Updated on February 4th, 2026 by Felix Martinez

The Dividend Aristocrats are 69 S&P 500 companies with 25+ consecutive years of dividend increases. Broadly speaking, they are among the highest-quality dividend-growth investments in the stock market.

You can see a full downloadable spreadsheet of all 69 Dividend Aristocrats, along with several important financial metrics such as price-to-earnings ratios, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

This update will cover food distributor Sysco (SYY). Sysco has a long history of steady dividends and regular dividend increases. It has paid a dividend every quarter since it went public in 1970.

Sysco has many attractive qualities as a dividend growth stock. It is the largest company in its industry, which provides it with higher profit margins and durable competitive advantages over its smaller rivals.

It also has growth potential and the ability to increase its dividend each year.

Business Overview

Sysco was founded in 1969 and went public the following year. The company has grown steadily over the past five decades.

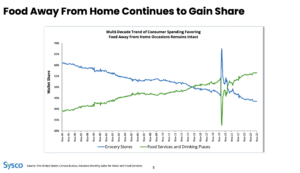

Today, Sysco is the largest food distributor in the U.S., distributing products including fresh and frozen foods, dairy, and beverages. It also provides non-food products, including tableware, cookware, restaurant and kitchen supplies, and cleaning supplies.

Source: Investor Presentation

The company serves a wide range of customers, including restaurants, healthcare facilities, education, government offices, travel, leisure, and retail businesses. It also serves a broad range of other customer types, including bakeries, churches, civic and fraternal organizations, vending distributors, and international exporters.

In all, Sysco has approximately 730,000 customers. Its position at the top of the food distribution industry gives Sysco high profit margins and strong growth potential.

Growth Prospects

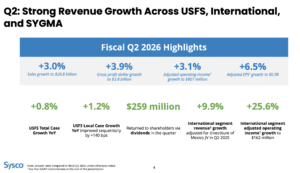

On January 27th, 2026, Sysco reported second-quarter Fiscal Year (FY) 2026 results. The company reported a solid fiscal 2026 second quarter, with revenue up 3.0% year over year to $20.8 billion and adjusted EPS rising 6.5% to $0.99. Gross profit increased 3.9% to $3.8 billion, and gross margin expanded 15 basis points to 18.3%, reflecting effective pricing, sourcing discipline, and controlled inflation impacts.

Operational trends continued to improve. U.S. Foodservice local case volume turned positive at 1.2%, marking the third straight quarter of sequential improvement, while International Foodservice remained a key driver, with sales up 7.3% and adjusted operating income jumping 25.6% on strong volume growth and margin expansion.

Sysco maintained a strong financial position, generating $611 million in operating cash flow year-to-date and returning $518 million to shareholders. Management guided full-year adjusted EPS toward the high end of the $4.50–$4.60 range, supported by improving volumes, stable margins, and continued execution across core initiatives.

Source: Investor Presentation

Competitive Advantages & Recession Performance

The U.S. food service industry is fiercely competitive. There are thousands of competitors to Sysco, including other food distributors, wholesale or retail outlets, grocery stores, and online retailers. Sysco also faces the risk of its customers negotiating directly with its suppliers.

However, what has kept competitors at bay for so many years is that Sysco is the industry’s largest operator. It controls about 16% of the U.S. food service industry. Sysco operates over 300 distribution facilities worldwide and serves over 600,000 customer locations. Such a huge presence allows Sysco to keep costs low and pass on the benefits to its customers.

Another benefit of Sysco’s business model is its resistance to recessions. Everyone has to eat, which gives Sysco a certain level of demand, regardless of the condition of the U.S. economy.

This is why Sysco’s profits held up well during the Great Recession:

- 2007 earnings-per-share of $1.60

- 2008 earnings-per-share of $1.81 (13% increase)

- 2009 earnings-per-share of $1.77 (2% decline)

- 2010 earnings-per-share of $1.99 (12% increase)

Sysco grew earnings per share at a double-digit pace in 2008 and 2010, with only a mild dip in 2009. The company grew earnings from 2007 to 2010, which was a rare achievement.

Sysco’s stable industry and strong competitive position have enabled it to raise its dividend annually, even during recessions.

Valuation & Expected Returns

We expect the company to earn $4.59 per share for FY2026. Based on this, the stock has a price-to-earnings ratio of 18.4. Our fair value estimate is a price-to-earnings ratio of 20, implying that the stock is trading below fair value.

Because Sysco is undervalued, annual returns could increase by 2% per year if the P/E multiple rises to 20 over the next five years.

Fortunately, Sysco does not need to rely on multiple expansions to deliver strong total returns, given its attractive growth profile and solid dividend. We expect Sysco to deliver up to 6% annual earnings growth going forward, consisting of organic growth, acquisitions, and share repurchases.

In addition, Sysco has a current dividend yield of 2.6%, which is higher than the S&P 500’s average yield. This yields an expected annualized return of 10.6% over the next five years. This is a strong expected rate of return, making the stock a Buy.

Sysco should have little trouble increasing its dividend going forward. The company has a projected dividend payout ratio of 47% for fiscal 2026. This indicates the dividend is more than sufficiently covered.

Final Thoughts

Sysco operates in a stable industry at the top of the market. It has an entrenched industry position and should see steady demand, even during recessions. These qualities make Sysco a reliable stock for income.

Sysco is also on the exclusive list of Dividend Kings, a group of stocks with 50+ consecutive years of dividend increases.

The stock appears undervalued, which suggests now is a good time to buy. We believe future returns will be satisfactory for investors buying the stock at the current valuation.

While returns will likely be boosted by an expanding valuation multiple, they will primarily be driven by earnings growth and dividends. As a result, we rate SYY stock a buy at the current price.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The 20 Highest Yielding Dividend Aristocrats

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 54 stocks with 50+ years of consecutive dividend increases.

- The 20 Highest Yielding Dividend Kings

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: