically Treasuries at least two years out)

- Your asset’s rate of return over some period (typically one year to five years)

- Your benchmark’s rate of return over the same period as the asset

To show how to use these variables to do the calculation of Beta, we’ll assume a risk-free rate of 2%, our stock’s rate of return of 14% and the benchmark’s rate of return of 8%.

You start by subtracting the risk-free rate of return from both the security in question and the benchmark. In this case, our asset’s rate of return net of the risk-free rate would be 12% (14% – 2%). The same calculation for the benchmark would yield 6% (8% – 2%).

These two numbers – 12% and 6%, respectively – are the numerator and denominator for the Beta formula. Twelve divided by six yields a value of 2.00, and that is the Beta for this hypothetical security.

On average, we’d expect an asset with this Beta value to be 200% as volatile as the benchmark.

Thinking about it another way, this asset should be about twice as volatile as the benchmark while still having its expected returns correlated in the same direction.

That is, returns would be correlated with the market’s overall direction, but would return double what the market did during the period.

This would be an example of a very high Beta stock and would offer a significantly higher risk profile than an average or low Beta stock.

Beta & The Capital Asset Pricing Model

The Capital Asset Pricing Model, or CAPM, is a common investing formula that utilizes the Beta calculation to account for the time value of money as well as the risk-adjusted returns expected for a particular asset.

Beta is an essential component of the CAPM because without it, riskier securities would appear more favorable to prospective investors. Their risk wouldn’t be accounted for in the calculation.

The CAPM formula is as follows:

The variables are defined as:

- ERi = Expected return of investment

- Rf = Risk-free rate

- βi = Beta of the investment

- ERm = Expected return of market

The risk-free rate is the same as in the Beta formula, while the Beta that you’ve already calculated is simply placed into the CAPM formula.

The expected return of the market (or benchmark) is placed into the parentheses with the market risk premium, which is also from the Beta formula. This is the expected benchmark’s return minus the risk-free rate.

To continue our example, here is how the CAPM actually works:

ER = 2% + 2.00(8% – 2%)

In this case, our security has an expected return of 14% against an expected benchmark return of 8%. In theory, this security should vastly outperform the market to the upside but keep in mind that during downturns, the security would suffer significantly larger losses than the benchmark.

If we changed the expected return of the market to -8% instead of +8%, the same equation yields expected returns for our hypothetical security of -18%.

This security would theoretically achieve stronger returns to the upside but certainly much larger losses on the downside, highlighting the risk of high Beta names during anything but strong bull markets.

While the CAPM certainly isn’t perfect, it is relatively easy to calculate and gives investors a means of comparison between two investment alternatives.

Analysis On The 5 Highest-Beta Dividend Stocks

Now, we’ll take a look at the 5 dividend stocks with the highest Beta scores (in ascending order from lowest to highest) in the Sure Analysis Research Database:

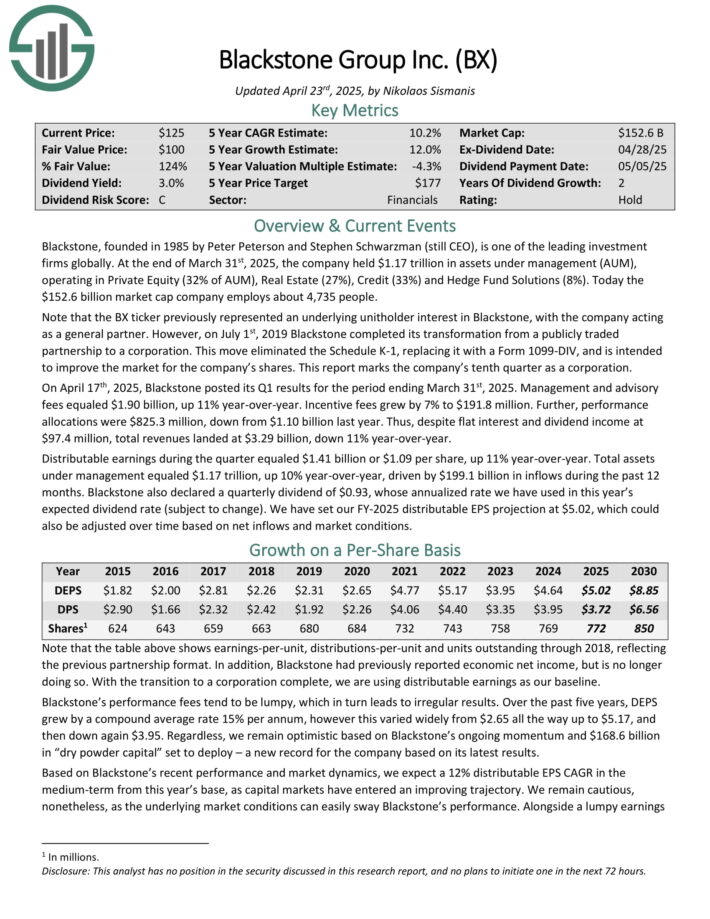

#5: Blackstone Group LP (BX)

Blackstone, founded in 1985 by Peter Peterson and Stephen Schwarzman (still CEO), is one of the leading investment firms globally.

At the end of March 31st, 2025, the company held $1.17 trillion in assets under management (AUM), operating in Private Equity (32% of AUM), Real Estate (27%), Credit (33%) and Hedge Fund Solutions (8%).

On April 17th, 2025, Blackstone posted its Q1 results for the period ending March 31st, 2025. Management and advisory fees equaled $1.90 billion, up 11% year-over-year.

Incentive fees grew by 7% to $191.8 million. Further, performance allocations were $825.3 million, down from $1.10 billion last year. Thus, despite flat interest and dividend income at $97.4 million, total revenues landed at $3.29 billion, down 11% year-over-year.

Distributable earnings during the quarter equaled $1.41 billion or $1.09 per share, up 11% year-over-year. Total assets under management equaled $1.17 trillion, up 10% year-over-year, driven by $199.1 billion in inflows during the past 12 months.

BX has a Beta value of 1.64.

Click here to download our most recent Sure Analysis report on BX (preview of page 1 of 3 shown below):

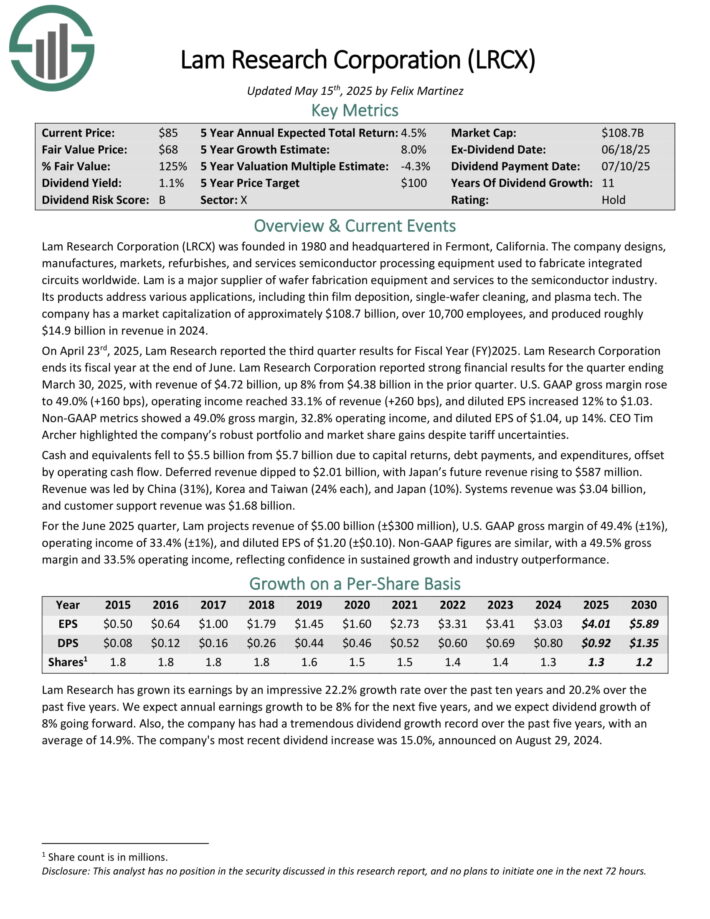

#4: Lam Research (LRCX)

Lam Research Corporation (LRCX) was founded in 1980 and headquartered in Fermont, California. The company designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used to fabricate integrated circuits worldwide.

Lam is a major supplier of wafer fabrication equipment and services to the semiconductor industry. Its products address various applications, including thin film deposition, single-wafer cleaning, and plasma tech.

The company has a market capitalization of approximately $108.7 billion, over 10,700 employees, and produced roughly $14.9 billion in revenue in 2024.

On April 23rd, 2025, Lam Research reported the third quarter results for Fiscal Year (FY)2025. Lam Research Corporation ends its fiscal year at the end of June. Lam Research Corporation reported strong financial results for the quarter ending March 30, 2025, with revenue of $4.72 billion, up 8% from $4.38 billion in the prior quarter.

U.S. GAAP gross margin rose to 49.0% (+160 bps), operating income reached 33.1% of revenue (+260 bps), and diluted EPS increased 12% to $1.03. Non-GAAP metrics showed a 49.0% gross margin, 32.8% operating income, and diluted EPS of $1.04, up 14%.

LRCX has a Beta value of 1.67.

Click here to download our most recent Sure Analysis report on LRCX (preview of page 1 of 3 shown below):

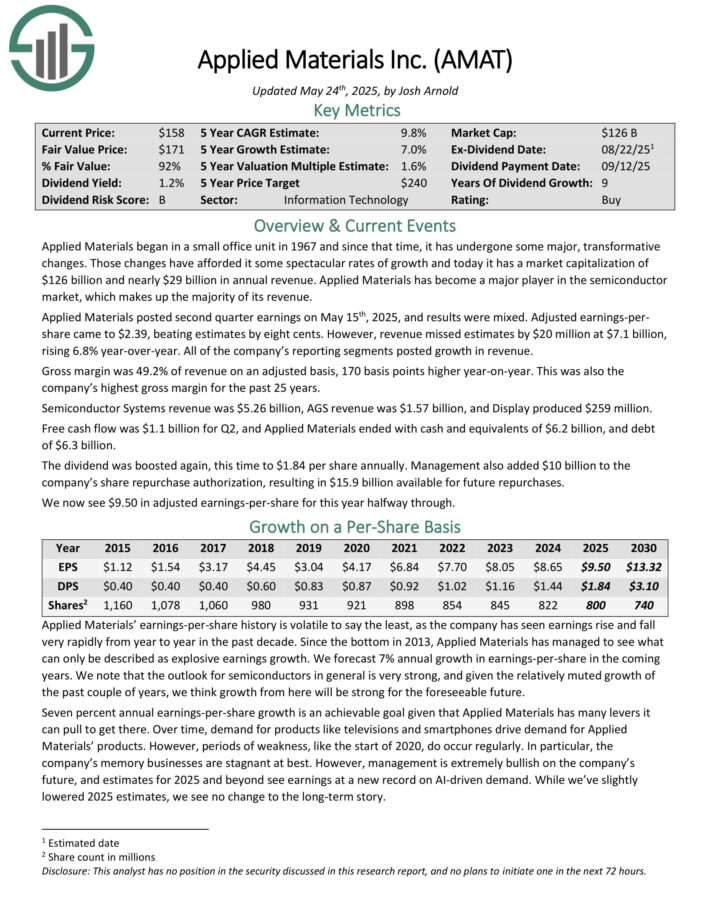

#3: Applied Materials (AMAT)

Applied Materials is a major player in the semiconductor market, which makes up the majority of its revenue.

Applied Materials posted second quarter earnings on May 15th, 2025, and results were mixed. Adjusted earnings-per share came to $2.39, beating estimates by eight cents. However, revenue missed estimates by $20 million at $7.1 billion, rising 6.8% year-over-year. All of the company’s reporting segments posted growth in revenue.

Gross margin was 49.2% of revenue on an adjusted basis, 170 basis points higher year-on-year. This was also the company’s highest gross margin for the past 25 years.

Semiconductor Systems revenue was $5.26 billion, AGS revenue was $1.57 billion, and Display produced $259 million. Free cash flow was $1.1 billion for Q2, and Applied Materials ended with cash and equivalents of $6.2 billion, and debt of $6.3 billion.

The dividend was boosted again, this time to $1.84 per share annually. Management also added $10 billion to the company’s share repurchase authorization, resulting in $15.9 billion available for future repurchases.

AMAT has a Beta value of 1.68.

Click here to download our most recent Sure Analysis report on AMAT (preview of page 1 of 3 shown below):

#2: Nucor Corp. (NUE)

Nucor is the largest publicly traded US-based steel corporation based on its market capitalization. The steel industry is notoriously cyclical, which makes Nucor’s streak of 52 consecutive years of dividend increases even more remarkable.

Nucor is a member of the Dividend Kings due to its dividend history.

On April 28, 2025, Nucor Corporation reported its financial results for the first quarter of 2025. The company posted net earnings attributable to stockholders of $156 million, or $0.67 per diluted share, a significant decrease from $845 million, or $3.46 per share, in the same quarter of the previous year.

Adjusted net earnings, excluding one-time charges related to facility closures and repurposing, were $179 million, or $0.77 per share, surpassing analyst expectations of $0.64 per share.

Net sales for the quarter were $7.83 billion, down 4% year-over-year but up 11% sequentially, driven by a 10% increase in total shipments to 6.83 million tons, despite a 12% decline in average sales price per ton compared to the first quarter of 2024.

The steel mills segment contributed $231 million in pre-tax earnings, benefiting from higher volumes and improved pricing, while the steel products segment generated $288 million, facing pressure from lower average selling prices.

NUE has a Beta value of 1.69.

Click here to download our most recent Sure Analysis report on NUE (preview of page 1 of 3 shown below):

#1: KKR & Co. (KKR)

KKR & Co is a global investment company with assets under management (AUM) of $496 billion. KKR operates on four business lines: Private markets, public markets, capital markets, and principal activities.

KKR manages private equity funds that invest capital for long-term appreciation through the Private Markets business line.

KKR & Co released Q1 2025 results on May 1st, 2025. In Q1, KKR reported fee-related earnings of $823 million, up 23% year-over-year, and total operating earnings of $1.1 billion, which was a 16% increase.

Adjusted net income reached $1.0 billion, marking a 20% rise. Fee-related earnings grew 37% to $3.4 billion for the last twelve months, while total operating earnings climbed 32% to $4.5 billion.

Adjusted net income totaled $4.4 billion, reflecting a 37% increase. KKR’s assets under management (AUM) rose 15% year-over-year to $664 billion, with fee-paying AUMs up 12% to $526 billion.

KKR has a Beta value of 1.88.

Click here to download our most recent Sure Analysis report on KKR (preview of page 1 of 3 shown below):

Final Thoughts

Investors must take risk into account when selecting prospective investments. After all, if two securities are otherwise similar in terms of expected returns but one offers a much lower Beta, the investor would do well to select the low Beta security as it would offer better risk-adjusted returns.

Using Beta can help investors determine which securities will produce more volatility than the broader market, such as the ones listed here.

The five stocks we’ve looked at offer investors high Beta scores along with very strong prospective returns.

For investors who want to take some additional risk in their portfolio, these names and others like them in our list of the 100 best high Beta stocks can help determine what to look for when selecting a high Beta stock to buy.

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

If that strategy appeals to you, it may be useful to browse through the following databases of dividend growth stocks:

- The Dividend Aristocrats List: S&P 500 dividend stocks with 25+ years of consecutive dividend increases

- The Dividend Achievers List is comprised of ~400 stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 55 stocks with 50+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.