Updated on September 8th, 2023 by Aristofanis Papadatos

Lancaster Colony (LANC) has a dividend track record that few companies can rival. The company has increased its cash dividend for 60 consecutive years, making it one of just 13 companies in the U.S. with that long of a streak. This puts the company among the elite Dividend Kings, a small group of stocks that have increased their payouts for at least 50 consecutive years.

You can see the full list of all 50 Dividend Kings here.

We have created a full list of all Dividend Kings, along with important financial metrics such as price-to-earnings ratios and dividend yields. You can download your copy of the Dividend Kings sheet (along with financial metrics such as price-to-earnings ratios and dividend yields) by clicking on the link below:

Dividend Kings are the “best of the best” when it comes to rewarding shareholders with cash and higher dividend payouts each year. This article will discuss Lancaster’s dividend and valuation outlook.

Business Overview

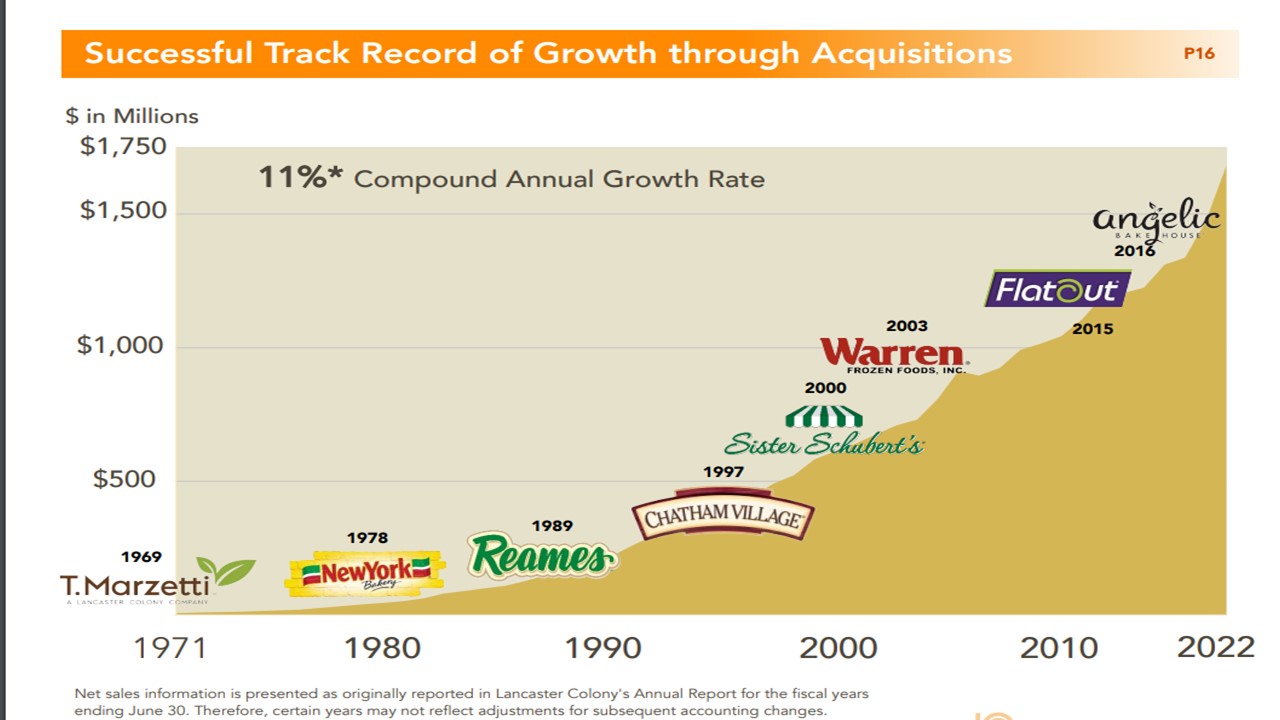

Lancaster Colony began its operations in 1961 after several small glass and related houseware manufacturing companies combined. The new company almost immediately began rewarding its shareholders with quarterly cash dividends and eventually went public in 1969, the same year it began operations in the food service business with the acquisition of the Marzetti brand.

Lancaster manufactures and distributes a fairly narrow product assortment split into two major categories: frozen and non-frozen. It makes salad dressings and various dips under the Marzetti brand, frozen breads under the Sister Schubert’s and New York brands, as well as caviar, noodles, croutons, flatbreads and other bread products under a variety of smaller brands.

The Marzetti and New York brands are cash cows for Lancaster, offering its core products of dips and dressings as well as croutons and frozen breads, respectively. Lancaster sells what amounts to accessories for meals and does it very well.

Source: Investor presentation

However, Lancaster also has partnerships with major consumer brands like Olive Garden, Jack Daniel’s, Buffalo Wild Wings, and Weight Watchers (WW), licensing the respective trademarks to produce products for grocery store shelves. A portion of the proceeds of these products goes to the license owners but these agreements are a way for Lancaster to diversify away from its own core brands.

Lancaster’s market cap is just $4.5 billion, and the company has generated $1.8 billion in revenue in the last 12 months. The vast majority of Lancaster’s sales are made in the U.S., so currency risk is not a factor. The company sells its products through the retail and food service divisions, offering its frozen and non-frozen products through those channels.

Lancaster has leadership positions in its core brands including New York, Sister Schubert’s, Flat Out (flat breads) and Marzetti, while it is more focused on growth with its smaller brands and acquisitions.

Growth Prospects

Lancaster reported fourth-quarter and full-year earnings on August 23rd, 2023, with results below expectations on both the top and bottom line. Total net sales remained grew 0.5%, from $452 million in the prior year’s quarter to a fourth-quarter record of $455 million. Retail net sales edged up 1.3% to $236 million but food service revenue declined 0.4% to $218 million.

Consolidated gross profit dipped 5%, from a fourth-quarter record of $98.4 million to $93.2 million, due to start-up costs at dressing and sauce facility in Horse Cave, Kentucky. Adjusted earnings per share declined 28%, from $1.39 to $1.00, due to lower demand from some large customers and the aforementioned start-up costs.

Lancaster’s earnings growth has been spotty because it is so beholden to volatile restaurant sales. Therefore, the company has made many acquisitions in the past in order to, not only grow the portfolio, but also attempt to make its revenue more predictable.

Source: Investor Presentation

We expect 8% average annual earnings growth over the next five years, with nearly all of this growth driven by revenue growth. We also note that Lancaster will almost certainly not grow linearly, as experience has shown that some years are likely to show declines while others are likely to show sizable increases.

Over time, Lancaster has proven it can grow through a variety of environments, including a pandemic, and we don’t see that as changing anytime soon.

Competitive Advantages & Recession Performance

Lancaster’s competitive advantages are mainly in its distributor partnerships with major sellers like Walmart (WMT) and McLane Distributors, as well as its leadership positions in certain categories like croutons, frozen bread products and dressings.

Lancaster built a niche in these categories over the years and while its heavy reliance upon two distributors for one-third of its revenue is a potential risk, it also means the company’s competitors don’t necessarily have the same access to those large customers. Indeed, we see Lancaster’s exposure to Walmart as a net positive as Walmart enjoys rising grocery sales.

Lancaster is in a strong position within its core categories, but that doesn’t make it immune from recessions. Earnings-per-share during and after the Great Recession are below:

- 2007 earnings-per-share of $1.45 (decrease of 42% from 2006)

- 2008 earnings-per-share of $1.28 (decrease of 12%)

- 2009 earnings-per-share of $3.17 (increase of 147%)

- 2010 earnings-per-share of $4.07 (increase of 28%)

Revenue fared pretty well during this period as Lancaster didn’t see any meaningful declines during the period and in fact, revenue was actually higher in 2008 than 2007. However, pricing and cost of goods suffered and hence margins declined significantly. This produced the earnings declines Lancaster experienced in 2007 and 2008 but to its credit, the rebound was swift and strong in 2009 and 2010.

It is also important to note that Lancaster has a rock-solid, almost debt-free balance sheet. As a result, the company can easily endure rough economic periods and wait patiently for a recovery.

Still, Lancaster is far from recession-proof because it sells products to foodservice customers – which suffer mightily during recessions and would thus order less from Lancaster – and consumers that may become cash-strapped during recessions and eschew the food accessories that the company offers.

Lancaster, however, proved markedly resilient throughout the coronavirus crisis, with just a 9% decrease in earnings per share in 2020 and record earnings per share expected in fiscal 2024.

Valuation & Expected Returns

We expect Lancaster to achieve record earnings-per-share of $6.10 in fiscal 2024 thanks to an expected recovery of sales and sharp easing of cost inflation. Shares are currently trading at 26.6 times this year’s EPS estimate, which is lower than our fair value estimate of 29 times EPS. If the stock trades at our assumed fair valuation level in five years, it will enjoy a 1.7% annualized gain in its returns.

Given also 8% earnings-per-share growth and a 2.1% dividend yield, the stock could offer a total annual return of 11.5% over the next five years. As a result, the stock receives a buy rating.

Final Thoughts

Lancaster is certainly not a high-yield income stock, due to its low yield, but it does have an impressive track record of dividend growth. Unfortunately, the current yield is not high enough to warrant a position simply for the dividend. On the other hand, the promising EPS growth expectations and the reasonable valuation of this Dividend King render it attractive around its current price.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields.

- The Dividend Achievers List is comprised of ~350 stocks with 10+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

- The High ROIC Stocks List: The top 10 stocks with high returns on invested capital.

- The High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta.

- The Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta

- The Complete List of Russell 2000 Stocks

- The Complete List of NASDAQ-100 Stocks