Updated on February 13th, 2023 by Samuel Smith

The best dividend growth stocks have the ability to maintain long records of steady annual increases in their dividend payouts. This is why we focus on the Dividend Aristocrats, a group of 68 companies in the S&P 500 Index, with 25+ consecutive years of dividend increases.

You can see a full downloadable spreadsheet of all 68 Dividend Aristocrats, along with several important financial metrics such as price-to-earnings ratios, by clicking on the link below:

Once per year, we review each of the Dividend Aristocrats. The next stock in the series is industrial manufacturer 3M Company (MMM). 3M has one of the best track records in the entire market when it comes to dividend longevity. It has paid dividends for more than 100 years, and it has raised its dividend for over 60 years in a row.

This makes 3M a Dividend King, an even smaller group of companies with 50+ consecutive years of dividend increases. There are only 48 Dividend Kings, including 3M.

3M is facing a number of uncertainties, including litigation headwinds, and global supply chain disruptions and logistics challenges. Furthermore, the lingering effects of the coronavirus pandemic are continuing to weigh on major industrial manufacturers.

Business Overview

3M’s history goes all the way back to 1902, when it was a small mining venture. 3M was originally known as Minnesota Mining and Manufacturing.

Its founders started out with a simple goal: to harvest corundum from a mine called Crystal Bay. There wasn’t much corundum to be mined, but over the next 114 years, 3M became one of the biggest industrial conglomerates in the world.

Today, 3M is a large diversified global manufacturer. It manufactures ~60,000 products, which are sold in ~200 countries around the world. 3M came to dominate the industrial manufacturing industry through a sharp focus on the most attractive market segments.

It invested heavily across its core areas of focus to build a product portfolio that leads the pack. 3M is comprised of four divisions. The Safety & Industrial division produces tapes, abrasives, adhesives and supply chain management software, as well as personal protective gear and security products. The Health Care segment supplies medical and surgical products, as well as drug delivery systems.

Transportation & Electronics division produces fibers and circuits with a goal of using renewable energy sources while reducing costs. The Consumer division sells office supplies, home improvement products, protective materials and stationery supplies.

3M trades with a market capitalization of $63 billion following a sharp selloff in 2022, making it a large-cap stock.

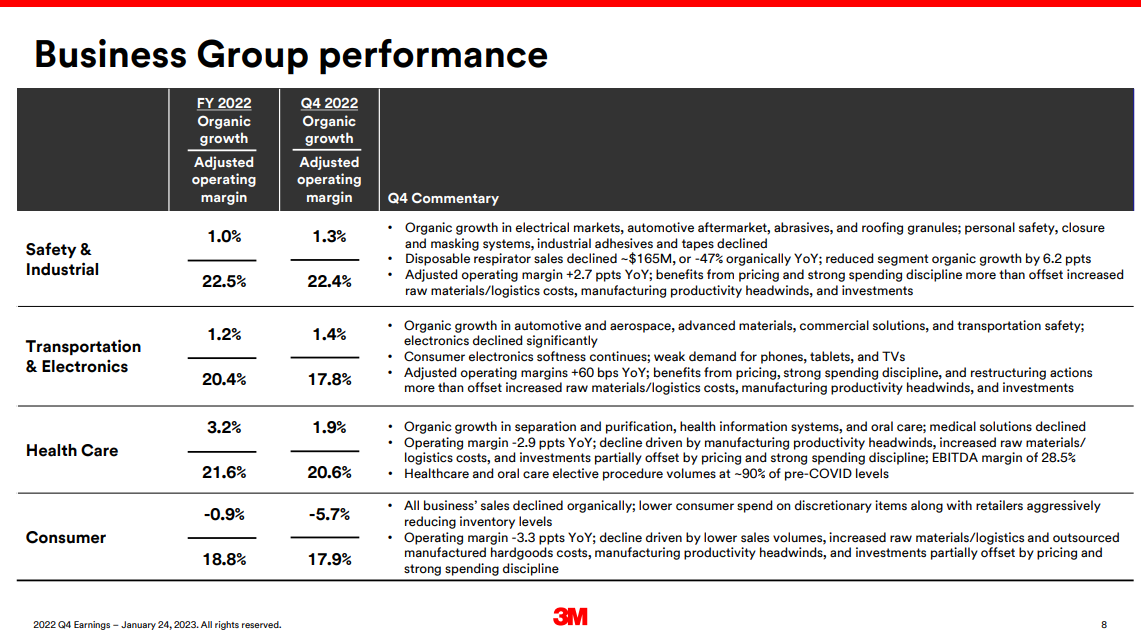

On January 24th, 2023, 3M reported earnings results for the fourth quarter and full year for the period ending December 31st, 2022. For the quarter, revenue declined 5.9% to $8.1 billion, but was $10 million more than expected. Adjusted earnings-per-share of $2.28 compared to $2.31 in the prior year and was $0.11 less than projected. For 2022, revenue decreased 3% to $34.2 billion. Adjusted earnings-per-share for the period totaled $10.10, which compared unfavorably to $10.12 in the previous year and was at the low end of the company’s guidance. Organic growth for the quarter was 1.2%. Health Care, Transportation & Electronics, and Safety & Industrial grew 1.9%, 1.4%, and 1.3%, respectively. Consumer fell 5.7%. The company will cut 2,500 manufacturing jobs.

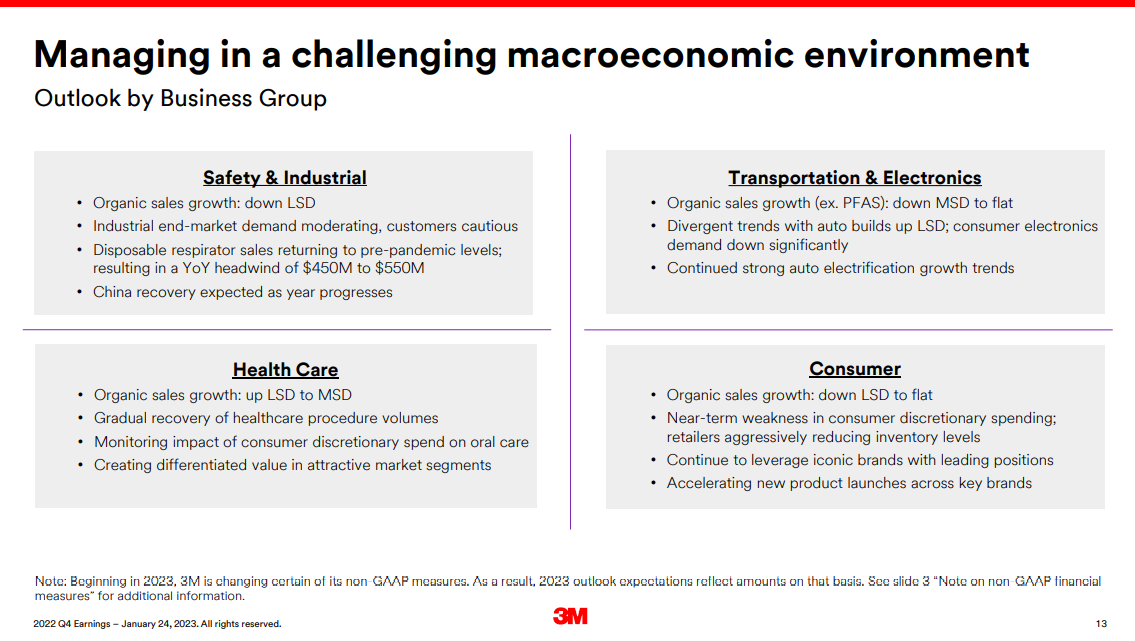

3M provided an outlook for 2023, with the company expecting adjusted earnings-per-share in a range of $8.50 to $9.00. On a comparable basis, adjusted earnings-per-share for 2022 was $9.88.

Source: Investor Presentation

We now expect $8.75 in earnings-per-share for this year after the company provided guidance.

Growth Prospects

3M has struggled to generate growth over the past few years. Still, 3M maintains a promising long-term outlook. We believe the company is capable of growing adjusted earnings-per-share by 5% per year over the next five years.

While the international markets are in decline at the moment, this is likely to be a short-term challenge. The long-term prospects for the emerging markets remain highly attractive, due to the relatively high economic growth rates in the under-developed regions of the world.

Source: Investor Presentation

3M faces challenges based on economic conditions, but given its enormous diversification, it tends to hold up nicely. We note that 3M’s highly global revenue base means it is susceptible to currency swings. When the US dollar is strong, 3M faces a headwind. It is a tailwind when the dollar is weak, however.

We see temporary headwinds for 3M from a still-struggling auto industry, but again, its diversification should help it continue to grow. Share repurchases will help a bit as well, but likely not more than 2% annually.

Competitive Advantages & Recession Performance

To raise dividends for more than 60 years requires multiple durable competitive advantages. For 3M, technology and intellectual property are its biggest competitive advantages.

3M has more than 40 technology platforms and a team of scientists dedicated to fueling innovation. Innovation has provided 3M with over 100,000 patents obtained throughout its history, which helps fend off competitive threats.

3M continues to invest heavily in research and development. The company aims to spend ~6% of annual sales on R&D. 3M R&D is so successful in creating new products that approximately 30% of annual sales come from products that didn’t exist five years ago. 3M has established itself as an industry leader, across its product segments. Competitive advantages also help 3M remain profitable, even during recessions.

3M’s earnings-per-share during the Great Recession are below:

- 2007 Earnings-per-share of $5.60

- 2008 Earnings-per-share of $4.89 (13% decline)

- 2009 Earnings-per-share of $4.52 (7.5% decline)

- 2010 Earnings-per-share of $5.75 (27% increase)

The company is not immune from recessions, and its earnings-per-share fell in 2008 and 2009. However, it bounced back in 2010. And, it remained steadily profitable throughout the recession, which allowed it to continue raising its dividend.

Indeed, 3M has a highly secure dividend payout. Based on management’s guidance, 3M is likely to have a dividend payout ratio of roughly 68% for 2023. With projected earnings growth of 5%, we see not only enhanced safety of the dividend, but also the ability for the company to continue raising the payout for many years to come.

Valuation & Expected Returns

Based on expected adjusted earnings-per-share of ~$8.75 for 2023, 3M stock has a price-to-earnings ratio of 13.1. This is lower than its average valuation. Our estimate of fair value is a price-to-earnings ratio of 17, which is a little below its 10-year historical average, but we believe it is warranted due to slowing growth and rising interest rates.

This makes the stock undervalued. Shareholders would see total annual returns improved by 5.3% per year if the stock reverted to our fair value estimate by 2028.

Owners of 3M stock should also see returns from earnings growth and dividends. 3M has experienced earnings-per-share growth of 6% to 7% over the last decade. We estimate the company will generate ~5% annual EPS growth over the next five years. Lastly, the stock has a very impressive 5.3% dividend yield.

This results in total expected returns of 15.6% through 2028. Due to the very high expected rate of return, we continue to rate the stock a buy.

Final Thoughts

3M remains a high-quality business and is likely to continue raising its dividend each year. There are very few companies that can match the company’s history of dividend growth. 3M has raised its dividend for 64 consecutive years and will likely continue to increase the dividend each year for many years to come.

Additionally, the current valuation improves total expected returns over the next five years. 3M remains a strong holding for its above-average dividend yield and annual dividend growth.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

- The 2022 High ROIC Stocks List: The top 10 stocks with high returns on invested capital.

- The 2022 High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta.

- The 2022 Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta.

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: