Updated on May 27th, 2025 by Bob Ciura

When you start investing, you know the least about investing that you will ever know.

This can lead to poor initial results, and ultimately ‘quitting’ investing without ever benefiting from the prosperity creating effects of compound interest.

If you are starting from scratch, it pays to begin your investment journey with the knowledge necessary to succeed. This article is your guide on how to invest well, from the start.

Investing can seem extremely complicated. There is a staggering amount of industry-specific knowledge in investing. Fortunately, you don’t need to know it all to do well.

In fact, how to do well as an investor can be boiled down into the following sentence:

Invest in great businesses with strong competitive advantages and shareholder friendly managements trading at fair or better prices.

You can do this by investing in quality dividend growth stocks such as the Dividend Aristocrats, an elite group of 69 stocks in the S&P 500 with 25+ consecutive years of dividend increases.

You can download a full list of all 69 Dividend Aristocrats by clicking on the link below:

Buying high quality businesses has historically been a winning strategy. The bolded statement above covers all there is to know about successful dividend growth investing. However, it is missing some detail.

The rest of this article discusses in detail how to build a dividend growth portfolio, starting with $5,000 or less. You can also watch a detailed analysis on the topic below:

Choosing a Stock Broker and Funding Your Account

The way that we purchase stocks has changed dramatically over the decades.

It used to be very expensive to purchase stocks – a ‘broker’ was an individual, not an online platform. Buying stocks involved calling your stock broker and seeing if he knew anyone who was selling your desired security.

Today, there are a plethora of online stock brokers with easy-to-use trading platforms. The biggest factor in selecting an online broker used to be fees, but recently many brokers have gone to $0 trading commissions, making investing more accessible than ever.

As a self-directed investor, your cost to buy or sell a security could be $0. However, there are a variety of reasons that it could still pay to focus on long-term investing.

Aside from simply buying and selling securities, brokers will charge for things like trading on margin, options and special circumstances.

Some investors will elect to trade on margin as a way to increase returns (with a proportionate increase in risk). This means that an investor will borrow money from their stock broker to purchase more stocks, using existing investments as a collateral.

Different brokers will charge different interest rates on borrowed margin. Typically, the interest rate will decrease as portfolio size increases.

For large portfolios that trade on margin, margin interest rates will be a larger factor than commission fees when determining which broker to use.

A further consideration is a broker’s built-in research capabilities. For investors that are new to the markets, some brokers will have dedicated in-house stock screeners and investment seminars that will help flatten the learning curve as you build your dividend growth portfolio.

All of these factors should come into play when deciding which stock broker to use.

Once you have selected a stock broker, you must then ‘fund’ your account. There are many different mechanisms through which you can fund your investment account.

Some brokers will accept checks delivered via mail. Others accept payments via a bill payment from your financial institutions.

Arrangements can often be made to have money automatically withdrawn from your checking account on a periodic basis (which is ideal for the systematic investor).

Instructions for funding your first investment account will be available on your broker’s website.

Should You Build Your Portfolio With Stocks or ETFs?

In the past, the only way to gain exposure to the financial markets was by investing in individual securities. Investors would buy stakes in companies like Walmart (WMT), Exxon Mobil (XOM), or Johnson & Johnson (JNJ) directly.

That changed with the introduction of the mutual fund and later the exchange-traded fund (ETF). These offerings are financial products where retail investors like you and I purchase a fund and our money is professionally managed by an investment manager.

While we generally oppose mutual funds because of their high fees, ETFs are a low-cost way for investors to gain diversification and access to the financial markets.

ETFs are traded through the same mechanism as shares on the stock exchange (which is not the case with mutual funds). You can purchase ETFs in your brokerage account and hold them for as long (or as short) as you like, just as with stocks.

There is much back-and-forth in the investing industry about what is better: ETFs or individual stocks.

The truth is that both options have pros and cons.

Related: The Pros and Cons of Dividend Investing.

Here are some pros and cons of ETFs versus individual stocks.

Related: The Full List Of Dividend Exchange-Traded Funds.

Pro: Investing in dividend ETFs provides wide diversification.

This is helpful for investors with small portfolios as they can get the necessary diversification from owning multiple stocks quickly.

Evidence shows that most of the benefit of a diversified portfolio comes from owning ~20 stocks. ETFs often hold hundreds of positions, so they might be overdoing it a bit.

With that being said, ETFs are a simple way for investors to gain diversified market exposure.

Pro: Investing in dividend ETFs has a low time commitment.

Once purchased, investors can “forget” about their ETF. No additional research is required.

This low time commitment is a benefit to people who are not interested in selecting individual stocks.

Pro: Dividend ETFs almost always have lower expense ratios than their mutual fund counterparts.

There are several dividend ETFs that have annual expense ratios below 0.1%. Many dividend mutual funds have a fee of 1% or more (which amounts to $1,000 in annual fees on a $100,000 portfolio).

Con: Dividend ETFs are always more expensive than owning individual stocks.

After the initial purchase is made, individual stocks don’t have an expense ratio; looked at another way, they will always have an expense ratio of 0.00%. There is no cost to hold a stock, regardless of the holding period.

Con: You cannot hand-select which businesses you own with a dividend ETF.

Dividend ETFs give you no control over your portfolio. You cannot buy or sell individual stocks, which means you cannot fine-tune your strategy to match your specific needs.

There are many cases where you would want to tweak your portfolio to meet certain needs. For example:

- Only stocks with 4%+ dividend yields (the Sure Retirement criterion)

- If you dislike a particular sector

- Hold only stocks with high levels of insider ownership

The endless customization possibilities are one of the major advantages of buying individual stocks over ETFs.

Conclusion: There is nothing necessarily wrong with dividend ETFs.

For investors with minimal time or interest in investing, ETFs are an excellent alternative to high-fee mutual funds.

With that being said, Sure Dividend prefers to invest in individual businesses. The rest of this article will explore this avenue.

Related: Do Individual Stocks or Index Funds Make The Better Investment?

Where to Find Great Businesses

To invest in great businesses, you have to find them first.

Sure Dividend generally recommends two databases of stocks as a source of high-quality dividend-paying businesses. Both of them are based on consecutive streaks of dividend increases.

Consecutive dividend increases are important because they demonstrate two things:

- The business is doing well

- The management is shareholder-friendly

With regards to the first point, a company cannot raise its dividend over the long-term if earnings are not also increasing.

While dividends may outpace earnings in the short-term, this is impossible over the long-term. A very long streak of constantly rising dividends means that a company has grown dividends (and earnings) through everything the market has thrown at it.

Secondly, shareholder-friendly management teams are a telltale sign of a great business. Exceptional people create exceptional companies, plain and simple.

The first source of great businesses we recommend is the Dividend Aristocrats Index. In order to be a Dividend Aristocrat, a company must:

- Be in the S&P 500

- Have 25+ consecutive years of dividend increases

- Meet certain minimum size & liquidity requirements

The Dividend Aristocrats have historically outperformed the overall stock market as measured by the S&P 500 Index.

Another great place to look for high-quality businesses is the Dividend Kings.

Like the Dividend Aristocrats, the Dividend Kings list is based on historical dividend increases – except it is even more exclusive. To be a Dividend King, a company must have 50+ years of consecutive dividend increases.

You can see the list of all 55 Dividend Kings here.

The Sure Analysis Research Database covers 150+ businesses with 25+ years of steady or rising dividend payments. (Including many companies beyond the Dividend Aristocrats and Dividend Kings).

How To Know If A Great Business Is Trading At Fair Or Better Prices

Finding great businesses with shareholder-friendly management is the first step.

The second is to determine if these great businesses are trading at fair or better prices. Even the best company becomes a poor investment if an investor pays too high a price.

“For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favorable business developments.”

– Warren Buffett

A very quick-and-easy rule of thumb is to look for great businesses trading at or below the S&P 500’s price-to-earnings ratio. If a business is higher-than-average quality, you would think it would command a higher price-to-earnings ratio than the market average (as measured by the S&P 500).

Great businesses that trade below the S&P 500’s price-to-earnings ratio are a good place to look into value with more detail. The S&P 500’s price-to-earnings ratio is currently 27.6.

Beyond comparing stocks to the overall market, investors should compare a business’ price-to-earnings ratio to both:

- Its 10-year historical average price-to-earnings ratio

- Its competitors’ price-to-earnings ratio

It is important to remember to use adjusted earnings when comparing price-to-earnings multiples.

GAAP earnings can be reduced by one time effects such as acquisition costs or depreciation charges. Similarly, GAAP earnings can be artificially inflated if the company sells assets.

These charges are accounting based, not reality based, and may not truly communicate the long-term earnings power of a business.

Another stock list of interest is the high dividend stocks list: 5%+ yielding stocks.

Buying Your First Stock

Once you have identified a high-quality business trading at an attractive valuation, it is time to buy.

Buying stocks can seem just as complicated as analyzing stocks. It is not as simple as just pushing ‘buy’ – there are a number of different order types that investors can use, depending on the circumstances.

For simplicity’s sake, the beginning investor should only be concerned with two types of orders:

- Market order

- Limit order

A market order is when you communicate to your broker ‘buy this stock at prevailing market prices’. Market orders are always the quickest way to execute a trade.

Market orders have downsides. If the stock price moves quickly after you place your order, you may end up buying the stock at a higher price than you wanted.

Limit orders are the solution to this problem. A limit order is when you communicate to your broker ‘buy this stock, but only at a price of X or below‘.

For example, if Target (TGT) was trading at $100 and you wanted to buy at $80, you could place a limit order for $130 and the order might never be filled unless Target stock dropped to $80 (or below).

There are many other types of buy orders and also equivalent sell orders.

However, limit orders are generally the best way to ensure that you are getting a fair or better price on a trade.

More sophisticated investors can also take advantage of options to buy and sell stocks to increase income.

However, these strategies are more advanced in nature and should not be pursued until investors have a firm grasp of the other investing basics and fundamentals that are described in this article.

How Many Stocks Should You Hold?

There is a tradeoff with diversification.

The more stock you hold, the safer you are if any one of them does poorly. On the other hand, you have less to gain from the stocks you hold that do well.

Professional investors also experience this divide. Warren Buffett, the CEO and Chairman of Berkshire Hathaway, manages a ~$300 billion common stock portfolio where his top 5 holdings make up over 70% of his portfolio.

You can see Warren Buffett’s top 20 stocks here.

Buffett does not have a very diversified portfolio.

Peter Lynch, on the other hand, most certainly did (he is now retired). As the manager of the Magellan Fund at Fidelity Investments between 1977 and 1990, Lynch’s portfolio averaged a 29.2% annual return – making him the best-performing mutual fund manager in the world.

Although managing much less than Buffett – around $14 billion at his peak – Lynch was known to hold more than 1,000 individual stock positions. Lynch had a very diversified portfolio.

Who is right? The empirical data suggests that a 1,000-position stock portfolio is unnecessary. According to studies cited by Morningstar:

“About 90% of the maximum benefit of diversification was derived from portfolios of 12 to 18 stocks.“

Holding a portfolio of ~20 stocks gives 90% of the benefits of holding 100+ stocks. There are also numerous advantages to holding around 20 stocks.

First of all, holding 20 stocks means you get to invest in your best ideas. You can own the businesses you are most comfortable holding – the ones that you believe have the greatest total return potential.

Related: How To Calculate Expected Total Return For Any Stock

Holding a large portfolio of 100 or 200 stocks also requires a large time commitment and is virtually impossible to keep up with. It’s hard to really know 100+ businesses. Keeping up with the quarterly earnings reports of this many businesses would be a huge endeavor – much less so for 20 businesses.

So investing in around 20 businesses is the ‘sweet spot’ between investing in only your best ideas while still benefiting from diversification.

You can’t just own any 20 stocks and be diversified, however.

As an example, if you owned 20 upstream oil corporations, you would not be well diversified. Similarly, owning 20 biotech companies does not a diversified portfolio make.

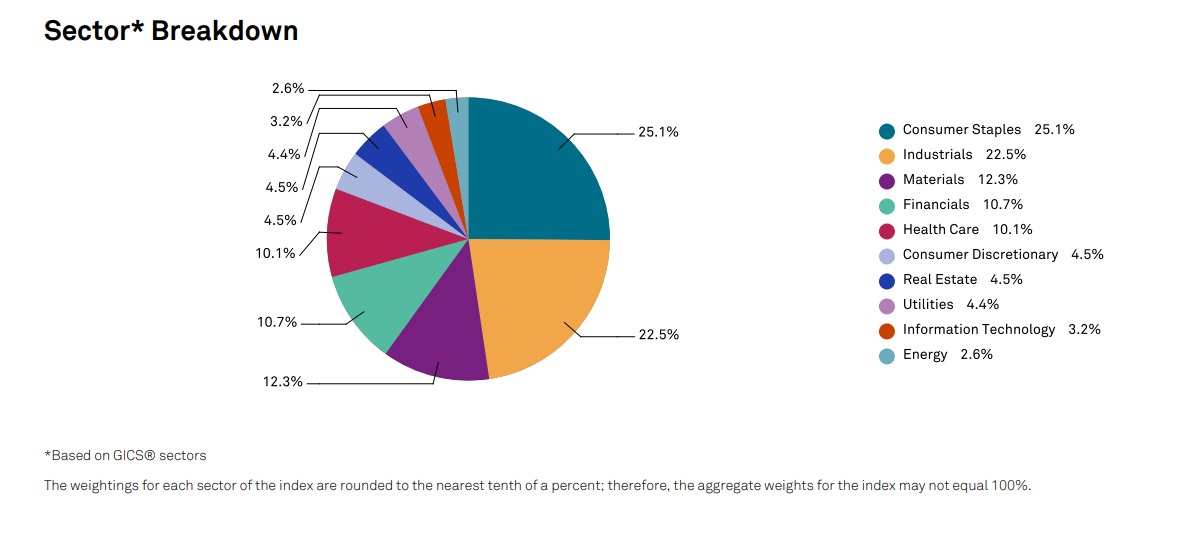

Dividend growth investors should look to invest in different sectors to gain exposure to different types of great businesses.

The list of Dividend Aristocrats is balanced across market sectors.

Source: Fact Sheet

Clearly, there exist high-quality business in basically every sector.

The next section discusses different portfolio building strategies.

Dividend Growth Portfolio Building Strategy

There are two types of ‘new’ dividend growth investors:

- Those that are starting from scratch

- Those with sizeable portfolios looking to transfer over to dividend growth investing

This article is about starting from scratch. That’s what will be covered in this section.

Building a high-quality dividend growth portfolio is a process. Diversified dividend income will not be created overnight. The process will take time, just like most important things in life. The webinar replay below covers how to build a dividend growth portfolio for rising passive income in detail.

I recommend buying the highest ranked stock you own the least every month based on your specific criteria. Each criterion should be selected to either increase returns or reduce risk.

Further, each criterion should be supported by empirical evidence with logical underpinnings (not clearly unrelated relationships like ‘companies with CEOs named Jim have outperformed over the past X years’).

The longer you invest, the more money you have to invest, and the more diversified your portfolio will become.

No matter how selective you are when purchasing stocks for your dividend growth portfolio, you will eventually have to trim the ‘dead weight’. The composition of your portfolio will undoubtedly change over time.

The best investments are long-term in nature. Once a stock is purchased, investors should prefer to let it compound their wealth indefinitely.

A long-term orientation also provides individual investors with a competitive advantage over institutional investors like pension plans and mutual funds, whose performance is judged on a quarter-over-quarter basis.

“The single greatest edge an investor can have is a long term orientation”

– Seth Klarman

With that being said, holding a stock for the long-term is not always possible. Things happen. Businesses that were great at one time lose their competitive advantage.

This can happen by management losing its way, technology changes, or by competitors finding a way to destroy or copy the company’s competitive advantage.

When a business loses its ability to compound your wealth through rising dividend payments, it is time to sell.

The primary sell criteria according to the general method at Sure Dividend is to sell when a business cuts or eliminates its dividend. This is a very clear sign from management that either:

- The dividend is not important (shareholders don’t matter)

- The business cannot sustain its dividend (business is in decline)

In either case, that is not the type of investment likely to generate long-term wealth. Of course, there are exceptions.

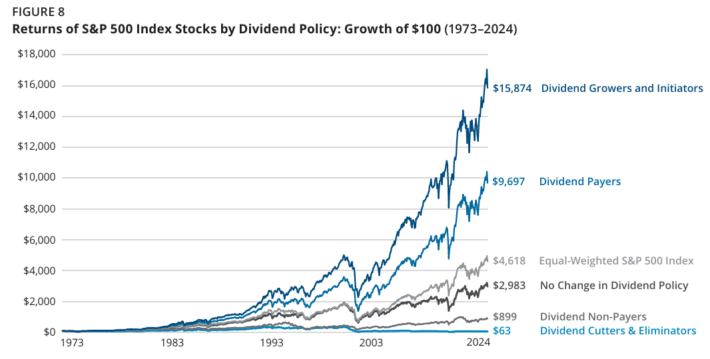

Sometimes businesses rebound after dividend cuts. However, the historical record shows that dividend cutters make poor investments, on average.

More specifically, dividend cutters have had a lower return and a higher standard deviation than all other classes of stocks, resulting in terrible performance on a risk-adjusted basis.

Source: Hartford Funds – The Power Of Dividends

Fortunately, there are typically many more dividend growers & initiators than dividend cutters/eliminators at any given time. This makes it easier (and less risky) for dividend growth investors to execute their investment strategy.

There is one other good reason to sell a dividend growth stock – if it becomes wildly and absurdly overvalued.

It is better to profit from this overconfidence by selling than to participate in it. Profits can be reinvested into dividend growth stocks with sane valuations.

This benefits investors in a number of ways. Stocks with lower valuations have better total return potential, all else being equal.

Similarly, two companies that have the same earnings and payout ratios but with different valuations will also have different dividend yields – the lower-valued company will generate more dividend income for shareholders.

Discipline Is The Key

What sets apart those who will retire wealthy from the rest is the amount of discipline you have to stick with the plan you lay out.

If your investment strategy is sound, and you follow it diligently, you are likely to do well in the market over time. The stock market does not go up in a straight line.

You can experience losses of 50% or more investing only in stocks. If you have the fortitude to persevere through market downturns, you can benefit from the compounding effect of owning fantastic businesses over long periods of time.

On the other hand, if you sell when things look their worst – like March, 2009 – you will likely underperform the market by a wide margin.

Staying fully invested throughout market cycles appears to be the best strategy. Missing a few key days over the long run can have a profound effect on investment performance.

Sadly, most individual investors tend to buy and sell far too often.

The study The Behaviour of Individual Investors by Brad Barber and Terrance Odean revealed the unfortunate truth about individual investors.

The authors analyzed data from 78,000 individual investors. They found that when individual investors sell a stock to buy another, the stock they sold outperforms the stock they purchased (on average).

This means we tend to buy and sell at the wrong times… What’s the solution?

Practice ‘do nothing’ investing. Don’t sell stocks without a very good reason. Price declines are not a good reason unless the underlying business has deteriorated.

For a moment, compare investing to grocery shopping. If you bought steak for $10 and it went on sale for $8, would you go back and return the steak you had already purchased? No! You would buy more.

When a stock’s price declines, you can buy more for a better deal (assuming the underlying business has not significantly changed). This makes stock declines the right time to add to your positions, not sell them.

Final Thoughts: Why Investing Matters

Why is investing important?

Because creating a passive income stream allows for financial flexibility in your life. You can take control of your time when you don’t have to worry about having a job to fund your needs.

With every step along the way, with each dividend check that comes in, you are closer and closer to the goal of financial independence. It is not a quick process, but it is certainly worthwhile.

The national GDP has marched upward over time, yet people are often not able to retire when they want or on their own terms.

Dividend growth investing will help you build a retirement portfolio that pays growing dividend income. This can lead to retirement on time – or even early retirement.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The 20 Highest Yielding Dividend Aristocrats

- The 20 Highest Yielding Dividend Kings

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: